The Best Property Investment Strategies UK Investors Can Use in 2024

The Best Property Investment Strategies UK Investors Can Use in 2024

The best property investment strategies UK investors use are those that align with their specific financial goals, whether that's generating consistent monthly income through Buy-to-Let or accelerating wealth through active approaches like the BRRRR method. This guide provides actionable insights into the most effective strategies, from foundational rentals to advanced commercial plays, helping you navigate the market with clarity. To accurately analyse and compare potential deals across these diverse strategies, a professional tool like the DealSheet AI app is essential for making data-driven decisions.

Choosing Your Path in UK Property Investment

Jumping into property without a clear strategy is like setting sail without a destination. The UK market is a patchwork of different opportunities, each with its own rulebook, risks, and potential rewards. The right path for you will come down to your own finances, how much risk you're comfortable with, and what you want to achieve long-term.

Some investors are drawn to the consistent, almost passive income that rental properties can generate. Others thrive on the challenge of forcing value through renovation to secure a quick profit. There's no single "best" strategy; the only one that matters is the one that fits your personal goals perfectly.

Aligning Strategy with Your Financial Goals

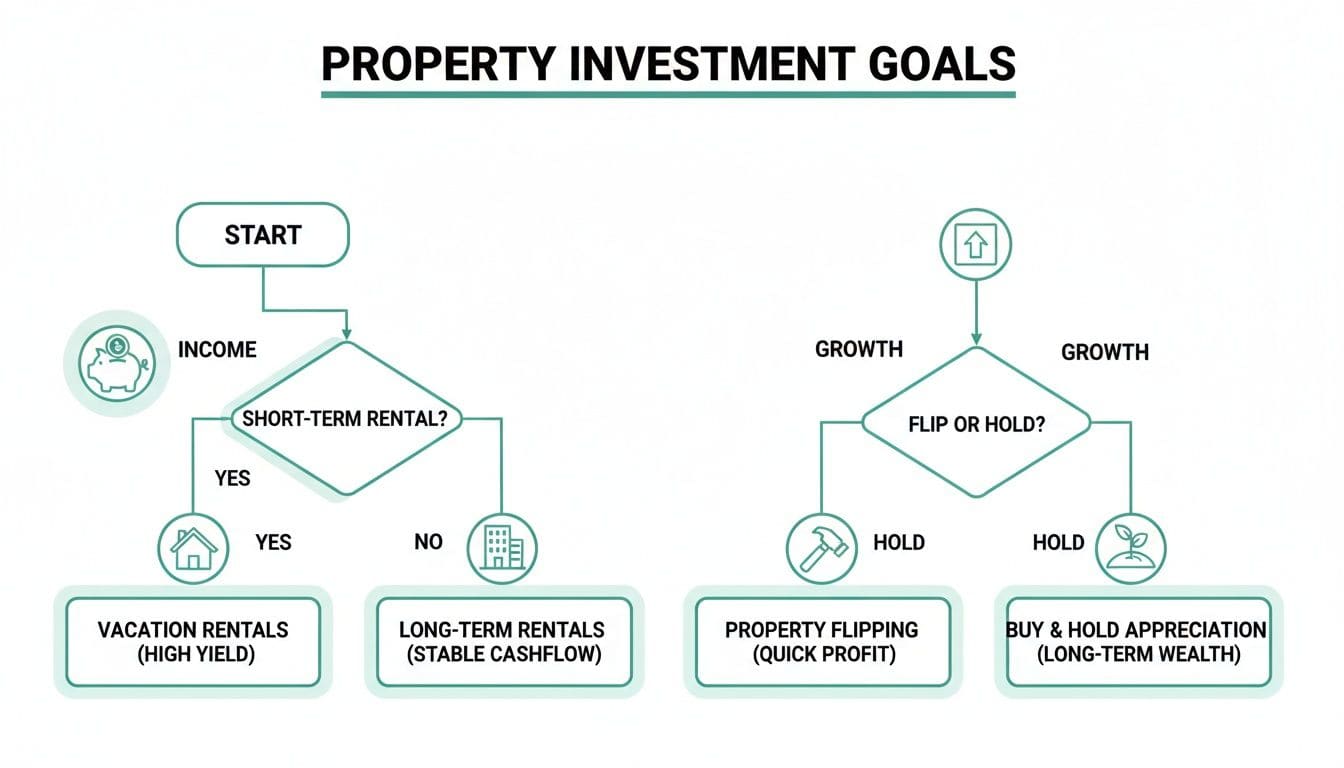

Before you even think about specific tactics, you need to be crystal clear on what you're trying to achieve. Are you aiming for monthly cash flow to top up your income? Or is your main focus on building long-term wealth through capital growth?

This simple decision tree shows how your primary goal—income or growth—points you down completely different investment avenues.

Getting this distinction right from the start helps you filter out the noise. It stops you from chasing deals that, while maybe good for someone else, simply don't fit your own portfolio plan.

From Strategy to Sourcing

Once you've settled on a strategy, the next job is finding the right deals to match it. This isn't about luck; it's about a systematic approach to sourcing properties that tick your specific boxes. Whether you need a turnkey rental or an undervalued wreck needing a full back-to-brick refurb, the quality of your deal flow will make or break your success.

A well-defined sourcing plan is just as critical as the investment strategy itself. For a much deeper dive, check out our guide on effective property deal sourcing in the UK.

The foundation of a successful property portfolio isn't just buying assets; it's buying the right assets. A clearly defined strategy acts as your compass, ensuring every acquisition moves you closer to your financial destination.

By getting clear on your goals from day one, you can confidently navigate the various property investment strategies UK investors have available, building a resilient and profitable portfolio that's tailored to your own vision.

Building Wealth with Buy-to-Let and HMOs

For most people starting out in UK property, the classic Buy-to-Let (BTL) is their first port of call. It's the most familiar of all the property investment strategies UK investors use: you buy a property and let it out to a single household or family. The appeal is timeless and comes from two directions at once – you get a steady stream of rental income each month, plus the potential for long-term capital growth as the property's value hopefully climbs over time.

Think of it as the foundation of a portfolio. It's a relatively simple model to get your head around, especially when you compare it to some of the more complex strategies we'll cover later. But don't mistake simple for easy; its success lives or dies on getting the numbers right from day one.

Understanding the Buy-to-Let Model

The BTL model is a perfect fit for investors who want a steady, fairly hands-off income stream and are playing the long game of wealth accumulation. This isn't about flipping for a quick profit; it's about patiently building equity over many years. The ideal investor is someone with a long-term mindset, who understands and is prepared for the real responsibilities of being a landlord.

Getting bogged down in the wrong metrics is a classic rookie mistake. You need to focus on what actually matters:

- Rental Yield: This is simply your annual rent as a percentage of the property's value. It's the first, most basic measure of how hard the property is working for you from an income perspective.

- Return on Investment (ROI): This is the killer metric. It calculates your net profit against the actual cash you've put in (your deposit, legal fees, any refurb costs). ROI tells you what your money is really earning.

- Cash Flow: This is the money left in your bank account each month after you've paid the mortgage, insurance, maintenance, and all other running costs. Positive cash flow is the lifeblood of a sustainable investment.

Getting the financing right can feel like a major hurdle. Lenders apply tough stress tests to BTL mortgages, checking that the rent can cover the payments even if interest rates were to shoot up. Forecasting all these numbers accurately before you even think about making an offer is absolutely vital. You can dive deeper into these calculations in our detailed guide on using a UK rental yield calculator.

Supercharging Returns with HMOs

Now, imagine taking the standard rental model and turning the volume up. That's a House in Multiple Occupation (HMO). Instead of letting a whole property to one family, you rent it out room by room to several unrelated tenants who share facilities like the kitchen and bathroom. This strategy is a favourite for student areas or cities with lots of young professionals.

The main draw of an HMO is the dramatically higher rental income. The total rent you collect from individual rooms is almost always significantly more than you'd get from a single tenancy in the same house. This can generate fantastic cash flow, often double or even triple that of a standard BTL.

An HMO can be a cash flow powerhouse, but it is not a passive investment. It transforms a property into a small-scale, service-oriented business, demanding more time, capital, and regulatory compliance than a standard BTL.

But this extra reward comes with a heavy dose of extra responsibility. HMOs are far more hands-on to manage, with higher tenant turnover and more potential for friction between housemates. They are also tangled in a web of specific regulations, including mandatory licensing from the local council, minimum room sizes, and very strict fire safety standards. Getting this wrong can lead to eye-watering fines.

Comparing BTL and HMO Investments

So, which path is right for you? It boils down to your goals, how much cash you have, and your appetite for getting your hands dirty.

| Feature | Standard Buy-to-Let (BTL) | House in Multiple Occupation (HMO) |

|---|---|---|

| Income Potential | Moderate, consistent cash flow | High, potentially 2-3x BTL cash flow |

| Management | Lower intensity, fewer tenants | High intensity, high tenant turnover |

| Regulations | Standard landlord obligations | Strict licensing and safety rules |

| Upfront Costs | Standard deposit and fees | Higher conversion & compliance costs |

| Ideal Investor | Long-term, hands-off investor | Active, cash-flow focused investor |

Underwriting either of these deals demands a forensic approach. With a BTL, you're modelling one income stream against your costs. With an HMO, you have to model multiple income streams, higher utility bills, council tax (which the landlord often pays), and factor in more frequent void periods as tenants come and go. This is where modern tools become indispensable, allowing you to run different scenarios and see the true profitability before you commit a single pound.

Accelerating Your Growth with BRRRR and Flipping

While traditional rentals build wealth with slow, steady predictability, some investors are wired for more active, high-growth approaches. Two of the most powerful property investment strategies UK investors use to get ahead faster are Buy, Refurbish, Rent, Refinance, Repeat (BRRRR) and flipping. Both revolve around adding value through renovation, but they point towards very different long-term goals.

Be warned, these strategies are not for the faint-hearted. They demand a sharp eye for a deal, an almost pessimistic accuracy in your costings, and the ability to manage a project without letting it run away from you. Get it right, though, and you can rapidly build your portfolio's equity or pull out substantial lump-sum profits, recycling your capital far quicker than with a standard buy-and-hold.

The BRRRR Method Unpacked

The BRRRR method is a cycle, designed to build a rental portfolio while leaving as little of your own cash in each deal as possible. It's a dynamic process that, in a perfect world, lets you pull out all of your initial investment to roll into the next project. Over time, you're effectively building your portfolio for free. The magic ingredient here is "forced appreciation"—you're not just waiting for the market to rise; you're forcing the property's value up yourself through smart renovation.

Here's a breakdown of the five crucial stages:

- Buy: This is where you make your money. You have to buy a property significantly below what it could be worth after a good renovation. Getting this part wrong makes the rest of the process incredibly difficult.

- Refurbish: You then carry out a strategic renovation to a high standard. The focus isn't just on making it look nice, but on improvements that genuinely add the most value—think modernising kitchens and bathrooms or reconfiguring a clunky layout.

- Rent: Next, you let the property to tenants to establish a rental income. This isn't just about cash flow; it's essential proof for the next step, as lenders need to see a proven income stream before they'll consider refinancing.

- Refinance: After a set period (usually six months to satisfy most lenders), you refinance the property with a new mortgage. Crucially, this is based on its new, higher value. This is the moment you unlock the equity you've created.

- Repeat: You take the tax-free capital released from the refinance, use it as the deposit for your next BRRRR project, and start the cycle all over again.

The whole point of BRRRR is capital recycling. In a traditional Buy-to-Let, your deposit is tied up for years. BRRRR aims to get that cash back out fast so it can be put to work on the next deal, allowing for potentially exponential portfolio growth.

The High-Stakes World of Flipping

Flipping, or 'fix-and-flip', starts the same way as BRRRR—you buy an undervalued property and you renovate it. But the endgame couldn't be more different. Instead of renting it out, you sell it on the open market as quickly as possible to crystallise a profit. It's a pure capital growth play, focused on generating a lump sum of cash in a short timeframe.

This is a high-risk, high-reward game. A successful flip can generate a profit equal to several years of rental income in just a few months. But the risks are just as significant. The market can turn on a sixpence, and a sudden downturn could wipe out your profit margin before you find a buyer. On top of that, renovation costs can easily spiral if you haven't budgeted with military precision.

Financing flips almost always means using specialist short-term lending like bridging loans, which come with higher interest rates and hefty fees. Understanding these costs is critical. You can learn more in our guide on using a bridging loan calculator to model these expenses properly before you commit.

Comparing BRRRR and Flipping Risks and Rewards

Choosing between these two active strategies really comes down to what you want: a long-term, income-producing portfolio or immediate cash profits.

| Aspect | BRRRR Strategy | Flipping Strategy |

|---|---|---|

| Primary Goal | Build a rental portfolio by recycling capital. | Generate a short-term, lump-sum profit. |

| End Result | You own a cash-flowing rental asset. | You walk away with cash after the sale. |

| Tax Implications | No Capital Gains Tax on refinance. Income Tax on rent. | Capital Gains Tax or Income Tax on profit from sale. |

| Market Risk | Lower risk from short-term market dips. | Highly exposed to market changes during the project. |

| Ideal Investor | Long-term portfolio builder focused on cash flow. | Project-focused investor seeking quick capital gains. |

Whether you're modelling a complex BRRRR deal with its tricky refinance sums or forecasting the potential profit of a flip, precision is everything. This is where tools like the DealSheet AI app become invaluable. They let you run these scenarios, track your refurb budget against your projections, and accurately forecast the final numbers to make sure your project is financially viable from day one.

Stepping Up: Niche and Commercial Investment Strategies

Once you move beyond standard residential lets, a whole world of specialised property investment strategies UK investors use to chase higher returns opens up. These approaches—think Serviced Accommodation (SA), mixed-use properties, and auction buys—can be seriously rewarding, but they demand a much more sophisticated level of analysis and hands-on management.

Let's be clear: these aren't for the passive, sit-back-and-collect-rent investor. But for those ready to handle the extra complexity, they can be incredibly lucrative.

Each strategy runs on a completely different financial engine, with unique income streams, costs, and risks. Getting the underwriting right is everything. It's the key to unlocking their potential and, more importantly, avoiding eye-wateringly expensive mistakes. This is where a versatile analysis tool becomes non-negotiable, letting you model everything from nightly SA rates to the dual-income streams of a shop with flats above.

The Hospitality Model: Serviced Accommodation

Serviced Accommodation (SA), often called short-term or holiday lets, is about renting a property on a nightly or weekly basis, just like a hotel. You're catering to tourists, business travellers, or people who need a temporary home. The big draw? The potential for massively higher income than a standard long-term rental. A property that might bring in £1,200 a month on a BTL mortgage could easily clear £3,000 in a good month as an SA.

Of course, that extra income comes at a price. Running an SA is less like being a landlord and more like running a small hospitality business. The management is intense and relentless. It involves:

- Constant Marketing: You have to keep the property visible and attractive on platforms like Airbnb and Booking.com.

- Guest Communication: Responding to enquiries, sending check-in details, and handling in-stay issues is a 24/7 gig.

- Logistics: The operational churn is huge. You're managing cleaning, laundry, and restocking between every single guest.

- Higher Costs: Your utility bills, insurance, and booking platform fees will all be substantially higher than for a simple BTL.

When you analyse an SA deal, you have to meticulously forecast occupancy rates, which can swing wildly with the seasons. You also have to budget for all the operational costs, not just the mortgage. This isn't just a property analysis; it's a full-blown business plan.

Diversifying with Mixed-Use Properties

A mixed-use property is a single building that combines commercial and residential space. The classic example is a high-street building with a shop on the ground floor and flats above. This strategy is a powerful way to diversify your income streams within a single asset. If the shop sits empty for a few months, you still have rent coming in from the flats, and vice versa.

That diversification offers a layer of security, but it also brings complexity. You're suddenly managing two completely different types of tenancies under one roof. Commercial leases are a different beast to residential agreements—often longer, more complex, and governed by different legal frameworks.

Recent market trends show why this can be so compelling. For instance, UK real estate delivered an impressive 8.1% total return over the 12 months to February 2025, with the retail sector leading the charge at 11.3%. This highlights the potential strength of the commercial part of a mixed-use building. You can dig into these market dynamics in this detailed Q2 2025 outlook.

Mixed-use properties force you to become an expert in two distinct markets at once. Success depends on your ability to understand both the local commercial demand and the residential rental landscape simultaneously.

The Thrill (and Terror) of Property Auctions

Property auctions offer a fast-paced, high-risk, high-reward way to buy property. You can find some incredible deals, often at significant discounts—think repossessions, probate sales, and unique buildings that are tough to value. The process is transparent and brutally decisive. When the hammer falls, the property is yours.

But that speed comes with serious pressure. You have to do all your due diligence—legal checks, surveys, financing—before you even think about bidding. Once that hammer falls, you are legally bound to complete the purchase, usually within 28 days. There is no backing out.

This compressed timeframe makes auctions totally unsuitable for traditional mortgage finance. Investors almost always use cash or specialist auction finance, like a bridging loan. When underwriting an auction deal, your analysis has to be lightning-fast but leave no stone unturned before you raise your paddle.

Navigating UK Property Tax and Finance

It doesn't matter how profitable your property strategy looks on paper if the taxman ends up with most of the profit. Understanding the UK's financial and legal framework isn't just a box-ticking exercise; it's the difference between a successful portfolio and an expensive hobby.

Every pound you make, from the initial purchase to the monthly rent, is subject to a specific set of rules. Getting to grips with these rules means you can structure your investments for maximum efficiency. It's about staying fully compliant while legally minimising your tax bill, ensuring the money you work so hard for actually stays in your pocket.

Key UK Property Taxes Explained

Three main taxes dominate the world of UK property investment. If you're serious about this business, these are non-negotiable.

-

Stamp Duty Land Tax (SDLT): Think of this as the entry fee. It's the tax you pay upfront when buying property or land in England and Northern Ireland. The rates are tiered, and as an investor, you'll almost always pay a higher rate than someone buying their own home. For a proper deep dive, check out our Stamp Duty Land Tax calculator guide.

-

Income Tax: This is levied on the net profit you make from renting out your property. You calculate it by taking your total rental income and then subtracting allowable expenses—things like maintenance, insurance, and letting agent fees.

-

Capital Gains Tax (CGT): When you sell an investment property for more than you paid, the profit is subject to CGT. Everyone gets a tax-free allowance, but any gains above that are taxed. Crucially, the rate for residential property is higher than for other assets.

The Section 24 Challenge

One of the biggest bombshells to hit individual landlords in recent years was the introduction of Section 24. It completely changed the game. Before this, you could deduct your full mortgage interest payments as a business expense before working out your taxable profit. Simple.

Now, that relief has been scrapped and replaced with a basic-rate tax credit of just 20%. This disproportionately hammers higher-rate taxpayers, who can no longer claim relief at their 40% or 45% tax rate. For many, it's single-handedly pushed them into a higher tax bracket and made holding property in a personal name far less attractive.

Section 24 fundamentally changed the profitability equation for individual landlords. It's the single biggest reason why so many investors now choose to purchase property through a limited company.

Limited Company (SPV) Or Personal Name?

This is now the first big decision every UK property investor has to make. Setting up a limited company, often called a Special Purpose Vehicle (SPV), has become the default move for a good reason.

Inside an SPV, the company can deduct 100% of the mortgage interest as a legitimate business expense before it pays Corporation Tax on the profits. This lets you sidestep the Section 24 problem entirely.

However, it's not a silver bullet. Mortgages for SPVs can come with slightly higher rates, and getting the profits out for your personal use means paying yourself a salary or dividends, which have their own tax implications. Buying in your personal name is administratively simpler but leaves you fully exposed to Section 24. The right answer depends entirely on your personal tax situation and what you want to achieve long-term.

Financing Your Property Investment Strategy

Your financing has to match your strategy. A standard Buy-to-Let mortgage is perfect for a long-term rental, but it's completely wrong for a fast-paced flip. For that, you'd be looking at a bridging loan to provide short-term capital for the renovation. For more complex assets like a mixed-use building, you'll need commercial finance.

Understanding the financial tools available is just as vital as understanding the tax rules. With the UK real estate market valued at USD 121.7 billion in 2024 and projected to hit USD 166.0 billion by 2030, there's enormous potential. The smartest investors will be the ones who use the right tax structures and financing to make the most of that growth.

Putting It All Together: Building Your Long-Term Portfolio

We've covered a lot of ground, exploring the most common property investment strategies UK investors have at their disposal. Now for the most important part: building a plan that actually works for you.

There's no secret "best" strategy. The right one is simply the one that fits your reality—your available cash, your stomach for risk, how much time you can realistically commit, and what you're ultimately trying to achieve.

Choosing your path starts with a bit of honest self-assessment. Are you looking for a steady, hands-off income stream where you can set it and largely forget it? Or are you the type who wants to get stuck into a project, force the value up, and get your cash back out to go again? The answer is what steers you towards a classic Buy-to-Let or a more intense BRRRR project.

Matching the Strategy to Your Investor Profile

To get a clearer picture, think about where you land on a few key spectrums. This isn't about right or wrong; it's about finding the vehicle that will get you to your destination without breaking down.

- How much cash do you have to play with? Have you got a hefty deposit ready for a standard BTL, or are you starting with less and need a strategy like BRRRR that's designed to pull your initial stake back out?

- How much time can you actually commit? Can you dedicate serious hours to managing a flip or running a Serviced Accommodation unit, or does your day job demand something far more passive?

- What's your appetite for risk? Are you comfortable taking on the market exposure and budget unknowns of a flip, or do you sleep better at night with the relative stability of a long-term rental asset?

Answering these questions honestly will immediately filter out the strategies that are a bad fit, helping you build a portfolio that works for you, not against you.

The Foundations of Success Never Change

No matter which path you choose, the non-negotiables for success are always the same. Every single deal, from a simple single-let to a complex mixed-use development, must be built on rock-solid due diligence and precise financial analysis. In property, guesswork is just a fast track to expensive mistakes.

Staying on top of market trends is just as crucial. For instance, in 2024, investment in the UK's 'living sector'—which includes build-to-rent (BTR)—shot up by 5% year-on-year to a massive £13.9 billion. This tells us that big institutions are hungry for professionally managed rental assets, especially in cities with housing shortages. It's a strong signal that BTR-focused portfolios could offer some very steady, reliable returns. You can dig into the numbers yourself by reading the full UK living market analysis here.

Your success as an investor isn't defined by the strategy you pick. It's defined by the rigour with which you execute it. Consistent, accurate deal analysis is the one skill that underpins every single profitable property portfolio.

Ultimately, building a lasting portfolio is a marathon, not a sprint. Whether you're buying your first rental or adding to a growing collection, the key is to have a clear plan. This is where professional analysis tools like DealSheet AI become so important. They give you the power to evaluate every opportunity with the same rigour and confidence, letting you execute your chosen property investment strategies UK with the precision that success demands.

Got Questions? We've Got Answers

Stepping into the world of UK property investment can feel like learning a new language, and it's natural to have questions. Here are some of the most common ones we hear, broken down with straight-talking answers.

What Is the Best Property Investment Strategy for a Beginner in the UK?

For most people starting out, a standard Buy-to-Let (BTL) is the cleanest entry point. It's far less complicated than running an HMO or a Serviced Accommodation business, and it doesn't demand the deep pockets or project management skills of a full BRRRR.

A simple BTL is your training ground. It lets you get to grips with the fundamentals – finding tenants, managing a property, and understanding the real-world finances of being a landlord – without the intense pressure of major refurbishments or constant guest turnover. The key is to pick an area with solid, predictable rental demand. That way, you can build your confidence and experience on a stable foundation.

How Much Money Do I Need to Start Investing in UK Property?

There's no single answer here; it really depends on where you buy and what strategy you choose. For a standard buy-to-let mortgage, you'll need a deposit of at least 25% of the property's value. On top of that, you need to budget for Stamp Duty, legal fees, and a healthy contingency fund for unexpected costs.

In some of the lower-cost areas across the UK, you might be able to get on the ladder with a pot of around £30,000-£40,000. But if you're looking at more capital-hungry property investment strategies UK investors often favour, like flipping a house or doing a BRRRR in a pricier region, your starting cash could easily need to be north of £100,000.

Should I Buy Property Through a Limited Company or as an Individual?

This is one of the most important decisions you'll make, and it has huge tax implications. There's no one-size-fits-all answer. Buying in your personal name is administratively simpler, but you'll be hit by the Section 24 mortgage interest restrictions, which can seriously dent your profits if you're a higher-rate taxpayer.

A limited company, often called a Special Purpose Vehicle (SPV), lets you offset 100% of your mortgage interest against your rental income before you pay Corporation Tax. For many higher-rate taxpayers aiming to build a portfolio, this is a much more tax-efficient route.

But it's not a magic bullet. Mortgages for companies can come with higher interest rates and fees, and getting money out of the company for your personal use isn't always straightforward. Before you do anything, you absolutely must get advice from a qualified property accountant. They can help you figure out the right structure for your specific situation and your long-term goals.

Ready to analyse your next deal with the confidence and precision of a pro? Download the DealSheet AI app and analyse any UK property strategy in seconds, not hours. Get started with DealSheet AI on the App Store