What Is a Good ROI on Rental Property in the UK for 2026?

What Is a Good ROI on Rental Property in the UK for 2026?

So, what is a good ROI on a rental property in the UK? There's no single magic number, but if you ask seasoned investors what they look for in a standard buy-to-let for 2026, you'll often hear a target of 8-12% cash-on-cash return. This figure is the true measure of how hard your invested cash is working for you after all the real-world costs are accounted for. To move beyond guesswork and forecast your return with precision, the DealSheet AI app models every cost, tax, and financing detail right from your phone, giving you actionable insights in seconds.

Defining a Good Rental Property ROI in the UK

Figuring out a 'good' Return on Investment (ROI) for a UK rental property isn't about finding one perfect percentage. It's about matching a target to your own financial goals, how much risk you're comfortable with, and the specific strategy you're running.

Many experienced investors aim for an ROI of 8% or higher, but this can swing wildly depending on the deal. A hands-off, single-family buy-to-let in a stable, high-demand area might deliver a respectable 8% ROI. In contrast, a more management-intensive strategy like a House in Multiple Occupation (HMO) needs to hit returns over 15% to make the extra work and regulatory hoops worth jumping through.

UK Property Investment ROI and Yield Benchmarks for 2026

This table gives you a quick reference for the kind of returns you might expect across different UK property investment strategies in 2026. Think of it as a snapshot to help you gauge if a potential deal is in the right ballpark.

| Investment Strategy | Typical Gross Yield Range | Target ROI Range (Cash-on-Cash) |

|---|---|---|

| Buy-to-Let (BTL) | 5-8% | 8-12% |

| House in Multiple Occupation (HMO) | 10-15% | 15-25% |

| Serviced Accommodation (SA) | 12-20%+ | 20-30%+ |

| Property Flips (BRRRR/Refurb) | N/A (focus is on capital uplift) | 20%+ on invested capital |

Remember, these are just benchmarks. Your actual returns will depend on the specific deal, your financing, and how well you manage the property. The key is to know what a good outcome looks like for your chosen path.

National Averages vs. Regional Reality

To really understand what is a good ROI on rental property, you have to look past the headlines. Government data shows the average property income for unincorporated UK landlords hit £19,400 in the 2023-2024 tax year, a 15% jump from 2019-2020.

But that average hides huge regional differences. For instance, London typically offers lower yields of 2-4%, while properties in the North West can achieve 6% or more. You can read the full property rental income statistics on GOV.UK.

This proves a critical point: a 'good' ROI depends entirely on context. A lower cash return in a high-growth capital city might be a great trade-off if you're banking on strong capital appreciation. In other regions, maximising monthly cash flow is the only game that matters.

The Factors That Define Your Target ROI

Ultimately, your personal criteria will decide what an acceptable return looks like. Ask yourself these questions:

- What's my risk tolerance? Are you comfortable with the higher stakes of a property flip for a potential 20%+ ROI, or do you prefer the steady, predictable returns of a traditional buy-to-let?

- How much time can I commit? An Airbnb or serviced accommodation unit might generate a massive ROI, but it demands serious hands-on management. A standard BTL handled by a letting agent is a completely different beast.

- What are my investment goals? If you want to replace your salary with passive income, you'll need a much higher cash-on-cash return than someone investing purely for long-term capital growth to fund their retirement.

Looking Beyond Yield to Understand Your True Return

Focusing only on rental yield is like judging a car's performance by its top speed. It's an exciting number, but it ignores the real-world factors that actually matter on the road, like fuel efficiency and running costs. For any serious UK property investor, your actual Return on Investment (ROI) is the fuel efficiency—it's what determines whether the journey is profitable or just a costly exercise.

Many investors get hooked on the allure of a high gross yield, but this metric can be dangerously misleading. It's a vanity figure, only looking at rental income against the property's purchase price while completely ignoring the mountain of costs that eat into your real profit. To truly answer the question, what is a good ROI on rental property, you have to look much deeper.

This is where Cash-on-Cash Return comes in. It's the most honest metric you can use, because it tells you exactly how hard your own money is working. It answers one simple, critical question: for every pound I've put into this deal, how many pence am I getting back each year?

The Two Sides of the True ROI Equation

To get to your real return, you need to be brutally honest about two things: the total cash you put in, and the actual profit you get out.

First, let's break down your Total Cash Invested. This isn't just your deposit. It's every single pound you had to spend to get the property ready for a tenant.

- Property Deposit: The big one, usually 25% for a standard buy-to-let mortgage.

- Stamp Duty Land Tax (SDLT): A major tax, especially for second homes, that can add thousands to your initial bill.

- Legal & Conveyancing Fees: The necessary cost for solicitors to handle the property transfer.

- Survey & Valuation Fees: Essential checks to make sure the property is structurally sound and worth what you're paying.

- Initial Refurbishment Costs: From a simple lick of paint to a new kitchen, any money spent upfront is part of your stake in the deal.

On the other side of the equation is your Net Annual Profit. This is what's left after your rental income has been hit by all the real-world running costs of being a landlord.

Key Takeaway: Gross rent is not profit. Your true profit is what remains after every single expense—from mortgage interest to a leaking tap—has been paid. This is the figure that truly determines your investment's health.

Why Yield Is a Flawed Metric

Yield can be a useful starting point for quickly filtering deals, but it fails to account for the biggest expenses that actually determine profitability. A property showing a 7% gross yield might look fantastic on paper, but if it needs a hefty refurbishment and comes with high service charges, its true ROI could plummet to just 3-4%.

On the flip side, a property with a modest 5% yield might have very low running costs and need no initial work, resulting in a much healthier actual return on your cash. This is exactly why a comprehensive analysis is non-negotiable. To get a better handle on this initial metric, you can explore our detailed guide on how to calculate rental yield in the UK.

Ultimately, your goal isn't just to own a property with a high yield; it's to own one that generates a strong, reliable cash return on your invested capital. This shift in mindset—from yield to true ROI—is fundamental for building a successful and sustainable property portfolio.

How to Calculate Your Property ROI Step by Step

Theory is one thing, but confidence comes from running the numbers yourself. Let's ditch the abstract concepts and walk through a real-world UK property deal. This step-by-step calculation will give you a practical blueprint you can use to analyse any buy-to-let opportunity that crosses your desk.

We'll break down every figure for a typical deal outside of London, from the cash you need to find on day one to the final net profit that actually hits your bank account. This is how you find out what is a good ROI on a rental property for a specific investment.

Step 1 Tally Your Total Cash Invested

Your 'Total Cash Invested' is the single most important figure in any ROI calculation. It's not just the deposit; it's every single pound you had to part with to get the keys and make the property ready for a tenant. This is your real skin in the game.

Let's say you're buying a two-bedroom terrace in Manchester for £200,000. Here's a realistic breakdown of the initial cash you'd need:

- 25% Mortgage Deposit: £50,000

- Stamp Duty Land Tax (SDLT): £7,500 (this is at the higher rate for second properties)

- Solicitor/Conveyancing Fees: £1,500

- Mortgage Arrangement Fee: £1,000

- Survey Fees (Level 2): £500

- Initial Refurbishment Budget: £3,000 (for a fresh coat of paint, new carpets, and a deep clean)

Add all that up, and your Total Cash Invested is £63,500. This is the number all your future profits will be measured against.

Step 2 Calculate Your Net Annual Profit

Next up, we need to work out your true annual profit. This means taking your total rental income and then ruthlessly subtracting every running cost you can think of. Forgetting even small expenses is a recipe for a dangerously optimistic forecast.

Let's assume the property rents for £1,000 per month. That gives you a gross annual income of £12,000.

Now, let's deduct the annual running costs:

- Mortgage Interest: £6,000 (based on a £150,000 interest-only mortgage at a 4% rate)

- Landlord Insurance: £300

- Letting Agent Management Fee: £1,440 (a standard 12% of gross rent)

- Maintenance & Repairs Fund: £1,200 (a prudent 10% of gross rent is a good rule of thumb)

- Gas Safety Certificate: £80

- Void Period Allowance: £500 (it's wise to budget for at least two weeks of vacancy per year)

Subtracting these running costs (£9,520) from your gross rent (£12,000) leaves you with a Net Annual Profit of £2,480. For a more detailed look at these costs, our guide on using a buy-to-let calculator in the UK is a great place to start.

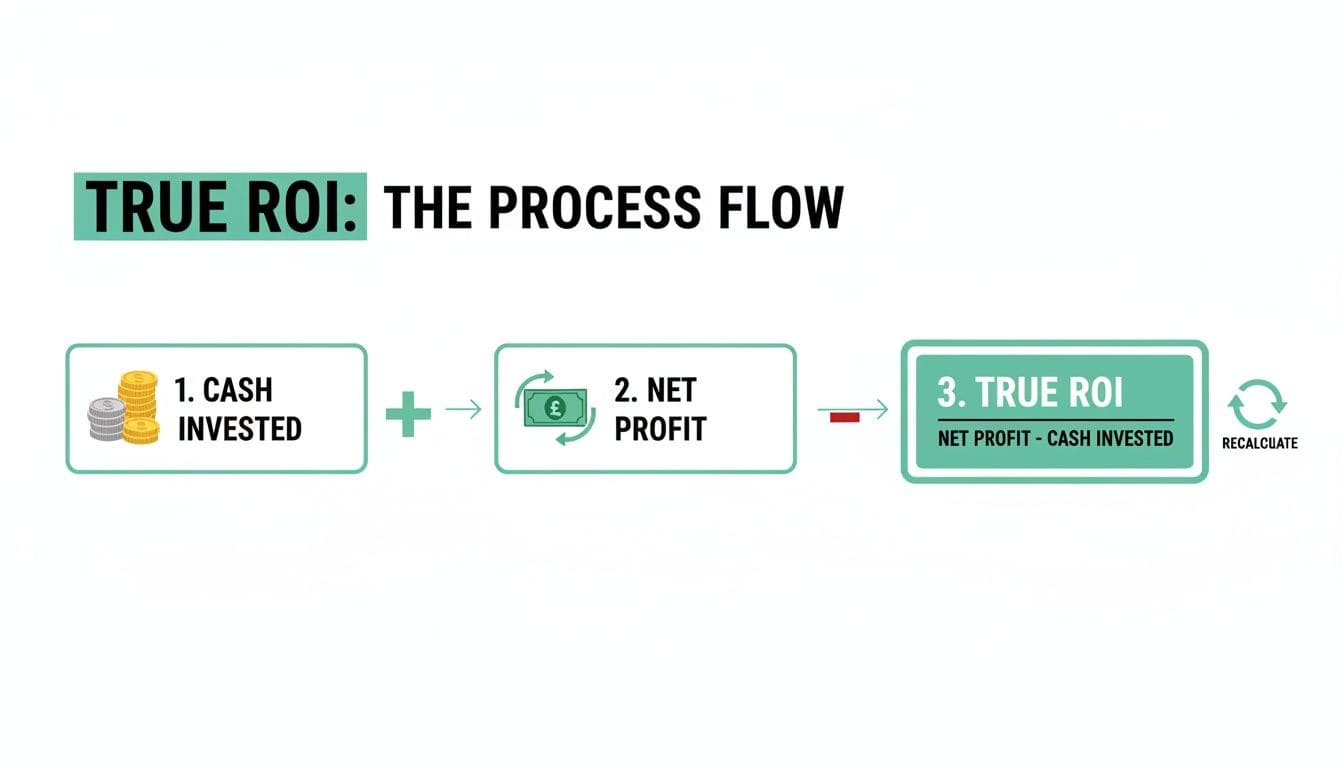

Step 3 Perform the Final ROI Calculation

With your two key figures dialled in, the final step is simple. You just divide your net annual profit by your total cash invested, then multiply by 100 to express it as a percentage.

The ROI Formula: (Net Annual Profit / Total Cash Invested) x 100 = ROI %

Plugging in the numbers from our Manchester example: (£2,480 / £63,500) x 100 = 3.91%

This visual breaks the process down, showing how your initial cash input and final net profit come together to give you the true return.

As you can see, the calculation strips away all the noise, focusing purely on how hard your cash is working for you.

So, is 3.91% any good? On its own, it looks quite low, falling short of that 8-12% benchmark we talked about. But remember, this figure doesn't include any potential capital appreciation. If the property's value goes up over time, your total return would be much higher when you eventually sell. This calculation gives you the pure, unvarnished cash-on-cash return—the most critical measure of how an asset is performing year on year.

How Your Investment Strategy Shapes Your ROI

A standard buy-to-let is just one way to play the property game in the UK, and the ROI you can expect changes dramatically depending on the strategy you pick. While a traditional rental offers a steady, almost passive return, more hands-on strategies can deliver seriously impressive profits—if you're ready for the extra work and risk.

Trying to answer "what is a good ROI on a rental property" is like asking "how fast is a vehicle?". A family car is worlds apart from a Formula 1 car. It's the same in property. The return from a hands-off single let has almost nothing in common with a high-turnover holiday home. Getting your head around these differences is the first step to matching your financial goals with the right investment model.

Houses in Multiple Occupation (HMOs) for Higher Cash Flow

A House in Multiple Occupation (HMO) is simply a property rented out to at least three people who aren't from the same family but share a kitchen or bathroom. For investors, the logic is compelling: more tenants equals more rent, which often leads to supercharged cash flow.

While a standard buy-to-let might bring in a respectable 8-12% ROI, a well-managed HMO can often hit 15% or even higher. But this extra profit doesn't come for free.

- Intense Management: Juggling multiple tenancies under one roof is far more demanding than dealing with a single family.

- Strict Regulations: HMOs are wrapped in red tape. You'll face stringent licensing rules, fire safety standards, and minimum room sizes that can be costly and a headache to navigate.

- Higher Turnover: Tenants come and go more often in HMOs. If you don't have a slick system for filling rooms, you'll be hit with more void periods and re-letting costs.

Serviced Accommodation for Maximum Revenue Potential

Serviced accommodation (SA), which most people know through platforms like Airbnb, is about letting your property out on a short-term basis, just like a hotel. This strategy can produce the highest returns of all, with top-tier properties potentially hitting an ROI of 20-30%. The secret is charging a premium nightly rate to capture demand from tourists, business travellers, or people between house moves.

For example, in the 12 months to December 2024, the London serviced accommodation market showed its muscle. The average monthly revenue per property was £3,174, with a high occupancy rate of 74% and an average daily rate of £152. Those numbers generate gross returns that leave traditional buy-to-lets in the dust. Discover more insights about London's Airbnb market on Airbtics.com.

But make no mistake—the SA model is a hospitality business, not a passive investment. It demands constant guest communication, cleaning, and maintenance, and your income can swing wildly with the seasons.

The BRRRR Method for Infinite Returns

The Buy, Refurbish, Refinance, Rent (BRRRR) strategy is a more advanced technique all about recycling your capital. The goal is to buy a rundown property, force its value up through a smart refurbishment, and then refinance based on its new, higher valuation to pull all (or most) of your initial cash back out.

If you nail it, you're left with a cash-flowing rental property with none of your own money left in the deal. This creates a theoretically infinite ROI, because you have zero cash invested. The "profit" is the cash you've pulled out, which you can then roll into the next project to scale your portfolio at speed.

Of course, BRRRR is the definition of high-risk, high-reward. It hinges on your ability to accurately forecast refurb costs and the final property value, and it's highly sensitive to what's happening in the mortgage market.

Comparing UK Property Strategy ROI

Each of these strategies offers a different balance of risk, reward, and hands-on effort. Choosing the right one depends entirely on your resources, experience, and what you're trying to achieve as an investor.

| Strategy | Typical ROI Range | Key Profit Driver | Management Level | Primary Risk Factor |

|---|---|---|---|---|

| Buy-to-Let | 4-8% | Steady rental income and long-term capital growth. | Low | Market downturns affecting property values. |

| HMO | 8-15%+ | Multiple rental streams from a single property. | High | Stricter regulations and higher tenant turnover. |

| Serviced Accommodation | 15-30%+ | High nightly rates charged to short-term guests. | Very High | Income seasonality and operational complexity. |

| BRRRR | Potentially infinite | Capital recycling through refinance after adding value. | High | Refurb cost overruns and valuation uncertainty. |

Understanding this landscape is critical. These different approaches carry unique risks and rewards, which is why it's essential to understand the full range of UK property investment strategies before you put your capital on the line.

Uncovering the Hidden Costs That Erode Your ROI

A promising ROI on paper can quickly dissolve when it meets reality. The gap between a profitable investment and a financial drain often comes down to the costs you didn't see coming. To truly understand what is a good ROI on rental property, you have to get good at spotting these hidden expenses before they start eating into your returns.

These aren't just minor miscalculations; they are significant financial hurdles that every UK investor must plan for. A spreadsheet might show a healthy return, but taxes, financing choices, and operational surprises can easily turn a great deal into a mediocre one.

The Impact of UK Tax and Regulations

Tax is arguably the biggest hidden cost for UK landlords. If you don't account for it properly from day one, it can dramatically shrink your net profit.

-

Section 24 (The Tenant Tax): This rule has been a game-changer, especially for higher-rate taxpayers. It stops you from deducting your mortgage interest costs from your rental income before working out your tax bill. Instead, you get a tax credit equal to 20% of your interest payments. For anyone paying tax at the 40% or 45% rate, this means paying significantly more tax than before, hitting your bottom line directly.

-

Stamp Duty Land Tax (SDLT): As an investor buying an additional property, you'll be paying a higher rate of SDLT. This is a substantial upfront cost that has to be factored into your total cash invested, as it directly reduces your final ROI. Getting this figure wrong can throw off your entire analysis from the very beginning. For a detailed breakdown, you can learn more about how Stamp Duty Land Tax is calculated in our guide.

-

Capital Gains Tax (CGT): While this only kicks in when you sell, CGT can take a huge bite out of your total profit. You pay tax on the gain you've made—the difference between your sale price and your purchase price plus any allowable costs. With the annual exempt amount for CGT being slashed in recent years, more of your profit is now exposed to tax, making it a crucial long-term consideration.

How Financing Choices Skew Your Returns

Your mortgage isn't just a loan; it's a major operational expense that dictates your monthly cash flow. The specific product you choose can have a surprising effect on your overall profitability.

Many investors make the mistake of focusing only on the interest rate. But high arrangement fees, sometimes running into thousands of pounds, can be added to the loan or paid upfront. If you pay them upfront, they increase your initial cash investment and lower your ROI. If you add them to the loan, they increase your monthly interest payments.

Investor Insight: Always model a few different financing scenarios. A slightly higher interest rate with no product fee might actually produce a better ROI than a lower rate with a hefty upfront charge, especially if you plan to refinance in a few years.

The Operational Cash Killers

Beyond taxes and finance, the day-to-day reality of owning a property brings its own unpredictable costs. These are the operational cash-killers that new investors often underestimate.

-

Void Periods: No property stays occupied 100% of the time. It's just not realistic. Budgeting for at least two to four weeks of vacancy each year is a sensible precaution.

-

Surprise Repairs: A boiler breakdown in the middle of winter can set you back £2,000-£3,000 instantly. Without a dedicated maintenance fund, one major repair can wipe out months of profit.

-

Compliance Costs: Being a landlord in 2026 means navigating a maze of regulations. Annual Gas Safety certificates, five-yearly Electrical Installation Condition Reports (EICRs), and potential licensing fees are all mandatory costs of doing business.

These hidden expenses are precisely why a healthy contingency fund isn't just a nice-to-have. It's an essential buffer that protects your investment from the unexpected and makes sure your calculated ROI stays achievable.

Actionable Ways to Boost Your Rental Property ROI

A good ROI isn't always found; it's made. The best investors don't just accept the numbers a deal presents at face value. They actively hunt for ways to force the numbers up, treating every property as an asset that can be improved.

Improving your return is a game of strategic nudges and shoves. It's about increasing income, squeezing down costs, and structuring your finances to be as efficient as possible. Every one of these is a lever you can pull to make your invested capital work that much harder for you.

Add Real Value Through Smart Refurbishments

One of the most direct ways to boost your rental income is to improve the property itself. But this isn't about splashing cash on expensive, indulgent overhauls. It's about making targeted upgrades that tenants in 2026 will actually value and pay a premium for.

Forget a simple lick of paint. In an era of remote and flexible working, turning a neglected box room or even a large cupboard into a dedicated home office can be a massive selling point. Likewise, a fresh, modern kitchen or bathroom can dramatically lift the achievable rent and attract a higher calibre of tenant who is more likely to stay long-term.

The entire game is to focus on changes that deliver a return.

- Create a Home Office: Adding a small, functional workspace can justify a higher rent and make your property the obvious choice for professional tenants.

- Upgrade Key Rooms: Your budget has the most impact in kitchens and bathrooms. These are the spaces that make or break a tenant's decision.

- Improve Kerb Appeal: First impressions count. Simple landscaping, a new front door, or sparkling clean windows can cut down your void periods significantly.

Of course, when you're planning these upgrades, you have to get your numbers right. Having a solid grasp of typical building costs per square metre in the UK will help you budget properly and ensure your refurb adds more in rental income or capital value than it costs you to complete.

Optimise Your Finances and Operations

Beyond bricks and mortar, you can wring out a surprising amount of extra ROI just by refining your financial and operational setup. This is all about minimising the drag on your profits from high interest rates and inefficient day-to-day management.

Reviewing your mortgage periodically is non-negotiable. If you can refinance to a lower interest rate, you directly slash your single biggest monthly outgoing. That's an instant boost to your net cash flow and your ROI. Another powerful move is to strategically release equity after a property's value has increased, freeing up capital to fund your next deposit without finding new cash.

Investor Tip: Don't just get fixated on the headline interest rate when you refinance. You have to look at the total cost, including arrangement fees. Sometimes those fees can wipe out the savings from a lower rate over a typical two or five-year fixed term.

Operationally, small tweaks can lead to big wins. Implementing efficient property management systems can save you hours of admin and prevent costly mistakes. And a simple change like adopting a pet-friendly policy can open up a wider pool of responsible, long-term tenants who are often happy to pay a bit more, reducing expensive turnover and voids.

Your ROI Questions Answered

When you're getting to grips with property investment, a few questions always pop up. Let's tackle some of the most common ones investors ask when figuring out what is a good ROI on a rental property in the UK. Think of this as the final check to make sure you're analysing deals with complete confidence.

What's the Real Difference Between ROI and Yield?

You'll hear investors throw these terms around, sometimes using them for the same thing. They're not. Knowing the difference is crucial.

Gross Yield is a quick, back-of-the-envelope calculation: (Annual Rent / Property Price) x 100. It's a useful first glance to filter out obvious no-go deals, but it ignores every single cost.

ROI, specifically the Cash-on-Cash Return, is the number that truly matters. It tells you how hard your invested cash is working by comparing your actual annual profit (rent minus all your costs) against the total cash you put in (deposit, stamp duty, fees, refurb costs).

Put it this way: yield is vanity, ROI is sanity.

So, Is a 5% ROI a Good Deal in the UK?

This is a classic "it depends" scenario, and the context is everything.

If you're looking at a straightforward, single-let property in a solid area with great tenants and strong potential for the property's value to grow over time, a 5% ROI (cash-on-cash return) might be perfectly fine. It's a steady, low-effort part of a bigger wealth-building plan.

But if you're running a high-intensity strategy like an HMO or a Serviced Accommodation unit, a 5% ROI would be a disaster. Those strategies come with far more management, risk, and regulatory hoops to jump through. To make that extra work worthwhile, you should be targeting returns of 15% or even higher.

Where Does Capital Appreciation Fit into My ROI?

This is a really important distinction. Your yearly cash-on-cash ROI calculation doesn't include capital appreciation. That metric is purely about measuring how efficiently your cash investment generates rental profit, year in, year out.

Capital appreciation is the other half of your return, but you only actually get your hands on it when you sell or refinance the property. While it's a huge part of building wealth through property, you need to keep it separate from your operational ROI. This stops you from confusing cash flow performance with long-term growth.

The best investments, of course, deliver both. Healthy cash flow keeps the business running, and capital growth builds your net worth in the background.

How Can I Calculate ROI Quickly Without Making Mistakes?

The single biggest headache in calculating ROI is getting all the numbers right. It's painfully easy to forget a cost—a bit of maintenance, a void period, or the true stamp duty figure—and suddenly your profitable-looking deal is actually a liability.

Investor Takeaway: Manual spreadsheets are a breeding ground for errors. They're slow to build for every deal you look at, and one broken formula can give you a dangerously optimistic forecast. A purpose-built tool makes sure every cost is counted and every calculation is consistent.

This is where technology gives you a serious edge. Instead of wrestling with spreadsheet formulas, you can model a deal in seconds, confident that no hidden costs have been missed. It gives you a reliable foundation to make smart, fast investment decisions.

Ready to stop guessing and start analysing property deals with speed and precision? The DealSheet AI app is designed for UK investors who need to analyse opportunities quickly and accurately. Paste a property link, and our AI builds a complete financial model in seconds, accounting for every UK-specific cost and tax.

Download DealSheet AI from the App Store and start your free trial today.