What Is Stamp Duty Land Tax? A 2026 Guide for UK Property Investors

What Is Stamp Duty Land Tax? A 2026 Guide for UK Property Investors

So, what is Stamp Duty Land Tax (SDLT)? In short, it's a tax you pay when buying property in England and Northern Ireland, and for property investors, it's one of the most significant upfront costs you'll face. Understanding SDLT is crucial as it can often be the deciding factor in whether a deal is financially viable. This guide breaks down the rates, rules, and surcharges for 2026 to ensure you can budget with accuracy. For instant, precise calculations on your next deal, the DealSheet AI app removes all guesswork and keeps your numbers spot-on.

Decoding This Crucial Property Tax

Getting your head around stamp duty is absolutely fundamental for any serious UK property investor. It's not just another line item on a completion statement; it's a hefty cash expense that directly hits your return on investment and can dictate whether a project is even viable.

The tax is calculated on a tiered basis, meaning you pay different rates on different slices of the property's purchase price. This progressive structure is designed so that cheaper properties attract less tax. For investors, however, the calculation gets more complex due to surcharges for second homes or buy-to-let properties.

The 2026 Residential SDLT Rates

To budget for a purchase properly, you have to know the current thresholds. For 2026, the standard residential rates are structured to reflect a property's value.

A key principle of SDLT is that the rates are applied only to the portion of the property price that falls within each specific band, not the entire purchase price. This is a common point of confusion for new investors.

The thresholds have seen plenty of changes over the years. The structure of Stamp Duty Land Tax underwent major reforms in April 2025, which sent ripples across the UK property market. These changes slashed the 0% threshold from £250,000 back down to £125,000, triggering a huge rush of transactions. In fact, HMRC statistics show 77,480 more residential property transactions in March 2025 compared to the previous year. You can read a detailed analysis of the SDLT surge to see the full impact.

Getting to grips with these rules is essential, as the right approach can massively reduce your upfront costs. To see how this tax fits into the bigger picture, check out our guide on different property investment strategies in the UK.

Navigating Surcharges and Reliefs for Investors

Once you've got the standard rates down, understanding what is stamp duty land tax for an investor really means getting to grips with the various surcharges and reliefs.

These are the extra layers that can completely change your final tax bill. Getting them right is absolutely critical if you want your deal analysis to be anywhere close to accurate. The rules aren't one-size-fits-all; they're designed to draw a clear line between someone buying their main home and an investor building a portfolio. This is where the real complexity kicks in.

The 3 Percent Higher Rate Surcharge

For pretty much every property investor in the UK, the single most important rule is the Higher Rate for Additional Dwellings (HRAD). This is a 3% surcharge slapped on top of the standard SDLT rates whenever you purchase an additional property.

So, if you already own a home (anywhere in the world) and you're buying a buy-to-let, a holiday home, or a flip in England or Northern Ireland, you will almost certainly pay this extra 3%. Crucially, this applies to the entire purchase price, not just a slice of it, making it a hefty upfront cost.

- Who pays it? Individuals buying a second property and all limited companies buying a residential property (even if it's their first).

- How it works: The 3% gets added to each of the existing SDLT bands.

- Example: For the band that's normally 0% (£0 - £250,000), an investor pays 3%. For the 5% band (£250,001 - £925,000), an investor pays 8%.

Nailing this calculation is fundamental to figuring out your real profitability. For a detailed guide on how this feeds into your overall returns, check out our piece on building a buy-to-let profit calculator that accounts for every cost.

The 2 Percent Non-Resident Surcharge

There's another key surcharge, this one aimed at overseas investors. If you aren't a UK resident when you buy a residential property in England or Northern Ireland, you'll be hit with an extra 2% Non-Resident Surcharge (NRSD).

This gets added on top of all other SDLT rates, including the 3% higher rate. For an overseas investor buying an additional property, this means they could be paying a total surcharge of 5% (3% HRAD + 2% NRSD) on top of the standard bands.

Key Reliefs for Property Investors

While surcharges push the tax bill up, some reliefs can bring it down. First-Time Buyer Relief won't apply to investors (it has to be your main residence), but there are other, more powerful options on the table.

One of the most valuable tools in an investor's arsenal is Multiple Dwellings Relief (MDR). If you're buying two or more dwellings in one go, this relief can slash your SDLT bill.

MDR works by letting you calculate the tax based on the average price per dwelling, rather than the total purchase price for the whole lot. You then multiply that smaller tax figure by the number of dwellings. This often leads to huge savings, especially when you're buying a block of flats or a portfolio of houses.

It's a complex area, for sure, but it's one that savvy investors use to get a real competitive edge. Mastering these nuances is a core part of figuring out what is stamp duty land tax in a real-world investment context.

How to Calculate SDLT with Practical Investment Examples

Theory is one thing, but seeing how Stamp Duty Land Tax plays out in the real world is where the penny really drops. Let's walk through three common investor scenarios to see how the different rates, surcharges, and rules stack up. This is where you see just how much this tax can make or break a deal.

Each calculation shows how a small change in circumstance—like buying through a company or as an overseas investor—can radically change the final tax bill. For property investors, getting these numbers wrong isn't an option. It's why tools like DealSheet AI are so essential; they automate these complex sums in seconds, taking manual error out of the equation.

Example 1: UK Resident Buy-To-Let Purchase

Imagine a UK resident investor who already owns their own home. They're looking to buy a standard buy-to-let property for £300,000. Because this counts as an additional property, the 3% Higher Rate for Additional Dwellings (HRAD) surcharge kicks in on the entire purchase price.

Here's the breakdown based on the 2026 rates:

- The first £125,000: This is usually in the 0% band, but we have to add the 3% surcharge. So, £125,000 x 3% = £3,750.

- The next £125,000 (£125,001 to £250,000): This slice is in the 2% band. With the surcharge, it becomes 5%. So, £125,000 x 5% = £6,250.

- The remaining £50,000 (£250,001 to £300,000): This portion falls into the 5% band. With the surcharge, it becomes 8%. So, £50,000 x 8% = £4,000.

- Total SDLT Due: £3,750 + £6,250 + £4,000 = £14,000.

For perspective, without the surcharge, the tax would have been just £5,000. This is a perfect illustration of how the HRAD surcharge has become a major cost for typical BTL investors.

Example 2: Limited Company Buying an HMO

Now, let's switch it up. A UK-based limited company is buying a property for £450,000 in 2026, planning to convert it into a House in Multiple Occupation (HMO).

Here's the key thing to remember: limited companies automatically pay the 3% HRAD surcharge on all residential purchases, even if it's the company's very first property.

The calculation works like this:

- First £125,000 at 3% (0% + 3% surcharge) = £3,750

- Next £125,000 at 5% (2% + 3% surcharge) = £6,250

- Next £200,000 at 8% (5% + 3% surcharge) = £16,000

- Total SDLT Due: £3,750 + £6,250 + £16,000 = £26,000.

That's a serious upfront cost that needs to be baked into the HMO conversion budget and profitability analysis right from the start. You can explore these nuances further with our comprehensive Stamp Duty Land Tax calculator, which is built specifically for investor scenarios.

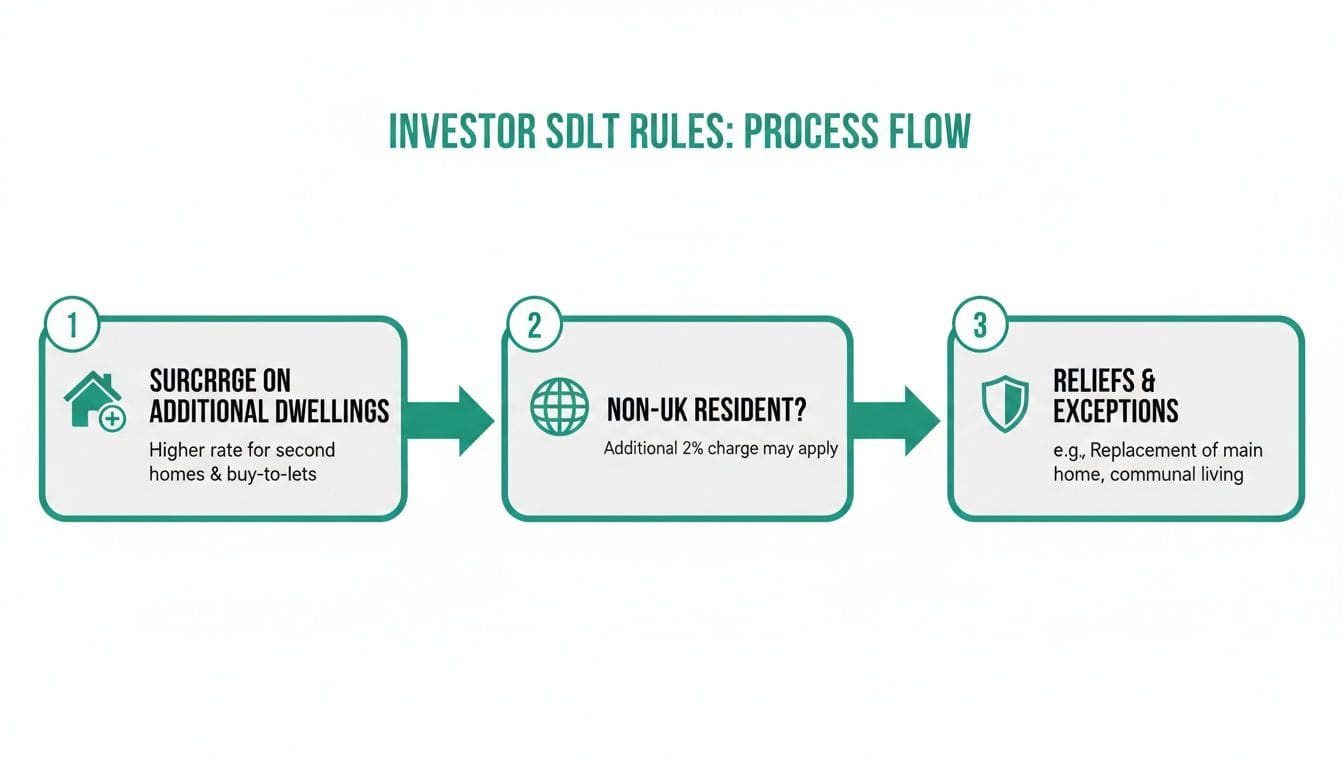

Example 3: Overseas Investor Flip Project

For our final scenario, let's look at an overseas investor who is not a UK resident. They're buying a London flat for £600,000 in 2026 to renovate and sell on—a classic 'flip' project. This situation triggers two different surcharges: the 3% HRAD and the 2% Non-Resident Surcharge (NRSD). These stack up, creating a total 5% surcharge on top of the standard rates.

This diagram shows how the different rules fit together.

As you can see, the surcharges are always the first thing to consider, before you even get to potential reliefs.

Let's do the maths for this overseas investor:

- First £125,000 at 5% (0% + 3% HRAD + 2% NRSD) = £6,250

- Next £125,000 at 7% (2% + 3% HRAD + 2% NRSD) = £8,750

- Next £350,000 at 10% (5% + 3% HRAD + 2% NRSD) = £35,000

- Total SDLT Due: £6,250 + £8,750 + £35,000 = £50,000.

This is a substantial upfront cost that directly eats into the project's profit margin. For 'flip' projects where timelines and margins are already tight, forecasting this tax bill with pinpoint accuracy is absolutely critical.

The SDLT Payment Process: Deadlines and Key Steps

Knowing how much Stamp Duty you owe is one thing; paying it on time is another. Getting the payment and filing process right is crucial for keeping your purchase on track and staying on the right side of HMRC. This isn't a step you can afford to get wrong.

The moment you complete your property purchase, a clock starts ticking. You have a strict 14-day deadline from the completion date to file your SDLT return and pay every penny you owe. This is a hard deadline, and missing it results in automatic penalties.

For most property investors, this whole process is handled by their solicitor or conveyancer. It's part of what you pay them for. They'll calculate the tax, prepare the forms, and submit everything on your behalf. Typically, they will collect the SDLT funds from you right before completion, bundled with their final invoice.

Key Administrative Steps

While your solicitor does the heavy lifting, the process still depends on you. Your job is to provide accurate information promptly and make sure the funds are ready when they ask for them.

The typical workflow looks like this:

- Calculation and Fund Collection: Your solicitor confirms the final SDLT bill and asks you to transfer the funds.

- Filing the SDLT1 Return: After you complete, they submit an SDLT1 form to HMRC. This form is a complete record of the transaction—buyer, seller, property price, and the final tax calculation.

- Payment to HMRC: The tax is paid to HMRC, ensuring it arrives within that critical 14-day window.

- Receiving the UTRN: Once HMRC accepts the return, they issue a Unique Transaction Reference Number (UTRN).

This UTRN isn't just a receipt. It's an essential piece of the puzzle. The Land Registry requires this number to officially register you as the new legal owner of the property. Without it, the legal transfer of ownership can't be finalised.

Penalties for Late Filing and Payment

HMRC is famously strict about the 14-day deadline. Failure to file and pay on time triggers automatic penalties and interest charges that can quickly escalate.

- Late Filing Penalties: You'll face a fixed penalty of £100 if the return is up to three months late, which jumps to £200 if it's any later.

- Late Payment Interest: On top of the penalty, interest is charged on the outstanding tax from the day after the payment was due until the day it's paid in full.

In tight situations where short-term funding is needed to cover upfront costs like SDLT, some investors use specialist finance. You can get a better sense of how this works by using a bridging loan calculator to model the costs.

Common SDLT Mistakes and How to Avoid Them

Even seasoned investors can get tripped up by Stamp Duty Land Tax, and a simple miscalculation can easily cost you thousands. It's one thing to know the rules, but the real test is avoiding the common pitfalls where expensive errors are made. Steering clear of these is vital for protecting your investment returns from the very first day.

The most frequent mistakes often stem from a simple misunderstanding of the surcharges and reliefs. An investor might incorrectly assume they qualify for First-Time Buyer Relief on a buy-to-let purchase (you don't), or fail to apply the 3% surcharge correctly across the entire property value. These aren't small rounding errors; they can have a massive financial impact.

Another common oversight is simply missing out on valuable reliefs. Forgetting to claim Multiple Dwellings Relief when purchasing a block of flats or several units at once, for instance, can lead to a hugely inflated tax bill. Similarly, getting the complex rules around 'linked transactions' wrong—where HMRC treats multiple purchases as a single event—can lead to an underpayment and painful future penalties.

The Impact of Stagnant Tax Thresholds

There's a quieter, more insidious issue at play, too: stagnant tax thresholds. As property prices rise with inflation, the fixed SDLT bands don't always keep pace. This phenomenon, known as fiscal drag, quietly pushes more and more properties into higher tax brackets, increasing your effective tax bill without any new laws being passed.

The historical data on this is stark. Between 2010 and 2020, the tax base for property deals grew faster than the UK's GDP, largely because rising house prices shoved more transactions over those static thresholds. The result was a tripling of SDLT revenue in just seven years during the early 2000s, driven almost entirely by this bracket creep. This makes getting your numbers right from the start even more critical. You can explore more on how property transaction taxes have evolved and the impact this has on today's market.

How to Avoid These Costly Errors

So, how do you sidestep these traps? The surest way is to remove the risk of manual error. While a good solicitor is absolutely essential for the conveyancing process, automated tools provide a crucial safety net for your own initial deal analysis.

The sheer complexity and ever-changing nature of tax legislation mean that relying on memory or an old spreadsheet is a high-risk strategy. An error in your initial underwriting can skew your entire financial forecast before you've even made an offer.

This is where a dedicated tool like DealSheet AI becomes invaluable. It's constantly updated with the latest UK tax legislation, ensuring your calculations for every single scenario are always accurate. It automatically applies the correct surcharges and considers the relevant reliefs, acting as a safeguard against the most common and costly mistakes.

This accuracy is fundamental to calculating your true profitability. To learn more about this, check out our guide on how to calculate rental yield in the UK, which is directly impacted by your initial purchase costs, including SDLT.

Your SDLT Questions Answered: An Investor's FAQ

Even when you think you've got a handle on the rules, property investing has a knack for throwing up tricky scenarios. Here are a few of the most common questions that trip investors up, with straight answers to keep you on the right track.

Can I Add SDLT to My Mortgage?

This is probably the most-asked question, and the answer is a firm no. You can't just roll the SDLT bill into your purchase mortgage. Lenders base their loan on the property's value (the loan-to-value), and they see Stamp Duty as a separate tax bill you need to settle yourself, upfront, with your own cash.

That said, experienced investors often get creative to manage the cash flow. It's not uncommon to remortgage another property in a portfolio to release the equity needed, or even use a short-term personal loan. Just be careful—while it solves an immediate cash problem, it adds another layer of debt and interest to your overall costs, so you need to weigh it up properly.

Is SDLT Due on Gifted or Inherited Properties?

In a straightforward gift, where a property is handed over with absolutely no payment or 'consideration' changing hands, you usually don't have to pay SDLT. The same goes for properties you inherit through a will.

But there's a massive exception: mortgages. If you are gifted a property but also agree to take over the existing mortgage, HMRC sees the outstanding mortgage balance as consideration. If that outstanding loan amount is over the SDLT threshold, you'll be liable for tax on that figure.

How Does SDLT Apply to Leasehold Properties?

Calculating SDLT on a leasehold purchase is a bit more involved than with a freehold. The tax isn't just on one figure; it's calculated on two separate parts of the deal:

- The Lease Premium: This is the headline purchase price you pay for the lease. It's taxed using the standard residential SDLT rates, including any surcharges for additional properties or non-resident status.

- The Net Present Value (NPV) of the Rent: This is a more complex calculation based on the total ground rent you'll pay over the life of the lease. If this NPV figure goes over the £125,000 threshold (as of 2026), a separate 1% SDLT charge kicks in on the amount above that threshold.

Is SDLT a Tax-Deductible Expense for Landlords?

Here's a crucial point that catches out a lot of new landlords: you cannot deduct your SDLT payment from your rental income as if it were a running cost, like an agent's fee or a repair bill. It won't reduce your annual Income Tax liability.

SDLT is classed as a capital cost, not an operating expense. This means it's considered part of the cost of buying the asset in the first place.

But that money isn't just lost to the taxman forever. When you eventually sell the property, you can add the SDLT amount to the initial purchase price. This increases your 'base cost', which in turn reduces your final Capital Gains Tax (CGT) bill. So, you get the tax benefit at the end of the investment journey, not during it.

Ready to analyse your next property deal with complete confidence in your tax calculations? The DealSheet AI app automatically calculates the correct SDLT for any UK investment scenario in seconds, removing the risk of costly errors. Download it from the App Store and start your free trial today at https://apps.apple.com/gb/app/dealsheet-ai/id6756220992.