A Guide to Student Accommodation as an Investment in the UK for 2026

A Guide to Student Accommodation as an Investment in the UK for 2026

Is student accommodation as an investment a smart move for your UK portfolio in 2026? The short answer is yes. With university applications projected to hit record levels and a severe shortage of available housing, the UK student property market offers a resilient, high-yielding opportunity for savvy investors. This guide provides the actionable insights you need to navigate this sector, from choosing between HMOs and PBSA to mastering the financials. To analyse deals and validate your numbers instantly, the sharpest investors use the DealSheet AI app.

Why Student Accommodation Excels in the UK Market

Investing in student property isn't just about collecting rent; it's about plugging into a market with robust growth that consistently outperforms vanilla buy-to-lets. This isn't some fleeting trend. It's a long-term structural shift powered by rock-solid economic drivers.

The real appeal lies in its defensive qualities. Education is non-discretionary, which means demand for housing stays strong even when the wider economy wobbles. This creates a dependable, ever-renewing tenant base, year after year. As more students flock to UK universities, the need for quality housing only intensifies, pushing both rental income and property values upwards. For an investor, that translates into reliable cash flow and the potential for serious capital appreciation.

The Core Drivers of Demand

Several key factors are converging to make student accommodation as an investment particularly compelling for 2026 and beyond. Get your head around these, and you'll see the opportunity clearly.

- Record University Applications: The number of young people applying to UK universities is at an all-time high, and forecasts show this is set to continue climbing towards 2030.

- Growing International Student Numbers: Despite recent policy noise, the UK remains a top global destination for higher education. This brings a steady stream of international students who need a place to live from day one.

- A Squeezed Rental Market: The traditional private rented sector is tightening. Increasing regulation, stricter energy efficiency standards, and the end of fixed-term tenancies are pushing some landlords out. This shrinks the overall supply of available housing, including homes that students once rented.

The UK is facing a huge supply crunch. Projections for 2026 show a potential shortfall of over 620,000 student beds against a student population of 2.2 million. This fundamental imbalance is a powerful engine for rental growth and sustained high yields.

Before we delve into the numbers, let's summarise the core strengths of this asset class.

Why Student Accommodation Investment Excels

This table gives a quick snapshot of the key advantages driving the UK student property market.

| Investment Driver | Market Impact | Investor Opportunity |

|---|---|---|

| High & Growing Demand | Record university applications and international student numbers create a consistent, renewing tenant pool. | Reliable occupancy rates and reduced void periods compared to traditional lets. |

| Structural Undersupply | A projected shortfall of over 620,000 beds by 2026 puts intense upward pressure on rents. | Strong potential for rental growth that outpaces inflation and other property sectors. |

| Defensive Qualities | Education is non-discretionary, making the sector resilient to economic downturns. | Stable income stream and lower volatility during periods of market uncertainty. |

| Higher Yields | The demand-supply imbalance and per-room rental model often result in superior net yields. | Enhanced cash flow and a quicker return on invested capital. |

In short, the fundamentals are incredibly strong, offering a compelling blend of income stability and growth potential that's hard to find elsewhere.

A Market Underpinned by Hard Data

The numbers don't lie. A looming supply crisis positions UK student accommodation as an investment you can't afford to ignore, with UCAS forecasting that university applications could hit 1 million by 2030. This intense demand is already driving rents, with university-owned accommodation seeing a 4.44% increase compared to just 1.16% in the private sector, sustaining yields around 5.25% in prime regions. For a deeper dive into these trends, check out the latest analysis from Charles Russell Speechlys.

This powerful mix of high demand and short supply makes a compelling case. But success hinges on running your numbers properly. You can learn more by checking out our guide on what constitutes a good ROI on a rental property.

This is where the right tools become critical. By automating the complex calculations, an app like DealSheet AI instantly shows you the key metrics like ROI and cash flow, letting you make fast, data-driven decisions instead of getting bogged down in spreadsheets.

Understanding the UK Student Accommodation Market

To get student accommodation as an investment right, you need to look past the headlines and get a feel for the real forces at play. This isn't your average property sector. It's a market driven by relentless, predictable demand from a growing student population, giving you a fresh, reliable pool of tenants every single year. That's a dynamic most traditional landlords can only dream of.

But it's not just a numbers game. The whole landscape is shifting under our feet. We're seeing a massive pivot away from the traditional student digs—think shared houses, or Houses in Multiple Occupation (HMOs)—and towards professionally managed, Purpose-Built Student Accommodation (PBSA). This isn't a fad; it's a fundamental change driven by students wanting better quality rooms, decent amenities, and the sheer convenience of having all their bills rolled into one.

The Big Shift From HMOs to PBSA

This move towards purpose-built blocks isn't just happening by chance. It's being actively pushed along by local council policies. Many university cities have brought in Article 4 Directions, a planning restriction that makes it much harder to create new HMOs in specific areas.

So, what does that actually mean for an investor?

- A Cap on New HMOs: Article 4 effectively stops you from turning a standard family home into a new student house, putting a ceiling on the supply of traditional student lets.

- The Value of Existing HMOs Goes Up: If you already own a licensed HMO in an Article 4 area, you're in a strong position. With new competition choked off, your asset often becomes more valuable.

- A Clear Path to PBSA: With the HMO route getting trickier and more regulated, both students and investors are naturally gravitating towards the PBSA model.

This regulatory squeeze creates a fascinating market dynamic. It protects the value of established student properties while funnelling new money and tenant demand towards modern, purpose-built developments.

The Power of Institutional Investment

One of the clearest signs of a healthy, mature market is when the "big money" gets involved. Institutional investors—we're talking pension funds and massive investment firms—don't throw cash around lightly. They do their homework, and they only pile into markets with rock-solid, long-term fundamentals. Right now, they are pouring capital into UK PBSA.

This flood of institutional cash is a massive vote of confidence. It's a signal that the experts see a stable, high-growth future for student accommodation as an investment. When these major players move in, it tends to professionalise the whole sector, raising standards and cementing its reputation as a proper, mainstream asset class.

This isn't just theory; the data backs it up. In the second quarter of 2025 alone, investors ploughed a staggering £830 million into UK PBSA. Total transactions hit £2.8 billion in the first nine months of the year, with yields holding firm—a clear sign of robust confidence. You can see more insights from this Knight Frank report on CoStar.

Why Rental Growth is Outpacing the Norm

When you combine surging demand, supply being held back by regulations, and a general move towards higher-quality living, you get a direct impact on rents. Student rental growth is consistently outstripping the wider private rental market. Landlords in this niche are dealing with a captive audience that has to find housing for the academic year, which often means less haggling on price and properties getting snapped up quickly.

On top of that, the costs to develop new PBSA are seriously high, which creates a natural barrier preventing a flood of new supply. You can get a better sense of the numbers involved by reading our guide on understanding UK building costs per square metre. This ensures that the existing supply-demand imbalance won't be fixed overnight, helping to protect rental incomes for years to come. For a private investor, that dynamic is a strong foundation to build a profitable portfolio on.

Choosing Your Investment Strategy: PBSA vs HMOs

Once you're convinced by the fundamentals of student property, the next big question is deciding what kind of investor you want to be. This choice really boils down to two main paths: the modern, professionally managed world of Purpose-Built Student Accommodation (PBSA), or the traditional, high-yield territory of the House in Multiple Occupation (HMO).

Each strategy offers a totally different blend of risk, reward, and hands-on involvement. Your decision will shape everything from your budget and financing options to your day-to-day life as a landlord. Are you after a more passive, hands-off income stream, or are you prepared to roll up your sleeves for potentially much higher returns? Answering this is the first step to making sure your investment actually fits your goals.

The Case for Purpose-Built Student Accommodation (PBSA)

PBSA refers to those large-scale developments designed and built specifically for students. Think slick, modern apartment blocks with en-suite rooms, shared gyms, study areas, and all-inclusive bills. For an investor, the appeal is obvious: it's a largely hands-off model.

- Professional Management: The entire building is typically run by a single operator. They handle everything from finding tenants and collecting rent to maintenance and security.

- Premium Rents: The better quality and all-in amenities mean you can charge higher rents compared to a room in a traditional shared house.

- Fewer Regulatory Headaches: Since these blocks are purpose-built, they're designed to meet all the necessary safety and living standards from day one, neatly sidestepping many of the complex licensing rules that come with HMOs.

But all this convenience comes at a price. The entry cost for a single PBSA unit is often much higher than for an HMO, and the net yields, while stable, can sometimes be lower once you factor in the hefty management fees.

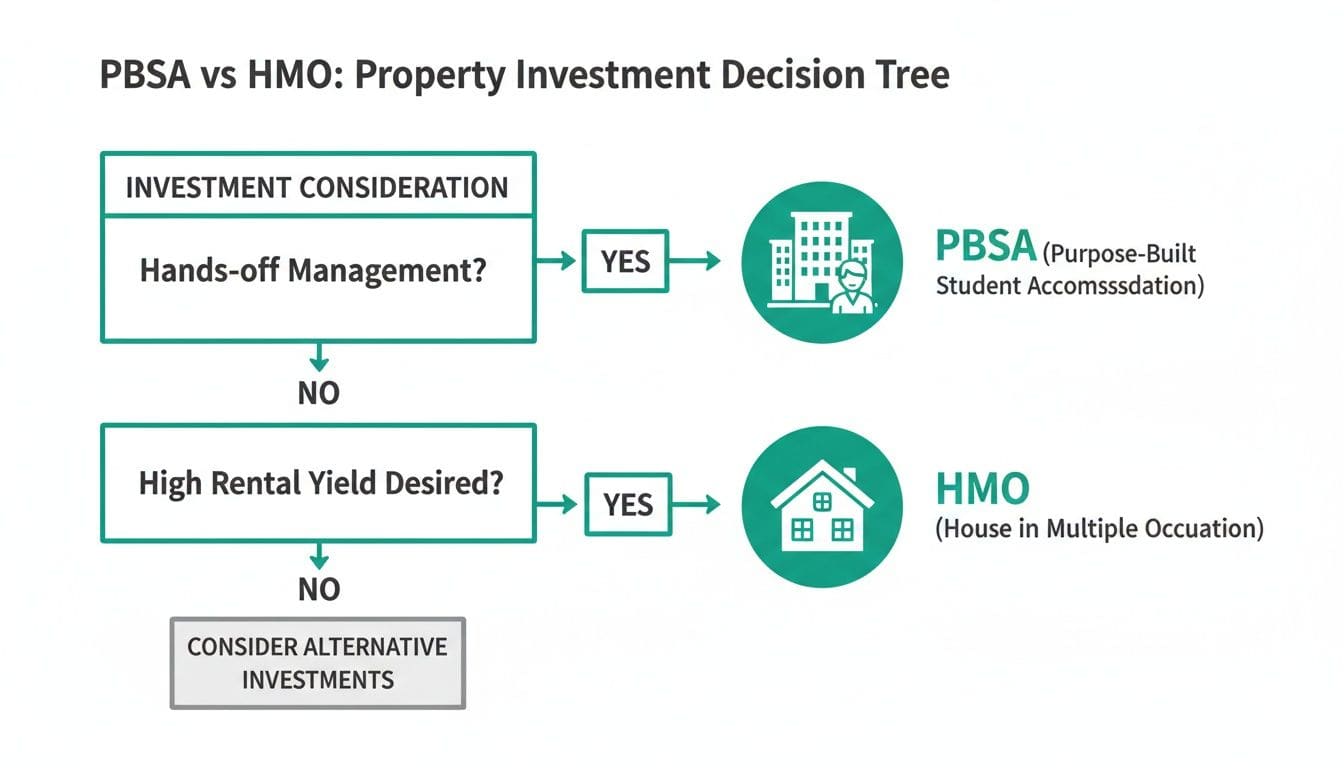

This image sums up the core trade-off perfectly: do you want hands-off management, or are you chasing the highest possible rental yield?

As the diagram shows, investors who prioritise a low-touch, passive income stream are naturally drawn towards PBSA. On the other hand, those focused on maximising gross rental income will find the HMO model far more compelling.

The Reality of Houses in Multiple Occupation (HMOs)

The student HMO is the classic model we all know: a standard residential house converted to be let out room-by-room to three or more unrelated tenants. For decades, this has been the absolute backbone of student housing in the UK.

The main draw of an HMO is its potential for significantly higher gross yields. By renting out individual rooms, your total rental income can easily dwarf what the same property would fetch as a standard family let. This potential for powerful cash flow makes it a hugely attractive option for hands-on investors.

But, as they say, with great yield comes great responsibility. HMOs demand intensive management. You're on the hook for everything from tenant squabbles and routine maintenance to navigating a maze of local and national regulations.

Licensing rules are strict, fire safety standards are rigorous, and council oversight is a given. Getting it wrong can lead to massive fines. What's more, you're dealing with a full tenant turnover every single year, which means a constant cycle of remarketing rooms and managing new tenancies. To get a real handle on the numbers, you need a solid process. You can learn more from our guide on how to evaluate HMOs and other complex deals without getting lost in a spreadsheet nightmare.

Investment Strategy Face-Off: PBSA vs Student HMOs

To really understand which path is right for you, it helps to see the two strategies side-by-side. This table breaks down the key differences to help you decide.

| Factor | Purpose-Built Student Accommodation (PBSA) | House in Multiple Occupation (HMO) |

|---|---|---|

| Management | Almost entirely hands-off; run by a professional management company. | High-touch and intensive; needs direct landlord involvement or a specialist agent. |

| Yield Potential | Stable but generally lower net yields (4.5% - 6%). | Potential for very high gross yields (8% - 15%+), but comes with higher operating costs. |

| Entry Cost | Higher initial capital needed to buy a single unit. | Lower barrier to entry; can be bought with standard finance and then converted. |

| Regulation | Simpler compliance as properties are built to the required standards. | Complex licensing, Article 4 restrictions, and strict, evolving safety standards. |

| Capital Growth | Often slower, as the value is closely tied to the income stream. | Strong potential for capital appreciation, much like a standard residential property. |

Ultimately, the choice between PBSA and HMOs comes down to your personal appetite for risk, your available capital, and how much time you are willing to commit. One offers a steady, passive income, while the other provides the opportunity for higher returns but demands far more of your attention.

Getting the Finance and Tax Right for Your Student Let

Profit in property isn't just about the rent you collect; it's about what you keep after the tax man and the bank have had their share. When it comes to student accommodation, the financial landscape is a whole different beast compared to standard buy-to-lets, especially around mortgages and UK tax law.

Getting this part right is non-negotiable. Seriously. A misstep here can see your profits vanish into thin air, eaten up by unexpected tax bills or eye-watering finance costs.

Securing the Right Mortgage

First up: getting the loan. Don't assume your standard buy-to-let mortgage will do the job, particularly if you're buying a House in Multiple Occupation (HMO). Lenders see student HMOs as a specialist, higher-risk game, and their borrowing rules reflect that.

You should be ready for:

- Tougher Stress Tests: Lenders will run much stricter affordability checks. They need to be absolutely sure the rental income can cover the mortgage payments, even if interest rates were to climb.

- Bigger Deposits: The barrier to entry is higher. For a student HMO, most lenders will want a deposit of at least 25-30%, a noticeable step up from the 20-25% you might see on a vanilla buy-to-let.

- Experience Often Required: Some lenders just won't touch an HMO deal with an inexperienced landlord. They want to see that you've got a track record before they'll fund a more complex asset.

Because of all this, it's almost always worth using a specialist mortgage broker. These guys live and breathe the student let and HMO market. They know which lenders are active and have access to products you'll never find on the high street.

Tackling the Tax Man: Section 24

One of the biggest bombshells for UK landlords in the last decade has been Section 24, sometimes called the 'tenant tax'. This rule completely rewrote how individual landlords are taxed on their rental income.

In the old days, you could subtract your full mortgage interest bill from your rental income before working out how much tax you owed. Simple. Now, if you own property in your personal name, you can't. Instead, you get a tax credit equal to 20% of your mortgage interest costs. This move clobbers higher and additional-rate taxpayers, who used to get relief at 40% or 45%.

The effect is stark: landlords now pay tax on their revenue, not just their profit. For some, this can be enough to push them into a higher tax bracket and turn a once-profitable investment into a money pit after tax.

The Limited Company Solution

So, how are investors fighting back against Section 24? Many now buy their student properties through a limited company, often known as a Special Purpose Vehicle (SPV). When a company owns the property, it isn't subject to those punishing Section 24 rules.

This means the company can still deduct the full cost of its mortgage interest from its rental income before it calculates its Corporation Tax bill. While you'll still pay Corporation Tax on the profits, this structure is often dramatically more tax-efficient for higher-rate taxpayers. It can make a huge difference to the net profit you actually see from your student accommodation as an investment. Just remember, getting money out of the company via dividends will trigger personal tax, so it's a balancing act that needs proper advice.

Understanding Stamp Duty Land Tax (SDLT)

Last but not least, you can't ignore Stamp Duty Land Tax (SDLT). In the UK, any purchase of an additional property gets hit with a 3% SDLT surcharge on top of the standard rates. This is a significant upfront cost you have to budget for from day one.

For larger student properties, the sums can get tricky, especially if the asset could be classed as having multiple dwellings or if the price tag is particularly high. Thinking through your purchase structure is vital to manage this cost effectively. For a deeper dive, it's worth taking the time to understand what Stamp Duty Land Tax is and how it will apply to your specific deal. Getting your SDLT budget right is a critical first step in making sure your investment numbers truly add up.

Your Complete Due Diligence Checklist

Good investments are made long before you ever make an offer. When it comes to student accommodation as an investment, this is doubly true. A rushed decision based on a flashy gross yield figure is the fastest way to a failing portfolio. Proper due diligence is your shield against costly mistakes, ensuring the asset you buy is as solid on paper as it looks in the agent's photos.

This process isn't about ticking boxes blindly; it's about systematically de-risking the deal. You need to investigate the location, understand the local regulations, and, most importantly, run the numbers with brutal honesty. This is where you move beyond optimism and into the realm of cold, hard data.

Location Analysis The Ground Rules

Location is everything in student property, but simply being "close to the university" is just the start of the story. You need to think like a student. Is it a safe, well-lit walk home from the library late at night? Are there decent local amenities like supermarkets, pubs, and cafes within easy reach?

Critically, you must assess transport links. Proximity to a reliable bus route connecting to the campus and the city centre can be a major selling point, especially in larger cities. Drill down to the postcode level—demand can vary dramatically from one street to the next.

Regulatory and Legal Checks

This is where many aspiring investors trip up. The regulatory landscape for student lets, especially HMOs, is a minefield if you're unprepared. Overlooking a key local rule can render your entire business plan useless before you've even started.

Your essential checks must include:

- Article 4 Directions: First things first, check if the property is in an Article 4 area. If it is, you cannot convert a standard family home into a new HMO without full planning permission, which is often difficult to get.

- HMO Licensing: Does the property need a mandatory HMO licence (for five or more tenants)? Does the local council have an additional or selective licensing scheme that applies to smaller HMOs? Check their website and speak to the HMO officer directly.

- Safety Compliance: Verify that the property meets all fire safety regulations, including having the correct fire doors, smoke alarms, and emergency lighting. Confirm that gas and electrical safety certificates are current and in order.

A successful student accommodation as an investment strategy hinges on compliance. The fines for breaching HMO regulations are severe, and local councils are becoming increasingly proactive in enforcement. Ignorance is no excuse.

Robust Financial Analysis

This is the most critical part of your due diligence. Too many investors get fixated on the Gross Yield—the annual rent divided by the purchase price. This figure is dangerously misleading because it ignores all your running costs. To understand the true profitability, you must calculate the Net Yield and Return on Investment (ROI).

This means accounting for every single expense, including:

- Mortgage Payments: Your largest monthly outgoing.

- Management Fees: Typically 10-15% of gross rent if using an agent.

- Council Tax & Utilities: If you're offering an "all-inclusive" bills package.

- Insurance: Specialist landlord and HMO policies are required.

- Maintenance & Voids: A crucial contingency. Budget at least 10% of your rental income for repairs and potential empty periods over the summer.

The resilience of the student sector is clear. The UK Purpose-Built Student Accommodation Index reported a total return of 3.4% for the year to September 2025, with industry revenue projected to hit £7.2 billion in 2025-26. To explore these figures further, you can read the full CBRE research on PBSA performance.

This kind of analysis can feel overwhelming, especially when you're trying to compare multiple deals quickly. This is precisely why tools like the DealSheet AI app are so effective. You can input the property details, and it automatically builds a full financial model, factoring in all UK-specific costs and taxes to give you an accurate picture of your net cash flow and ROI in seconds.

For those looking to deepen their understanding of these essential metrics, you might be interested in our detailed guide on how to calculate the yield on a property. It provides a step-by-step breakdown that moves beyond simple calculations to reveal the true health of your investment.

Managing Risks and Maximising Returns

Every investment has its quirks, and making money from student lets isn't just about collecting rent—it's about smart risk management. Getting your head around the potential hurdles is the first step. Building solid strategies to handle them is what separates the profitable landlords from the ones who get overwhelmed. This isn't about trying to avoid risk altogether, which is impossible, but about seeing it coming and turning threats into manageable problems.

A smart approach means tackling the unique challenges of the student market head-on. If you understand the common pitfalls, you can protect your cash flow, keep your rooms full, and build a resilient asset that performs year after year.

Mitigating Common Investment Risks

The academic calendar creates a rhythm that most standard buy-to-let investors never have to deal with. The most obvious risk is the potential for seasonal void periods during the summer months. If you don't plan for this, it can take a serious bite out of your annual income.

On top of that, rising operational costs, especially utilities in an "all-inclusive" bills model, can quickly eat into your profits. In popular university cities, you're also facing a growing wave of competition from shiny new PBSA blocks and other HMO landlords, which can put a squeeze on rents and occupancy.

Here's how to get ahead of these issues:

- Combat Summer Voids: Don't just accept an empty house in July and August. Proactively target postgraduate or international students, as they often stay in the city year-round for research or work. You could also offer flexible summer lets at a slightly lower rate just to keep the income flowing.

- Get a Grip on Operational Costs: A few smart upgrades can make a huge difference. Swapping to LED lighting, installing smart thermostats, and improving insulation have an upfront cost, but they deliver real savings on utility bills over the long term. It also makes your property far more attractive to today's eco-conscious students.

- Stand Out from the Competition: Don't get dragged into a race to the bottom on price. Focus on quality. A well-maintained property with modern amenities and a landlord who actually fixes things quickly will always command better rents and attract the best tenants.

Strategies to Maximise Your Returns

Dodging risks is only half the job. The other half is actively finding ways to boost your returns. You'd be surprised how small, strategic improvements can have an oversized impact on both your rental income and the long-term value of your property. The aim is to create a better product that students are happy to pay a premium for—and, crucially, are keen to re-book for next year.

The real secret to maximising returns isn't just hiking the rent. It's about adding genuine value that makes the price a no-brainer. Happy tenants become repeat tenants, and repeat tenants mean zero void periods and no remarketing costs. That's pure profit straight to your bottom line.

Consider these simple but effective value-add strategies:

- Light Refurbishments: Never underestimate the power of a cosmetic upgrade. A fresh coat of paint, some modern furniture, and updated taps or shower screens can transform a tired-looking house into a place students are excited to live in.

- Offer All-Inclusive Bills: Students love simplicity and knowing exactly what their outgoings will be. Bundling high-speed internet, utilities, and even a TV licence into the rent is a massive selling point that easily justifies a higher overall price.

- Maintain High Standards: Be the landlord you'd want to rent from. Respond to maintenance issues the same day, get the property professionally cleaned between tenancies, and invest in decent, durable furnishings. This builds a brilliant reputation and encourages re-bookings, which is the ultimate win for any student landlord.

Your Questions on Student Investment Answered

We've talked strategy, risks, and the potential rewards of diving into student property. Now, let's get into the questions that come up time and time again before investors take the plunge.

What Are Typical Rental Yields for Student Accommodation in the UK?

It really depends on the strategy. For a well-run student HMO in a prime university city, you could be looking at gross yields anywhere from 6% to over 10%. That often leaves traditional buy-to-lets in the dust.

Purpose-Built Student Accommodation (PBSA), on the other hand, tends to offer lower yields, typically in the 4.5% to 6% range. The trade-off is that it's a far more hands-off, stable investment. But remember, gross yield is a vanity metric. Always, always calculate your net yield after accounting for every last cost—voids, maintenance, tax, and fees—to see what you'll actually bank.

How Difficult Is It to Get a Mortgage for a Student HMO?

It's definitely more involved than getting a standard buy-to-let mortgage, but it's very achievable. Lenders will want to see a bigger deposit, usually around 25-30%, and they'll often have specific criteria about your experience as a landlord.

The key is not to go it alone. Using a specialist mortgage broker who lives and breathes HMO products is essential. They know which lenders are active in the market and how to package your application for success.

What Are the Best UK Locations for Student Property Investment?

The classic answer is to look at large university cities where student numbers massively outweigh the available housing. Places like Bristol, Manchester, Birmingham, and Nottingham are perennial hotspots for a reason.

However, just picking a city isn't enough. Hyper-local research is absolutely crucial. Performance can vary wildly from one postcode to the next, depending on proximity to campus, transport links, and local amenities. The real wins are found on a street-by-street level, not a city-wide one.