How to Build a Property Portfolio in the UK for 2026

How to Build a Property Portfolio in the UK for 2026

Knowing how to build a property portfolio in the UK for 2026 and beyond is not about timing the market perfectly; it's about executing a clear, repeatable process. The answer lies in mastering five core areas: defining a UK-specific strategy, securing the right finance, analysing deals with precision, managing assets effectively, and knowing how to scale. This guide provides actionable insights for each stage, giving you a blueprint for building a resilient portfolio. For an immediate advantage, the DealSheet AI app is a game-changer, handling complex UK tax rules and financial modelling to turn property listings into investment-ready reports in seconds.

Your Blueprint for Building a UK Property Portfolio

Learning how to build a property portfolio can feel overwhelming, but it boils down to making a series of smart, calculated decisions. Success isn't about owning the most properties; it's about owning the right ones that work together to get you where you want to go.

Think of your portfolio as more than just a collection of buildings. It's a strategic assembly of assets, each with a specific job to do—whether that's generating income, delivering growth, or a blend of both.

The journey starts not with property viewings, but with a bit of introspection. Before you even glance at Rightmove, you need to define what success looks like for you. Are you chasing monthly cash flow that could one day replace your salary? Or is the main goal long-term capital appreciation, building serious wealth over a couple of decades? Your answers here will shape every single choice you make from this point on.

Defining Your Long-Term Vision

Every single successful investor started with a crystal-clear end goal. This vision is your compass, the thing that keeps you on track when UK markets get choppy or a deal gets complicated.

So, where do you want to be in 5, 10, and 20 years?

Your financial objectives will likely fall into one of these buckets:

- Generating Passive Income: Creating a steady stream of rental income to cover your living expenses and give you freedom.

- Wealth Accumulation: Building significant equity through property value growth over the long haul.

- Capital Recycling: Using strategies like BRRRR (Buy, Refurbish, Refinance, Rent) to rapidly expand your portfolio with a limited starting pot of cash.

A well-defined strategy is the difference between simply buying properties and intentionally building a portfolio. It ensures each purchase gets you one step closer to your ultimate destination, rather than just adding another address to your list.

This guide will serve as your blueprint for 2026 and beyond, kicking off with the most fundamental step: choosing an investment strategy that actually fits your vision. We'll dive into the most effective UK property strategies out there, helping you pick the one that lines up with your cash position and appetite for risk.

Choosing Your Foundational Investment Strategy

Your investment strategy is the compass for your entire portfolio. It's not just about buying property; it's about buying the right property, for the right reasons, at the right time. Without a clear path, you risk ending up with a jumble of assets that don't work together to get you where you want to be.

The best strategy for you will lock in with three things: your available cash, your appetite for risk, and how much time you can actually commit. Each one strikes a different balance between cash flow, capital growth, and the sheer amount of hands-on work required. Picking your lane is the most important decision you'll make at the start.

Buy-to-Let: The Bedrock of Many Portfolios

The classic Buy-to-Let (BTL) is where most UK investors cut their teeth, and for good reason. The concept is beautifully simple: buy a property, rent it out, and the monthly rent covers your mortgage and costs, leaving you with a profit.

Investors favour this route for its steady, predictable cash flow and the slow, compounding power of long-term capital growth. It's a marathon, not a sprint. Building real wealth here usually means stacking up several BTLs over a number of years.

Think of a typical BTL investor in 2026. They might buy a two-bedroom flat in a commuter town like Reading. Their entire focus is on finding a solid property in a high-demand area that attracts professional tenants, keeping those dreaded empty periods to a minimum.

Houses in Multiple Occupation: Dialing Up the Yields

For those willing to roll up their sleeves, Houses in Multiple Occupation (HMOs) offer a way to seriously ramp up your rental yields. The model is simple: instead of renting a whole house to one family, you rent it out room by room to several different tenants.

Because you're collecting multiple streams of rent from a single asset, the gross yield is often dramatically higher than a standard BTL. A four-bed house that might fetch £1,500 per month for a family could generate £2,400 (at £600 per room) as an HMO.

But that extra income comes at a price. You're facing more complex management, much stricter regulations, and higher setup costs for conversions and furnishings. You can explore more about different UK property investment strategies in our detailed guide.

BRRRR: Recycling Your Capital for Rapid Growth

The Buy, Refurbish, Refinance, Rent (BRRRR) strategy is a powerhouse for investors who want to scale fast without a massive pot of starting cash. You buy a tired, unloved property, force the value up through a smart refurbishment, and then refinance it based on its shiny new valuation.

Done right, this lets you pull out most—and sometimes all—of your initial investment to roll straight into the next project.

Imagine you buy a run-down terraced house in Manchester for £120,000. You spend £20,000 on a full renovation, and it's then revalued at £180,000. A lender offers a 75% mortgage on the new value, giving you £135,000. This pays off your initial costs and frees up your capital for the next deal.

Be warned, though: this strategy isn't for the faint of heart. It demands a rock-solid grasp of renovation costs, local market values, and the ability to manage a project without it spiraling out of control.

Flipping for Quick Equity Gains

Property flipping is an active, short-term play. You buy a property, give it a quick and impactful renovation, and sell it on for a profit. The focus here is entirely on capital gains, not rental income.

Success hinges on three things: buying at the right price, budgeting your refurb accurately, and knowing the local market inside out to ensure you can sell it quickly. The lure of a big, tax-free (potentially) lump sum is strong, but so are the risks. A sudden market dip or a nasty surprise behind the plasterboard can wipe out your profit margin in a flash.

Serviced Accommodation: Tapping into the Travel Market

Serviced Accommodation (SA), often seen as short-term lets on platforms like Airbnb, means letting a fully furnished property for short stints—from a few nights to a few weeks. This can generate far higher income than a traditional BTL.

An investor might run a high-spec SA apartment in a tourist hotspot like Bath, catering to holidaymakers and business travellers. But while the nightly rates are fantastic, the management intensity is off the charts. You're not just a landlord; you're running a hospitality business with constant guest communication, cleaning, and marketing.

UK Property Investment Strategy Comparison

To make sense of these options, it helps to see them side-by-side. Each strategy serves a different purpose, and what works for one investor might be a disaster for another. The key is aligning the strategy with your own resources and goals.

This table breaks down the core differences in capital, returns, and effort.

| Strategy | Best For | Typical Yield | Capital Required | Management Level |

|---|---|---|---|---|

| Buy-to-Let (BTL) | Steady cash flow & long-term growth. | 4-6% | Medium | Low to Medium |

| HMO | Maximising cash flow from a single asset. | 8-12%+ | Medium to High | High |

| BRRRR | Rapidly scaling a portfolio with limited capital. | Varies | Low (recycled) | High |

| Flipping | Generating lump-sum capital gains. | N/A (Profit Margin) | Medium to High | High |

| Serviced Accommodation | High income potential in tourist/business areas. | 10-15%+ | Medium to High | Very High |

Ultimately, there's no single "best" strategy—only the one that is best for you. Use this as a starting point to decide which path feels right, then dive deep into the mechanics of making it work.

Financing Your Portfolio and Using Leverage Smartly

Securing the right finance is the fuel for your entire property engine. Once you've picked a strategy, figuring out how to fund your purchases is the next critical hurdle. This is all about getting to grips with leverage—using borrowed money to amplify your returns—without accidentally blowing up your portfolio.

For most UK investors, the journey starts with a standard buy-to-let (BTL) mortgage. Unlike the mortgage on your own home, lenders will expect a much bigger deposit, usually around 25% of the property's value. So, for a £200,000 property, you'll need £50,000 in cash ready to go, plus extra funds for your solicitor and Stamp Duty.

But lenders aren't just looking at your deposit. They're stress-testing your deal to see if it can stand on its own two feet. They need absolute confidence the rent will cover the mortgage, even if the Bank of England decides to hike interest rates.

How Lenders Actually Assess Your BTL Mortgage Application

Lenders use a strict affordability calculation called a "stress test." It sounds complicated, but the logic is simple. They'll typically want the projected rental income to be at least 125% of the mortgage payment, calculated at a hypothetical interest rate that's much higher than your actual deal—often around 5.5% or even more.

This is a make-or-break calculation. A property might look profitable on your spreadsheet, but if it fails this test, you won't get the mortgage. Think of it as a safety net designed to protect both you and the bank from future pain.

A key part of building a property portfolio is understanding that borrowing is a tool. Used correctly, leverage can dramatically accelerate wealth creation. Used carelessly, it can magnify losses and put your entire portfolio at risk.

Beyond the Standard Buy-to-Let Mortgage

While BTL mortgages are the workhorse for most investors, they're not the only tool in the box. Different situations and strategies call for different kinds of funding.

- Bridging Loans: This is fast, short-term finance. It's perfect for buying at auction where you have to complete in just 28 days. You'd also use a bridging loan to snap up an unmortgageable wreck, do it up, and then refinance onto a standard BTL mortgage once the work is complete.

- Commercial Finance: As your portfolio gets bigger, especially if you start buying multi-unit blocks or larger HMOs, you'll likely move from individual BTL products to commercial loans. Lenders here are less concerned with your personal income and more focused on the asset's commercial viability and your track record as an operator.

- Further Advances & Remortgaging: This is how you pull equity out of your existing properties to fund new deals. Once a property has gone up in value, you can remortgage to release some of that tax-free capital, giving you the deposit for your next purchase.

Getting your head around the different funding avenues is vital. Our guide on how to finance property development takes a much deeper dive into these options.

The Power and Peril of Loan-to-Value

Your Loan-to-Value (LTV) ratio is just the size of your mortgage compared to the property's value. A £150,000 mortgage on a £200,000 property means you have a 75% LTV. Keeping a sensible LTV across your entire portfolio is non-negotiable for long-term survival and growth.

Why does it matter so much? A lower LTV (say, 60-65%) gives you a huge buffer if the market turns south. If property prices suddenly drop by 10%, you won't be plunged into negative equity. It also makes you a much more attractive customer to lenders when you want to refinance or buy again.

On the other hand, pushing your LTV to the max across all your properties leaves you dangerously exposed. A small dip in values could wipe out your equity, and a jump in interest rates could make your entire portfolio unprofitable. Smart investors use leverage to grow, but they always keep a close eye on their overall LTV, making sure they have the resilience to ride out the inevitable market cycles. It's a constant balancing act between ambition and prudence.

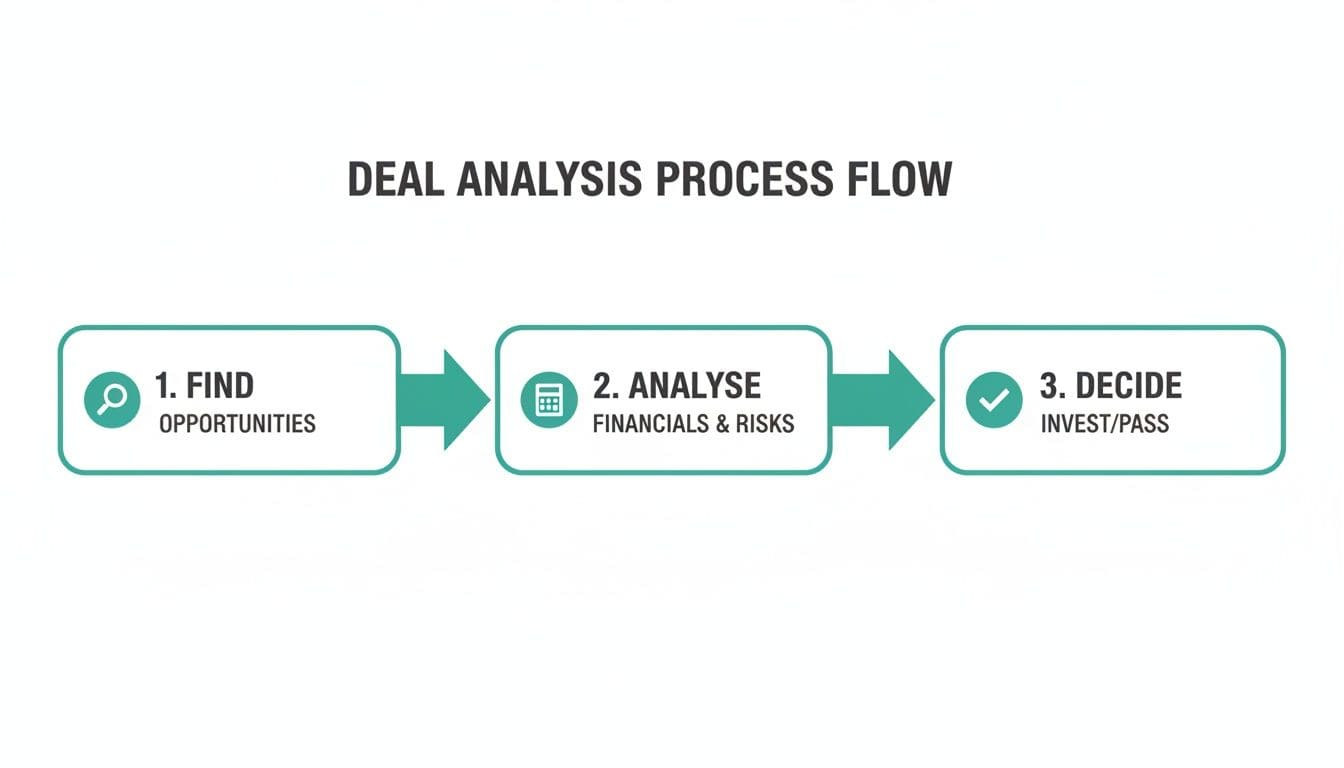

Mastering Deal Analysis to Find Winning Properties

Anyone can find a property for sale. The real skill is finding the hidden gems, and that comes down to one thing: deal analysis. This is the critical, non-negotiable process of vetting a deal's financial potential. Get this right, and you're on your way. Get it wrong, and you're just buying yourself a headache.

We're about to demystify the key metrics you'll live by, from rental yield to the all-important cash-on-cash return. You'll learn how to forecast every conceivable cost, from Stamp Duty (SDLT) and solicitor fees to those sneaky maintenance issues that always pop up.

Doing this manually is slow, painful, and riddled with potential for costly errors. It's why tools like DealSheet AI are becoming so essential. You can feed it a property link, and it instantly applies UK tax rules and runs the numbers, giving you a clear go or no-go decision in seconds.

Ultimately, proper deal analysis breaks down into three core stages, moving from that initial spark of interest to a confident, numbers-backed investment decision.

This isn't about guesswork. It's a repeatable system designed to filter out the duds and pinpoint the winners, time and time again.

The Essential Metrics You Must Know

Before you get emotionally attached to that charming Victorian terrace, you need to let the numbers do the talking. A few key performance indicators (KPIs) will tell you 90% of what you need to know about whether a deal has legs.

- Gross Yield: The simplest metric and a good starting point. It's just the total annual rent divided by the purchase price. So, a £200,000 property renting for £1,000 a month (£12,000 a year) has a 6% gross yield. It's handy for quickly comparing different areas.

- Net Yield: This is your first reality check. Net yield takes your annual rent and subtracts all running costs—mortgage, insurance, voids, maintenance, the lot. That final figure, divided by the purchase price, shows the asset's true profitability.

- Cash-on-Cash Return: For portfolio builders, this is arguably the most important number. It measures your annual pre-tax cash flow against the total cash you actually put into the deal (deposit plus all your transaction costs). It bluntly answers the question: "How hard is my cash actually working for me?"

A high gross yield means absolutely nothing if your running costs are sky-high. Always, always focus on the net figures and your cash-on-cash return. That's what actually lands in your bank account.

For a deeper dive into the numbers that matter, check out our complete guide to analysing UK buy-to-let deals for 2026.

Forecasting Costs Like a Pro

The line between a profitable deal and a money pit is often drawn by how accurately you estimate costs. Your analysis must go miles beyond just the purchase price and mortgage payment.

You have to factor in everything:

- Upfront Costs: Stamp Duty Land Tax (SDLT), solicitor fees, mortgage arrangement fees, and survey costs all add up.

- Refurbishment Budget: Get detailed quotes, not just a finger-in-the-air guess. And whatever that number is, always add a 10-15% contingency for the inevitable surprises.

- Ongoing Costs: Landlord insurance, letting agent fees (typically 8-12% of rent), service charges, ground rent, and an allowance for void periods are non-negotiable. I always budget for at least one month's rent per year for voids.

- Maintenance: A solid rule of thumb is to set aside 1% of the property's value annually for repairs and upkeep.

A Real-World Deal Analysis Example

Let's run the numbers on a typical three-bed terraced house in the Midlands—a classic starting point for anyone figuring out how to build a property portfolio.

First, the capital outlay:

- Purchase Price: £250,000

- Deposit (25%): £62,500

- Stamp Duty & Fees: £10,000

- Refurbishment: £5,000

- Total Cash Invested: £77,500

Now, let's look at the operational figures:

- Monthly Rent: £1,200 (£14,400 per year)

- Monthly Mortgage (5% interest-only): £781 (£9,372 per year)

- Monthly Costs (insurance, voids, maintenance): £200 (£2,400 per year)

So, your Net Annual Cash Flow is £14,400 (rent) - £9,372 (mortgage) - £2,400 (costs) = £2,628.

And the big one, your Cash-on-Cash Return, is £2,628 / £77,500 = 3.4%.

This simple calculation tells you instantly whether the deal stacks up. In this case, a 3.4% return might be too low for many investors, flagging it as one to pass on.

The BRRRR Analysis Checklist

When you're running a BRRRR deal, the analysis has more moving parts. The purchase is just the beginning; you also need to nail the refurb costs, holding expenses, and the all-important refinance valuation. A simple checklist can keep you from missing a critical expense that could derail the whole project.

Here's a sample checklist to guide your analysis process.

Sample BRRRR Deal Analysis Checklist

| Metric/Cost Item | Calculation/Consideration | Example Value |

|---|---|---|

| Purchase Price | Agreed sale price. | £150,000 |

| Total Upfront Cash | Deposit + SDLT + Legal/Broker Fees. | £45,000 |

| Refurbishment Budget | Detailed quotes for all planned works. | £25,000 |

| Contingency Fund | 15% of the refurb budget for unexpected issues. | £3,750 |

| Holding Costs | Bridge/finance interest, insurance, council tax during refurb. | £6,000 (6 months) |

| Total Cash Deployed | Sum of all cash costs before refinance. | £79,750 |

| GDV (Gross Development Value) | Estimated end value post-refurb, backed by comps. | £240,000 |

| Refinance LTV | Lender's Loan-to-Value, typically 75%. | 75% |

| Refinance Amount | GDV x LTV (e.g., £240,000 x 0.75). | £180,000 |

| Cash Left In | Total Cash Deployed - Refinance Amount. | -£250 (cash out) |

| End Rental Income | Realistic monthly rent based on post-refurb condition. | £1,100 |

| New Mortgage Payment | Based on refinance amount and current BTL rates. | £750 |

| Final Monthly Cash Flow | Rent - Mortgage - Ongoing Costs (voids, maintenance). | £200 |

This kind of structured analysis forces you to think through every phase of the project, from the initial purchase right through to the final rental cash flow. It's this level of detail that separates a successful, profitable BRRRR from one that leaves you with your cash trapped and your profits eroded.

Scaling Your Portfolio From One Property to Many

Getting from your first investment property to your second, third, and beyond is where you stop being just a landlord and start becoming a true portfolio builder. This isn't just about having more capital; it's a leap that demands solid systems, a clear strategy, and a completely different mindset. The game changes from closing one deal to creating a repeatable process for sustainable, rapid expansion.

The real goal here is to turn that first successful project into a self-sustaining engine for growth. A cornerstone of this is figuring out how to recycle your initial capital—pulling your deposit out of one deal to fund the next one. This is how you learn how to build a property portfolio without needing a bottomless pit of cash.

As you grow, the focus shifts from finding a single great deal to managing risk across multiple assets. You'll need to learn how to stress-test your holdings against interest rate hikes and economic wobbles, all while having clear exit strategies in place. This ensures your growth isn't just fast, but resilient.

Recycling Capital to Fuel Growth

The BRRRR method (Buy, Refurbish, Refinance, Rent) is an absolute powerhouse for scaling. Its magic lies in allowing you to pull your initial capital back out after adding value, freeing it up for the next purchase. This creates a powerful compounding effect where your original pot of money can be used over and over again to acquire more properties.

But here's the catch: successful recycling hinges entirely on the accuracy of your deal analysis. You have to be confident that the post-refurbishment valuation will be high enough for a new mortgage to cover your original purchase price, the refurb costs, and all the associated fees. Misjudge that end value, and your capital stays trapped.

Assembling Your Power Team

Let's be clear: you cannot scale a property business alone. As you grow, you need a trusted network of professionals who understand the investor mindset and can move at pace. Your 'power team' isn't a luxury; it's an essential asset.

This team absolutely must include:

- A Specialist Mortgage Broker: Not just any broker. You need someone with whole-of-market access who gets the nuances of portfolio finance, limited company mortgages, and the complex lending criteria that comes with them.

- An Efficient Solicitor: A proactive, communicative conveyancer who is experienced with investor deals is worth their weight in gold. These transactions often move much faster than standard residential sales, and a slow solicitor can kill a deal.

- A Property-Savvy Accountant: Their job is far more than just filing tax returns. They should be providing strategic advice on tax efficiency, company structures (like holding properties in a limited company), and navigating the minefield of Section 24 mortgage interest relief changes.

Building a relationship with these professionals before you need them is critical. When a great deal appears, having a team ready to spring into action can be the difference between securing the property and missing out.

A good power team saves you time, money, and countless headaches. It allows you to focus on high-value work like finding the next deal, rather than getting bogged down in paperwork. Shifting to a portfolio-level mindset for landlords is crucial at this stage.

To Self-Manage or Delegate

With one or two properties, self-management is often doable. But once your portfolio hits five, ten, or more units, the administrative burden can become crushing. The constant calls about leaky taps and tenant queries will drag you away from what you should be doing: sourcing and financing your next project.

This is the crossroads where you must decide whether to hire a letting agent.

- Pros of Hiring an Agent: They take care of tenant sourcing, referencing, rent collection, and maintenance calls, freeing up your time. A good agent also ensures you're always on top of legal compliance.

- Cons of Hiring an Agent: The main drawback is the cost, which typically runs at 8-12% of the monthly rent plus VAT. You also give up some control over who you let your property to and how it's managed day-to-day.

Ultimately, the decision comes down to a simple calculation: is the time you save worth more than the fee you pay? For most investors serious about scaling, the answer is a resounding yes.

Managing Risk as You Expand

A bigger portfolio brings bigger rewards, but it also amplifies risk. A minor issue in a single property can become a major financial headache when it's replicated across ten. That's why stress-testing your portfolio isn't optional; it's non-negotiable.

You should be regularly modelling how your portfolio's cash flow would cope with interest rate rises. For instance, what happens if your mortgage rates jump by 2%? Does the portfolio stay profitable, or does it start haemorrhaging cash? This analysis reveals your financial buffer and flags which properties might become vulnerable.

A cornerstone of UK property portfolio growth is leveraging house price appreciation. The Halifax House Price Index offers 42 years of data showing consistent long-term gains. From a low of just 45.16 points in January 1983, the index climbed to an all-time high of 516.90 in October 2025. This trajectory means a £100,000 investment made 25 years ago would be worth an average of £454,000 today, nationally. You can read more about these long-term trends in the UK housing index.

Finally, have a clear exit strategy for every single asset. If a property consistently underperforms, fails to hit its projected returns, or causes a disproportionate amount of management pain, be prepared to sell it. A successful portfolio is actively managed, and sometimes that means pruning weaker assets to redeploy your capital into better opportunities.

Understanding Market Cycles and Timing Your Entry

Great investors don't just find good deals; they understand the bigger picture. Knowing how to build a property portfolio that stands the test of time means learning to read the UK property market cycle and use it to your advantage, making strategic moves instead of just reacting to scary headlines.

Spotting patterns in the data helps you find opportunities where everyone else only sees risk. Take low transaction volumes, for example. When fewer properties are selling, it often signals a buyer's market—the perfect time to negotiate better prices and terms from sellers who need to get a deal done.

Reading the Economic Tea Leaves

The UK property market is never a straight line. It ebbs and flows in cycles, pushed and pulled by much bigger economic forces. The two most powerful influences are almost always government policy and Bank of England decisions, as they directly shape how buyers feel and what they can actually afford.

- Government Policy: Think back to the 2021 stamp duty holiday. Fiscal incentives like that can create short, sharp booms, artificially pumping up demand and prices. If you understand these policies, you can see the market shifts coming.

- Bank of England Decisions: Every time interest rates change, it has a direct impact on mortgage affordability. When rates go up, borrowing gets more expensive. That tends to cool the market down, creating a window of opportunity for cash-rich investors.

The real secret is to play the long game. By letting data guide your decisions, you can time your purchases for maximum impact—buying when others are fearful and holding firm when the market is flying high.

Using Transaction Data to Your Advantage

One of the clearest signals of market health—and your cue to enter—is transaction volume. If you want to build a property portfolio in the UK, you need to watch this data closely because it reveals the best moments to strike.

HMRC data shows just how wild the swings can be. Transactions peaked at a massive 1,082,900 in 2021-2022, fuelled by stamp duty holidays, before dropping to 773,280 in 2023-2024 as interest rates bit hard. That data tells a story about timing: jumping in during lulls, like the low-volume market of 2023, is how you get better pricing. You can dig into the official numbers in the UK monthly property transactions commentary on GOV.UK.

The most experienced investors often scale their portfolios by buying 5-10 properties a year during these dips, compounding their returns when the market inevitably recovers. Timing your entry isn't just about finding one cheap house; it's about acquiring the right assets in the right places at the right phase of the cycle. To help pinpoint those prime locations, you might want to check out our guide on the best investment property cities in the UK.

This strategic approach turns market volatility from a threat into your single biggest opportunity for growth.

Got Questions? Let's Get Them Answered

Starting a property portfolio journey in the UK always brings up a few classic questions. It's only natural. Let's tackle some of the most common ones I hear from investors, so you can move forward with a bit more clarity.

How Much Money Do I Actually Need to Get Started?

There's no magic number, but let's be realistic. The biggest hurdle is usually the deposit for your first buy-to-let mortgage, which lenders typically set at 25% of the property's value.

So, for a £150,000 property, you're looking at a £37,500 deposit. But don't stop there. You'll also need to cover the costs of the transaction itself—Stamp Duty, solicitor fees, and surveys. Budget another 5-7% for those. All in, having around £45,000 to £50,000 liquid and ready to go gives you a solid, realistic launchpad for that first investment.

Should I Buy One Pricey Property or a Few Cheaper Ones?

This really comes down to your strategy and what you're trying to achieve. There's no single right answer, just trade-offs.

Spreading your capital across several cheaper properties gives you immediate diversification. If one property sits empty for a month, you still have rent coming in from the others to cover the bills. These properties are also often found in areas with higher rental yields, which is great for cash flow.

On the other hand, a single, more expensive property might be in a prime location with stronger potential for capital growth, but the rental yields are often lower.

For most people starting out, focusing on cash flow is the smarter, less risky play. Diversifying across a couple of lower-cost properties is a much safer way to build a sustainable portfolio from the ground up.

How Do I Find Those Elusive "Below Market Value" Deals?

Finding a genuine Below Market Value (BMV) deal isn't about luck; it's about proactive, consistent effort and building the right relationships. They don't just land in your inbox.

Here's where the real work happens:

- Get Friendly with Agents: Don't just be another name on a mailing list. Build proper connections with local estate agents. Show them you're a serious buyer who can make a decision and move quickly when the right deal comes along. They'll remember you when a motivated seller appears.

- Look for the 'Ugly Ducklings': Actively search for properties that need work. A tired kitchen, a dated bathroom, or an overgrown garden will put off most homebuyers, but for an investor, that's where the value is. These properties give you a chance to add value through refurbishment.

- Head to the Auctions: Property auctions are a fantastic source for finding motivated sellers and potential bargains. Just be warned: you absolutely must do all your due diligence before the auction day. Bidding is legally binding.

- Work with a Sourcer: A good, reputable property sourcer can be worth their weight in gold. They often have access to off-market opportunities you'd never find on the open market.

Ready to analyse deals faster and with greater accuracy? DealSheet AI turns property listings into comprehensive investment reports in seconds, handling all the complex UK tax rules and calculations for you. Download DealSheet AI on the App Store and start your free trial today.