How to Finance Property Development in the UK for 2026

How to Finance Property Development in the UK for 2026

Figuring out how to finance property development in the UK for 2026 is about more than just finding a lender; it's about structuring the right mix of funding to make your project a reality. The most effective strategy involves combining different layers of finance: typically, senior debt covers 60-70% of costs, mezzanine finance or preferred equity adds another 10-20%, and your own cash (developer equity) makes up the rest. This guide will walk you through building this "capital stack" to secure the funding you need. To ensure your proposals are viable from the start, use a tool like the DealSheet AI app to accurately model and stress-test your numbers.

Understanding the Capital Stack

For any developer in the UK, this is ground zero. You can't get a project funded without mastering the capital stack.

Think of it as a layered cake of money. Each layer represents a different type of finance with its own risk profile and what it expects in return. Getting this structure right is non-negotiable if you want to get your scheme off the ground.

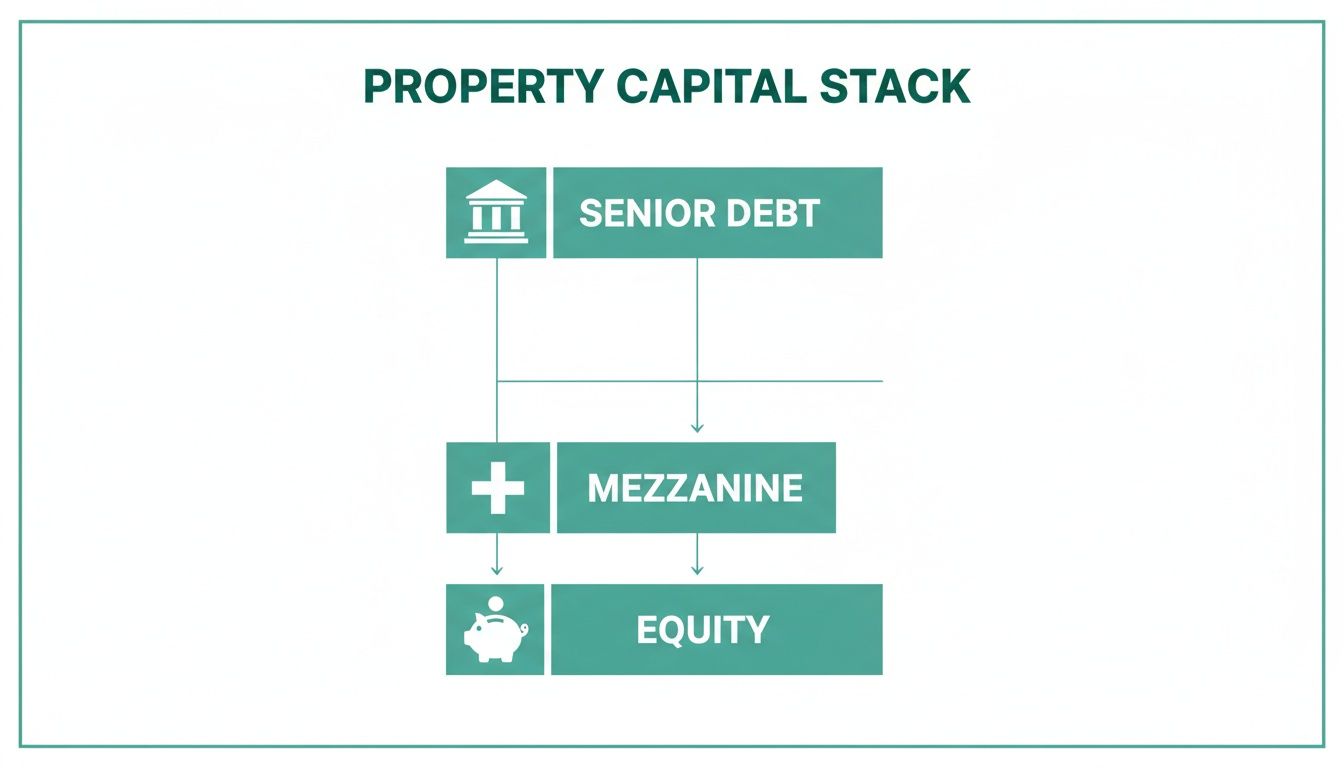

At the bottom, you have senior debt. This is the biggest and cheapest slice of the funding pie, your primary loan from a bank or specialist development lender. It's secured against the property, making it the least risky for them, which is why it comes with the lowest interest rate.

The next layer up is often mezzanine finance, a hybrid of debt and equity. It's pricier than your senior loan but cheaper than giving away a chunk of the profit. It's there to bridge the gap between what the senior lender will give you and the cash you have available.

Finally, at the very top, sits your developer equity. This is your skin in the game—the first money in and the last money out. It's the highest risk, but also takes the highest reward.

Visualising the Funding Layers

To really see how this fits together, the diagram below shows the classic hierarchy.

This visual makes one thing crystal clear: as you move up the stack from senior debt to your own equity, the cost of that money goes up. Why? Because the risk goes up with it.

Lenders need to see a rock-solid financial model that proves how every single layer will be repaid. A miscalculation anywhere in your appraisal can kill the deal before it even starts. This guide will walk you through each piece, helping you build a proposal that's not just compelling, but genuinely fundable.

The UK Property Development Capital Stack Explained

To summarise, here's a quick-glance table breaking down the typical layers you'll encounter when structuring your development finance. It maps out where the money comes from, how much you can expect from each source, and the risk level associated with it.

| Financing Layer | Typical % of Total Project Cost | Risk Level | Source of Funds |

|---|---|---|---|

| Senior Debt | 60% - 70% | Low | High Street Banks, Challenger Banks, Specialist Lenders |

| Mezzanine Finance | 10% - 20% | Medium | Specialist Mezzanine Funds, Private Lenders |

| Preferred Equity | 10% - 20% | Medium-High | Private Equity Funds, High-Net-Worth Individuals |

| Developer Equity | 10% - 20% | High | Developer's Own Cash, Joint Venture Partners, Family Offices |

Understanding this structure is the first step towards presenting a credible and professional funding application. It shows lenders you understand their position and have structured the deal in a way that aligns everyone's interests.

Getting to Grips With the Current UK Development Finance Market

If you're trying to finance a property development in 2026, the first thing to grasp is that the lending landscape has fundamentally shifted. The old dynamic—where you went cap-in-hand to a high street bank—is long gone. In its place is a far more diverse and competitive environment, dominated by a growing class of specialist, alternative lenders. For a savvy developer, this is a huge opportunity.

The overly cautious, post-financial-crisis mindset is finally fading. What's emerged is a lively marketplace where specialist lenders and powerful debt funds are hungry to deploy capital. These players are typically more agile and have a real appetite for the kind of complex or non-standard projects that would make a high street bank's computer say 'no'. In short, you've got more choice and a better shot at flexible terms, provided your deal stacks up.

The New Players on the Block

While traditional banks are still a major source of funding, they're no longer the only game in town. Debt funds, in particular, have muscled in to become serious players, especially in the residential development space. Often backed by big institutional money, they can move fast and create bespoke funding packages that are genuinely tailored to your project's needs.

This has shaken things up, creating a much healthier and more competitive interest rate environment. That's great news for developers. The trick is knowing how to pitch your project to this varied audience. It's no longer a one-size-fits-all game; you have to match your funding request to the lender's specific risk appetite and the kind of deals they actually want to do.

The key takeaway for 2026 is that alternative lenders aren't just a Plan B anymore. For a huge number of developers, they're the first port of call, offering the speed, flexibility, and deep sector knowledge that mainstream banks often lack.

What the Market Is Telling You

Recent data paints a clear picture of this evolution. Margins in the UK residential development finance market dipped below 500 basis points in 2025 for the first time since 2020. At the same time, new lending for commercial real estate shot up by 33% in the first half of the year, with development finance being a major driver, accounting for 22% of all new loans.

Here's the kicker: debt funds now provide 32% of all residential development funding. That's not a niche—that's a huge slice of the market.

This data isn't just academic; it's your strategic roadmap. It shows that lenders have capital and are actively looking for good development projects to back. Your job is to make sure your project is the one they can't ignore.

Here's how to position your deal to get funded in this climate:

- Nail Your Exit Strategy: Lenders need to see a clear and believable way out. Whether you're planning to sell the finished units (build-to-sell) or hold and rent them (build-to-rent), your financial models have to prove that the exit is rock-solid.

- De-Risk Everything You Can: Show them you've already tackled the big hurdles. This means having planning permission secured, a fixed-price contract with a reputable builder locked in, or even getting a chunk of the units pre-sold.

- Your Cost Plan Must Be Bulletproof: With material and labour costs still a major variable, a detailed and fully substantiated cost plan is non-negotiable. Lenders will pick apart your contingencies, so make sure they're robust. For more on this, check out our deep dive into understanding UK building costs per square metre.

What Lenders Are Hungry For in 2026

So, what kind of deals are actually getting the green light right now? While every lender has their own focus, a few clear trends have emerged.

There is enormous appetite for funding residential schemes, especially in regions with proven demand and solid economic fundamentals. Small-to-medium-sized projects—think 5-50 units—are often the sweet spot for specialist lenders. They're large enough to be profitable but not so huge they require a complex syndicated loan.

Another big factor is sustainability. Projects with strong green credentials, like high EPC ratings, are increasingly catching lenders' attention. This isn't just for show; lenders have their own Environmental, Social, and Governance (ESG) targets to hit. By aligning your project with these trends, you're not just building for the future—you're significantly boosting your chances of getting the funding you need to get spades in the ground.

Getting to Grips With Your Core Funding Options

To get a development project funded in the UK, you have to speak the lender's language. It's not about complex jargon; it's about knowing which funding tools to reach for and when. Let's break down the four pillars of development finance so you know exactly how to build your deal.

Each type of finance has a specific job, a different price tag, and slots into your "capital stack" in a unique way. Getting this right isn't just an academic exercise—it's the key to structuring a deal that gets approved and, more importantly, stays profitable.

Senior Debt: The Workhorse of Development Finance

Think of senior debt as the foundation of your entire funding package. It's the largest and cheapest loan you'll get, usually from a high street bank, a challenger bank, or a specialist development lender. In simple terms, it's the main mortgage for your project.

This lender has the first charge over the property, meaning if anything goes south, they get paid back first. Because they're in the least risky position, they offer you the lowest interest rate.

A senior debt facility typically covers a percentage of your total project costs, known as the Loan to Cost (LTC). For a typical ground-up development in 2026, lenders are offering up to 65% LTC. For heavy refurbs, you might get that stretched to 75%. The rest has to come from your pocket or other funding sources.

Bridging Loans: Your Tool for Speed and Agility

Bridging loans are all about speed. They are short-term loans designed to 'bridge' a gap until you can arrange longer-term finance or sell the asset. They are the perfect solution when you need to move faster than a traditional lender can.

Picture this: you've just won a site at auction. The hammer falls, and you have just 28 days to complete the purchase. A normal development loan application takes months. A bridging lender, however, can often get funds to you in a matter of weeks, sometimes even days. That speed is what you're paying for.

But this convenience isn't cheap. Bridging loans carry higher monthly interest rates and come with hefty arrangement and exit fees. They're not a long-term plan but an invaluable tool for grabbing an opportunity. You'll need a cast-iron exit strategy—like refinancing onto a development loan or a quick sale—to get the lender comfortable.

If you're facing this kind of time pressure, you can model the costs accurately using our detailed guide and UK bridging loan calculator.

Mezzanine Finance: The Critical Gap-Filler

So, your senior debt lender has offered 65% of the project cost, but you only have the equity to cover 15%. That leaves a 20% funding gap. What do you do? This is exactly where mezzanine finance steps in.

"Mezz," as it's often called, is a second-charge loan that sits behind the senior debt. It's riskier for the lender because they only get their money back after the senior lender has been fully repaid. Naturally, that higher risk means a higher interest rate for you.

By plugging this funding gap, mezzanine finance can be the difference between a project getting off the ground and a missed opportunity. It lets you take on much larger schemes than your own cash would otherwise allow, stretching your capital further.

A typical mezz loan can push your total borrowing from 65% LTC right up to 85% or even 90% LTC. The interest is usually 'rolled up' and paid from sales proceeds at the end of the project, which is great for your cash flow during the build.

Joint Venture Equity: The Partnership Route

Sometimes, the funding gap is just too big for mezzanine finance to fill. Or perhaps you're a newer developer who needs to bring in experience as well as cash. This is when a Joint Venture (JV) partnership becomes a fantastic option.

In a JV, you partner with an individual or a company who provides the equity you're missing. In return, they take a share of the project's profit. This isn't a loan; it's a true partnership. Your JV partner is sharing the risk with you, so they'll expect a significant slice of the profits—often a 50/50 split after all costs and loans are paid off.

The huge advantage is that a JV can enable you to do a project with very little of your own money in. The trade-off, of course, is giving away a large chunk of the profit. A successful JV always comes down to a rock-solid partnership agreement that clearly defines roles, responsibilities, and the profit split right from the start.

Comparing UK Property Development Funding Types

To make sense of these options at a glance, the table below breaks down their core features. It helps you see not just what they are, but where they fit.

| Funding Type | Typical LTC/LTV | Interest Rate Range | Best For |

|---|---|---|---|

| Senior Debt | 60-75% LTC | 5% - 8% per annum | The main funding for any standard development project. |

| Bridging Loan | Up to 75% LTV | 0.7% - 1.5% per month | Securing auction properties or land quickly before arranging development finance. |

| Mezzanine Finance | Up to 90% LTC (combined) | 15% - 25% per annum | Plugging the gap between your senior debt and your available equity. |

| JV Equity | Up to 100% of costs (via partner) | N/A (Profit Share) | Projects where you have a significant equity shortfall or need an experienced partner. |

Understanding these fundamental building blocks is the first step. The real art lies in knowing how to stack them together to create a funding structure that works for your specific project, your risk appetite, and your profit goals.

Building a Lender-Ready Funding Proposal

A fantastic development idea and a prime site are a great start. But they won't get you funded.

Lenders don't back ideas; they back meticulously planned, de-risked proposals. Your funding submission is far more than a pile of documents. It's the story of your project, and it needs to be compelling, credible, and answer every question before it's even asked.

To get your proposal to the top of the pile, you have to think like an underwriter. They're looking for a clear narrative that proves your competence, the project's viability, and a rock-solid exit plan. This is how you build that narrative, piece by piece.

The Core Components of Your Proposal

Your funding pack needs to be a comprehensive and professional reflection of your project. Cobbling together a few spreadsheets and a floor plan simply won't cut it. A lender-ready proposal has to be organised, detailed, and leave no room for doubt.

Here are the non-negotiable elements every lender will expect to see:

- Developer CV and Team Experience: This is where you showcase your track record. Include a summary of completed projects, highlighting their GDV, profit, and timelines. If you're light on personal experience, then detail the expertise of your professional team—architect, builder, project manager—to build that crucial confidence.

- Detailed Project Summary: Think of this as your executive summary. It should concisely outline the project, the location, planning status, the proposed scheme, and the total funding you need.

- Full Financial Appraisal: This is the absolute heart of your proposal. It must include a detailed breakdown of all costs (land, construction, professional fees, finance costs, contingency) and a thorough analysis of the Gross Development Value (GDV), backed up by solid comparable evidence.

- Cash Flow Forecast: A month-by-month cash flow is essential. It shows the lender exactly when you'll need to draw down funds and proves you have a firm grip on the project's financial management.

Proving Your Numbers and Your Exit

One of the most common mistakes developers make is presenting figures without backing them up. Your Gross Development Value (GDV) isn't just a number you hope to achieve; it must be substantiated with hard evidence. You need to include recent sales data for comparable properties in the area from reputable sources like the Land Registry or major property portals.

Likewise, your build costs have to be based on a detailed schedule of works, ideally from a quantity surveyor or supported by fixed-price quotes from your main contractor. A vague 'per square metre' estimate is a massive red flag for any experienced underwriter. Accurately calculating your potential returns is critical, and our guide on using a UK property ROI calculator can provide a solid framework for this.

The credibility of your entire proposal hinges on the quality of your cost plan and GDV analysis. If a lender can pick holes in these numbers, they will assume the rest of your proposal is just as weak.

Your exit strategy must be just as well-defined. If you plan to sell the units ('build-to-sell'), who is your target market? Which local estate agents will you be using, and what is their honest opinion on your projected sales values?

If you intend to hold the properties and refinance onto a buy-to-let mortgage ('build-to-rent'), you'll need to provide a rental appraisal and evidence that the finished scheme will meet the stress tests of long-term lenders.

Navigating a Competitive Funding Landscape

Even with a perfect proposal, securing finance remains a huge hurdle. Recent market analysis shows a challenging environment for UK developers. The 2025 Developer Survey highlights that while 52% of developers have over a decade of experience, access to funding and planning delays are the top barriers to growth.

With 58% of developers focused on new builds and many others on refurbishments, the competition for lender attention is fierce. This data underscores the absolute necessity of presenting a meticulous, conservative, and well-structured funding package to stand out. You can learn more about the key findings from the latest developer survey.

In this climate, simply knowing how to finance property development isn't enough. You must present a case that is superior to the dozens of others a lender will see that week. Your proposal is your primary tool to make that happen.

Exploring Alternative and Specialist Finance Routes

While the traditional capital stack is the backbone of most property development deals, the savviest developers I know are always looking beyond it. In today's market, understanding how to tap into alternative and specialist finance can give you a serious competitive edge.

These aren't just fringe ideas anymore. They are legitimate funding channels that can complement or even completely replace conventional loans. More importantly, they often bring a level of flexibility that opens the door to projects that a high-street bank simply wouldn't touch.

The Rise of Peer-to-Peer and Crowdfunding Platforms

Over the last few years, Peer-to-Peer (P2P) lending and property crowdfunding have well and truly come of age. They've moved from the fringes to become genuine forces in the UK development finance market, connecting developers directly with a deep pool of individual and institutional investors.

For developers, this often means quicker decisions and more pragmatic lending criteria. The big win is that they cut out the traditional bank as the middleman. P2P platforms, in particular, have carved out a niche in smaller residential schemes, making them a fantastic option for projects with a Gross Development Value (GDV) under £5 million.

So, how do they actually work?

- Peer-to-Peer (P2P) Lending: This feels a lot like applying for a standard loan. The platform vets your project, and if it gets the green light, your loan opportunity is listed for its network of investors to fund collectively.

- Property Crowdfunding (Equity): Instead of taking on debt, you're selling a stake. Investors get equity in your Special Purpose Vehicle (SPV), becoming shareholders who share in the risk but also in the potential upside when the project is sold.

The key here is to do your homework. Look for established platforms with a proven track record of successfully funded and completed projects. Dig into their fee structures and make sure you understand their specific lending appetite before you waste time on an application.

Tapping into Government Schemes and Affordable Housing

This is a huge area, especially for developers who want to build with a social impact. Government-backed funding for affordable housing is designed to get more homes built for rent and shared ownership, offering grants and favourable loans to developers who can help hit those targets.

Don't underestimate the scale here. Private Registered Providers (PRPs) invested a staggering £13.6 billion in new housing in the year to March 2025. The sector's total borrowing facilities hit an enormous £135.5 billion, which tells you just how robust and diverse its financial backing really is. You can dig into the official data on the financing of affordable housing on the UK government's website.

Partnering with a Housing Association or even becoming a Registered Provider yourself can unlock these substantial funding streams. Yes, it adds a layer of regulatory compliance, but it also gives you a secure exit and massively reduces your sales risk.

Private Investors and Family Offices

Beyond the online platforms and government bodies lies the world of private capital. High-net-worth individuals, angel investors, and family offices are constantly on the lookout for well-structured property deals that can deliver attractive returns. This is relationship-based funding in its purest form.

Unlike an institution, a private investor might back you based on your character, your vision, and the story behind the project—not just whether you tick every box on a checklist. Approaching them, however, requires a completely different mindset. It's less of an application and more of a professional pitch.

Building your network is everything. Get yourself to property events, join professional bodies like the RICS, and leverage your existing relationships with solicitors and accountants. A warm introduction is infinitely more powerful than a cold email. You'll need an immaculate business plan and total transparency on the risks and potential rewards. This route can be particularly effective for niche projects, like those we detailed in our guide on student accommodation as an investment. Ultimately, success here comes down to building trust and proving you can deliver on your promises.

Your UK Property Development Finance Questions Answered

As you get deeper into financing a development, a few key questions always bubble to the surface. We hear them from developers all the time. Let's tackle the big ones head-on with some straight answers.

How Much of My Own Money Do I Actually Need?

This is the big one. Almost every developer asks it, and the honest answer is you'll always need some of your own capital in the deal. Lenders call it your 'equity' or 'skin in the game'—they need to see you're sharing the risk, not just borrowing theirs.

For most UK projects in 2026, you should expect to put in between 10% and 30% of the total project costs. But this doesn't always have to be a lump of cash sitting in the bank.

Your contribution can come in a few different forms:

- Cash Equity: This is the most straightforward. It's your direct cash injection into the deal.

- Land Equity: If you already own the development site outright (or have a lot of equity in it), this can often be used as your contribution. The land's value is effectively your opening stake.

- Waived Fees: Sometimes, if you're a built-environment professional like an architect or project manager, you can structure the deal so the value of your waived fees counts towards your equity stake.

What Is the Difference Between LTV and LTC?

Getting Loan to Value (LTV) and Loan to Cost (LTC) mixed up is a common and costly mistake. They sound similar but measure two completely different things, and lenders use both to gauge the risk of your project.

Loan to Cost (LTC) is the metric that matters most during the actual development. It's the total loan amount as a percentage of the total project costs—that's the land, the build, professional fees, and even the finance costs themselves. So, if your total project costs are £1 million and your loan is £650,000, your LTC is 65%.

Your development lender lives and breathes LTC. It tells them exactly how much of the real-world spend they are funding, which defines their immediate risk while the diggers are on site.

Loan to Value (LTV), on the other hand, is all about the end game. It's based on the project's final completed value, or Gross Development Value (GDV). If your finished scheme is worth £1.5 million and your loan is £650,000, your LTV is just over 43%. Lenders look at this to make sure there's a healthy profit margin in the deal to cover their loan comfortably.

Can I Get Development Finance with No Experience?

It's tough, but not impossible. Lenders are naturally cautious, and a first-time developer is a big unknown for them. But with the right approach, you can build a case that gets funded.

Forget trying to jump straight into a ten-unit new-build scheme. You need to build a credible track record first.

Here are a few strategies that actually work:

- Start Small: Your first project should be something like a light refurbishment or a simple 'flip'. These deals have shorter timescales, lower costs, and are much easier to get funding for. A few successful completions like this build a portfolio that lenders can see and trust.

- Partner Up: Find an experienced developer and form a Joint Venture (JV). Bringing in a partner with a proven track record instantly de-risks the project in a lender's eyes. You'll have to share the profits, but the experience and credibility you gain are invaluable.

- Assemble an All-Star Team: If you don't have the experience, hire it. A strong professional team—a reputable builder, an experienced architect, and a diligent project manager—can give a lender the confidence they need to back you. The tax side of development can also be a minefield; you can get your head around the essentials by learning more about what Stamp Duty Land Tax is in our detailed guide.

Ready to analyse your next deal with confidence? DealSheet AI helps you analyse UK property investments in seconds, turning complex data into a clear financial model. Download the app and start your free trial today.