Master Your UK Property Investments with a Buy to Let Calculator UK for 2026

Master Your UK Property Investments with a Buy to Let Calculator UK for 2026

Figuring out if a UK property deal actually works requires more than a gut feeling—it demands a ruthless focus on the numbers, and the best way to achieve this is with a powerful buy to let calculator UK. This essential tool cuts through the noise and guesswork to show you a property's real financial potential, giving you the critical metrics—rental yield, cash flow, and return on investment (ROI)—that separate a profitable asset from a costly mistake. For investors needing to analyse deals quickly and accurately, tools like the DealSheet AI app automate the entire process, turning a simple property listing into a full financial model in seconds.

Your Essential Tool For Smart UK Property Investing

At its core, UK property investing is a numbers game. Your intuition about a great street or a property with "potential" is a good starting point, but it must be backed up by cold, hard data. Think of a buy-to-let calculator as your financial co-pilot; it translates property details, costs, and mortgage figures into a clear verdict on whether a deal stacks up.

This guide will walk you through exactly how these calculators work, what numbers you need to feed them, and how to read the results to make decisions that build wealth. Once you get the hang of it, you'll have the confidence to analyse any potential UK property investment that comes your way.

Why Every UK Investor Needs a Calculator

The UK property market can shift quickly. A solid calculator keeps your decisions grounded in financial reality, preventing you from getting caught up in hype or speculation.

- Objective Analysis: It strips the emotion out of the decision. The numbers either work, or they don't.

- Speed and Efficiency: You can run dozens of scenarios in minutes. What if interest rates rise? What if the rent is lower than expected? You get instant answers.

- Risk Mitigation: By forcing you to account for everything from stamp duty to potential void periods, it helps you avoid nasty surprises that can sink a deal later on.

Right now, this kind of analysis is more critical than ever. The UK rental market is seeing unprecedented conditions. Gross rental yields on new buy-to-lets in England and Wales soared to a record high towards the end of 2024. As we move into 2026, this trend of a serious, ongoing imbalance between rental supply and tenant demand is expected to continue, creating a unique moment for investors who know their numbers. You can discover more insights about the current state of the buy-to-let market.

A proper financial breakdown is the difference between a successful long-term investment and a costly mistake. It's the foundation upon which a profitable property portfolio is built, especially for those just starting out.

This article breaks down the mechanics, giving you the power to move forward with confidence. If you're new to all this, understanding these fundamentals is the perfect first step. You might also find our property investment for beginners guide useful for building more foundational knowledge.

Gathering the Right Numbers for Accurate Calculations

The output from any buy to let calculator uk is only as reliable as the numbers you feed it. To get from a vague guess to a proper financial forecast, you have to account for every single cost that comes with buying and running a UK investment property.

It's a bit like baking a cake; if you miss a key ingredient or get the measurements wrong, the result will be a mess.

A solid calculation needs you to look far beyond the headline figures like the purchase price and expected monthly rent. Too many investors get fixated on these numbers alone, which is a fast track to nasty surprises that eat away at their returns. To build a robust financial model, you need a complete checklist covering both the one-off costs to buy the place and all the ongoing expenses to run it.

Essential Upfront Investment Costs

Before you even get the keys, you'll need a significant amount of cash ready to go. These one-off costs are the foundation of your Return on Investment (ROI) calculation, so getting them right is absolutely critical.

- Purchase Price: The price you've agreed to pay for the property.

- Deposit: The chunk of the purchase price you're paying yourself. For a buy-to-let mortgage in the UK, this is typically 25% or more.

- Stamp Duty Land Tax (SDLT): A big one. For second homes in England and Northern Ireland, you'll pay a hefty surcharge on top of the standard rates. This cost is easily underestimated. For a deeper dive, check out our guide on using a Stamp Duty Land Tax calculator.

- Legal Fees: The cost for your solicitor or conveyancer to handle all the legal paperwork. Expect to pay somewhere between £1,000 to £2,500.

- Surveyor Fees: Essential for flagging potential structural problems. A decent survey can cost anywhere from £400 to over £1,500, depending on how detailed it is.

- Mortgage Fees: This covers arrangement fees from your lender. You can often add these to the loan, but they still add to your overall cost base.

- Initial Refurbishment: You must budget for any immediate work needed to get the property ready for tenants—think a lick of paint, new carpets, or essential repairs.

Forgetting even one of these upfront costs can skew your entire investment analysis. A good calculator forces you to consider each one, ensuring your initial capital outlay figure is accurate from the start.

Critical Ongoing Operational Expenses

Once the property is legally yours, the costs don't stop. These are the recurring monthly or annual expenses that determine your true net cash flow—the actual profit that lands in your bank account each month. Any quality buy to let calculator uk will prompt you for all of these.

- Mortgage Payments: Your monthly repayment to the lender. This is usually your single biggest outgoing.

- Letting Agent Fees: If you're not self-managing, expect to pay an agent between 8% and 15% of the monthly rent for finding tenants or full management.

- Landlord Insurance: This isn't standard home insurance. You need specialist cover for the building, liability, and sometimes loss of rent. It's a non-negotiable cost.

- Maintenance Budget: A sensible rule of thumb is to set aside 1% of the property's value each year for repairs and general upkeep. Things will break.

- Service Charges & Ground Rent: For leasehold properties like flats, these are annual fees to cover the maintenance of communal areas and the building itself.

- Void Periods: No property is occupied 100% of the time. Factoring in a void period of at least a few weeks per year provides a much-needed realistic buffer for your cash flow.

- Utilities & Council Tax: These are costs you'll likely have to cover yourself during those void periods between tenancies.

By meticulously gathering these figures, you transform a basic buy to let calculator uk from a simple toy into a powerful forecasting engine that gives you numbers you can actually trust.

Putting the Calculator to Work with UK Property Examples

Theory is one thing, but seeing a buy-to-let calculator chew on real numbers is where the clarity really comes from. To bring all this to life, let's walk through the four essential calculations every investor needs, using a realistic example of a UK investment property.

Imagine you've found a two-bedroom terrace house in the Midlands that looks promising. Here are the headline figures:

- Purchase Price: £200,000

- Deposit (25%): £50,000

- Total Upfront Costs (SDLT, fees etc.): £10,000

- Total Capital Invested: £60,000

- Expected Monthly Rent: £950 (£11,400 per year)

With these numbers scribbled on the back of an envelope, we can now dig into the metrics that will tell us if this deal is actually a winner.

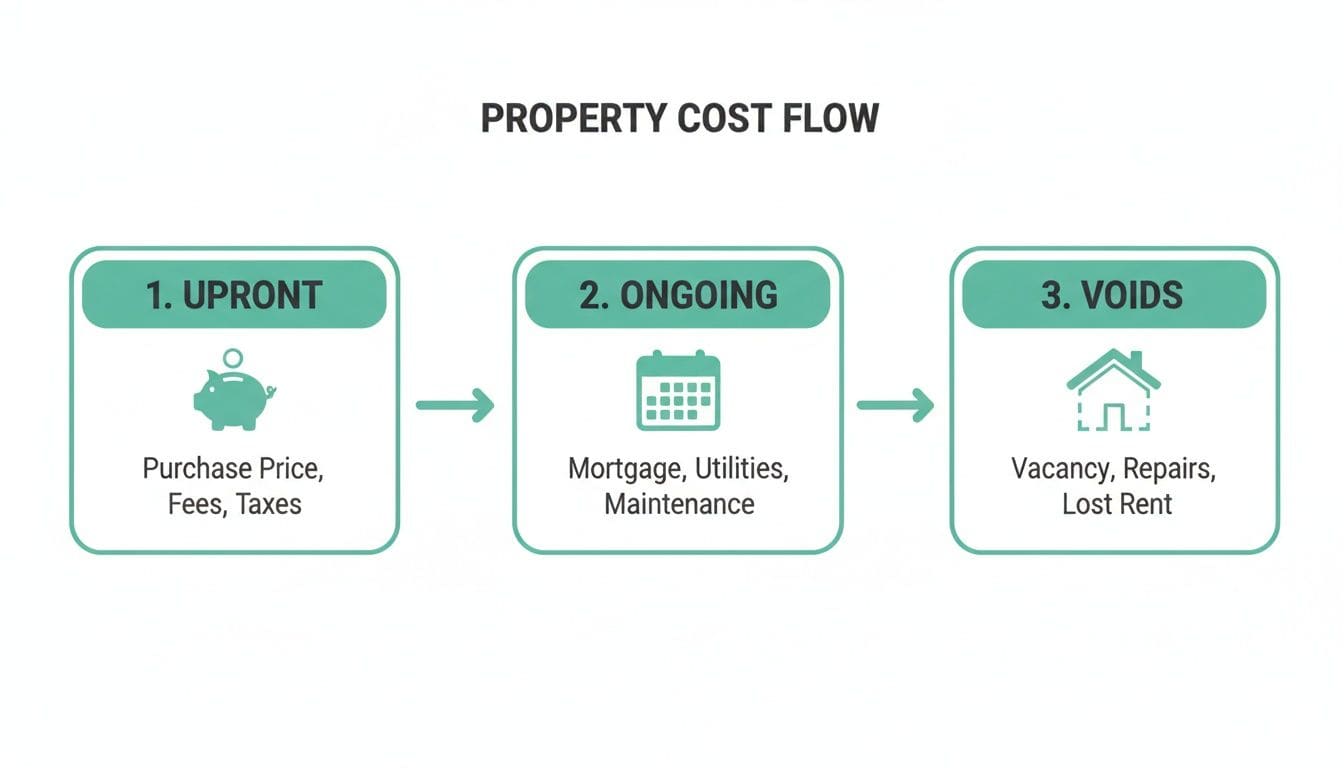

First, it's crucial to understand where your money is going. This diagram breaks down the different costs you'll face on any property journey.

As you can see, a profitable investment isn't just about the purchase price. You have to budget properly for one-off upfront costs, predictable ongoing expenses, and those inevitable gaps in income from void periods.

Example 1: Calculating Gross and Net Rental Yield

Rental yield is the first health check for any buy-to-let. It's a quick-and-dirty measure of the annual rent as a percentage of the property's value. It comes in two flavours: gross and net.

Gross Rental Yield is the simple one. It just looks at the rental income against the purchase price, ignoring all your running costs.

- Formula: (Annual Rental Income / Purchase Price) x 100

- Calculation: (£11,400 / £200,000) x 100 = 5.7%

But Net Rental Yield gives you a much more honest picture by factoring in all the operational costs. Let's say your annual running costs—things like mortgage interest, insurance, agent fees, and a maintenance fund—add up to £7,200.

- Formula: ((Annual Rental Income - Annual Running Costs) / Purchase Price) x 100

- Calculation: ((£11,400 - £7,200) / £200,000) x 100 = 2.1%

See how quickly the numbers change? A 5.7% gross yield looks perfectly respectable, but the 2.1% net yield is a far more accurate reflection of what the property is actually earning. For a much deeper dive, check out our complete guide to analysing UK buy-to-let deals.

Example 2: Determining Monthly and Annual Cash Flow

Cash flow is the absolute lifeblood of your property portfolio. It's the actual profit left in your bank account after every single bill has been paid. Positive cash flow means the property is funding itself and putting extra money in your pocket.

Let's break down the monthly figures:

- Monthly Rent: £950

- Monthly Mortgage Payment: £600

- Other Monthly Costs (insurance, agent fees etc.): £250

- Total Monthly Outgoings: £850

Now we can work out the cash flow:

- Monthly Cash Flow Formula: Monthly Rent - Total Monthly Outgoings

- Calculation: £950 - £850 = £100 per month

- Annual Cash Flow: £100 x 12 = £1,200 per year

That £100 a month is your buffer and your profit. It's the money that proves the investment is working.

Example 3: Measuring Your Return on Investment (ROI)

While yield measures income against the property's value, Return on Investment (ROI) is arguably the most important metric of all. It tells you how hard your actual cash is working for you.

Your total invested capital was your £50,000 deposit plus £10,000 in upfront costs, for a total of £60,000 out of your pocket.

- ROI Formula: (Annual Net Profit / Total Capital Invested) x 100

- Calculation: (£1,200 / £60,000) x 100 = 2.0%

A 2.0% ROI might feel low, but remember, this is purely the return on your cash from rental income. It doesn't include any potential capital appreciation if the property's value goes up over time.

Example 4: Modelling the Impact of UK Taxes

Finally, no UK property analysis is complete without tackling tax. Under the Section 24 rules, higher-rate taxpayers can no longer deduct their mortgage interest from their rental income. Instead, they just get a 20% tax credit. This can be brutal.

Let's assume you're a 40% taxpayer and your annual mortgage interest is £4,800. Here's how the taxman sees it:

- Taxable Income: Your full annual rent of £11,400 is considered income.

- Tax Due at 40%: £11,400 x 40% = £4,560

- Tax Credit (20% of interest): £4,800 x 20% = £960

- Final Tax Bill: £4,560 - £960 = £3,600

Your annual profit before tax was £1,200. But after paying £3,600 in tax, this investment is now running at a significant loss. This single example shows exactly why any good buy-to-let calculator must account for Section 24, or you risk walking straight into a financial disaster.

The table below summarises the key steps we've walked through, showing how each metric is built upon the last.

Sample Calculation Breakdown for a UK Buy-to-Let Property

This table provides a clear, step-by-step breakdown of the inputs and calculations for the key performance metrics of our example UK investment property.

| Calculation Step | Formula Used | Example Value |

|---|---|---|

| Gross Annual Rent | Monthly Rent x 12 | £950 x 12 = £11,400 |

| Gross Rental Yield | (Annual Rent / Purchase Price) x 100 | (£11,400 / £200,000) x 100 = 5.7% |

| Net Annual Income | Annual Rent - Annual Running Costs | £11,400 - £7,200 = £4,200 |

| Net Rental Yield | (Net Annual Income / Purchase Price) x 100 | (£4,200 / £200,000) x 100 = 2.1% |

| Annual Cash Flow | Net Annual Income - Mortgage Capital Payments | £4,200 - £3,000 (example) = £1,200 |

| Return on Investment (ROI) | (Annual Cash Flow / Total Capital Invested) x 100 | (£1,200 / £60,000) x 100 = 2.0% |

| Final Tax Bill (40% Taxpayer) | (Taxable Income x 40%) - (Interest x 20%) | (£11,400 x 40%) - (£4,800 x 20%) = £3,600 |

Seeing the numbers laid out like this really highlights how an initially promising deal can look very different once all costs and taxes are factored in. This is the core job of a reliable calculator: to move you from headline figures to the financial reality.

Common Mistakes That Lead to Bad Investments

A buy to let calculator uk might seem simple enough, but a few classic blunders can turn a promising deal into a financial nightmare. Get the analysis wrong at the start, and you're building your entire investment on dangerously flawed projections. In a market with tight margins, there's just no room for that kind of error.

The smartest investors I know treat their calculator not as a magic box that spits out a "yes" or "no," but as a tool that demands realistic, well-researched inputs. Let's break down the most common traps.

Underestimating Voids and Maintenance

It's so easy to get carried away by the headline rent. But one of the fastest ways to end up with negative cash flow is to ignore the small, recurring costs that relentlessly eat away at your profit margin.

A classic rookie mistake is assuming your property will be tenanted 365 days a year. It never is. Any decent buy to let calculator uk will force you to account for void periods—the empty weeks between tenancies. Being conservative here is your best defence; I always budget for at least one month of vacancy per year.

Likewise, maintenance isn't an "if," it's a "when." Boilers break. Fences blow over. Tenants will always find something that needs fixing. A good rule of thumb is to set aside 1% of the property's value every single year for repairs. On a £200,000 property, that's a £2,000 maintenance fund. Pretending these costs don't exist gives you a dangerously optimistic view of your cash flow.

- The Void Period Trap: Forgetting to budget for at least 4-6 weeks of vacancy each year, which can wipe out a huge chunk of your annual profit.

- The Maintenance Miscalculation: Not ring-fencing a dedicated fund for repairs, leaving you to cover surprise costs from your personal savings.

Ignoring the True Impact of UK Tax Rules

This is a big one, especially for higher and additional-rate taxpayers. A critical error is failing to correctly model the impact of Section 24. These tax rules stop you from deducting your mortgage interest as a business expense, swapping it for a far less generous 20% tax credit.

This isn't some minor detail you can ignore; for anyone paying 40% or 45% tax, it can completely wipe out the profitability of a leveraged investment. A generic, non-UK calculator will miss this nuance entirely, presenting a profit figure that is dangerously misleading.

This is more relevant than ever right now. The UK buy-to-let market is shifting under the weight of new regulations and tax burdens. Data suggested a significant number of landlords were exiting the market in the previous couple of years, with more potentially following by 2026 as profitability gets squeezed. You can read more about the trends shaping the 2025 rental property market on Landlord Zone.

Forgetting One-Off Acquisition Costs

Your Return on Investment (ROI) is based on the total cash you put into a deal. Too many investors make the mistake of only counting their deposit. But the true figure for your "cash invested" has to include every single one-off acquisition cost.

These always include:

- Stamp Duty Land Tax (SDLT): The 3% surcharge on additional properties is a significant upfront hit.

- Legal Fees: Conveyancing costs can easily top £1,500.

- Surveyor and Mortgage Fees: Essential due diligence and lending costs that all add up.

- Initial Refurbishment: The budget needed just to get the property ready for its first tenant.

If you forget to add these costs to your initial investment in the calculator, you'll artificially inflate your ROI percentage. It'll make the deal look far better than it actually is. By avoiding these common traps, you ensure your analysis is grounded in reality, protecting your capital and setting your investment up for genuine success.

When to Move Beyond a Basic Calculator

A standard buy to let calculator uk is brilliant for a quick first look at a property. It gives you the headline numbers you need to decide if an investment is even worth a second thought. But for any serious investor, that initial screen is just the starting whistle, not the final score.

Sooner or later, you'll hit the ceiling of what these simple tools can do.

What happens when you need to compare five potential deals side-by-side, each with its own unique costs and mortgage terms? Or when you want to properly model more creative strategies like BRRRR (Buy, Refurbish, Rent, Refinance, Repeat) or an HMO (House in Multiple Occupation)? This is the point where you graduate from a simple calculator to a proper property analysis tool.

The Limits of Simple Calculators

Let's be clear: basic online calculators are designed for one job—running the numbers on a straightforward, single-let property. They often buckle under the weight of modern UK property investing.

- No Strategy Templates: They can't model the unique cash flow of an HMO with multiple tenants or a BRRRR deal that hinges on a critical refinancing step. They treat everything like a vanilla buy-to-let.

- Limited Tax Modelling: Most fail to automatically apply nuanced UK tax rules, particularly the punishing impact of Section 24 on higher-rate taxpayers. This isn't a small oversight; it can wipe out your entire profit.

- Inability to Compare: You can only analyse one deal at a time. This forces you back into messy, error-prone spreadsheets just to see how opportunities stack up against each other.

- No Long-Term View: They rarely account for future capital expenditure or model how your returns change over a 5, 10, or 20-year holding period. They live purely in the here and now.

These limitations aren't just inconvenient; they're dangerous. A flawed analysis could lead you to chase a deal that looks profitable on the surface but is a financial dead end in reality. For a deeper dive into the financial mechanics, our guide on structuring complex deals is essential reading.

Stepping Up to Advanced Property Analysis

When your investment strategy evolves, your toolkit has to evolve with it. This is where advanced analysis platforms come in, built specifically to solve the problems that basic calculators can't touch. Tools like DealSheet AI, for example, are designed from the ground up for the UK market.

Instead of tedious manual data entry, these tools can often extract key information straight from a property listing URL. In a fast-moving market, that speed is a massive advantage.

The real power, though, lies in the pre-built financial models. Whether you're analysing a standard buy-to-let or a multi-unit block, the tool applies the correct UK-specific rules for SDLT, Section 24, and financing assumptions, making your analysis both consistent and reliable.

Advanced tools move you away from fragile, homemade spreadsheets and towards a professional system for underwriting deals. They give you the robust financial modelling needed to make confident, data-driven investment decisions. This isn't just about finding good deals; it's about systematically avoiding the bad ones. By embracing a more powerful approach, you gain the clarity required to build and scale a successful UK property portfolio.

From Numbers to a Confident "Yes"

Right, you've wrestled with the key metrics, seen how the numbers play out in the real world, and you're wise to the common traps that can trip up even experienced investors. The final piece of the puzzle is turning all that hard work into a clear, confident decision.

The whole point of using a buy to let calculator uk isn't just to spit out a bunch of figures. It's about building a solid, evidence-backed case for your investment.

This kind of rigorous analysis does more than just help you sleep at night. It's a powerful tool in its own right. When you walk into a lender's office with a detailed financial model, you're not just an applicant; you're a professional. It immediately shows you've done your homework and dramatically improves your chances of getting the finance you need. Likewise, knowing your numbers inside-out strengthens your hand when it's time to negotiate, letting you justify your offer with cold, hard data.

Your Final Pre-Commitment Checklist

Before you pick up the phone to instruct your solicitor, run through this one last time. Think of it as your final pre-flight check, making sure every dial is green before your investment takes off. A methodical review at this stage can save you a world of pain and expense down the line.

- Have I stress-tested my numbers? What happens to my cash flow if interest rates jump by 1%? What if I have a void for six weeks instead of the four I budgeted for? A proper analysis accounts for the worst-case scenario, not just the rosy best-case.

- Is my ROI genuinely attractive? Does the return on your invested cash actually justify the risk, the hassle, and the time involved? Stack it up against other potential investments to be sure it's the best home for your funds.

- Have I accounted for all UK tax implications? Have you properly modelled the impact of Section 24 on your specific tax bracket? This single factor can be the difference between a profitable deal and a financial headache.

- Does this property fit my long-term strategy? Are you chasing high monthly cash flow, long-term capital growth, or a blend of the two? Make sure this specific deal is a step towards your bigger portfolio goals, not a distraction.

The ultimate goal of a detailed financial breakdown is to move from uncertainty to clarity. It transforms you from a speculative buyer into a strategic investor who understands every angle of the deal, from the upfront costs to the long-term profitability.

In a fast-moving property market, using sharp, accurate tools isn't a luxury; it's a necessity. Mastering this level of financial analysis is what separates the successful investors from everyone else. It gives you the foundation you need to build a resilient and profitable UK property portfolio, one well-calculated deal at a time. The confidence you get from a thorough buy to let calculator uk analysis is the final green light you need to move forward.

Frequently Asked Questions About Buy-to-Let Calculations

When you start digging into property investment analysis, a few key questions always pop up. Let's tackle some of the most common queries investors have when using a buy-to-let calculator uk to vet a potential deal.

What Is a Good Rental Yield in the UK?

There's no single magic number, but many UK investors use a gross rental yield of 6% or higher as a rough benchmark. At that level, a property usually has enough income potential to generate positive cash flow after you've paid all the bills.

Of course, it's not that simple. Yields vary hugely across the country. In big cities like London, you might see yields closer to 4-5%, where investors are often counting on long-term capital appreciation to do the heavy lifting. Head up to some cities in the North and the Midlands, and you can find gross yields pushing 7-9% or even more.

But the number that really matters is the net yield. This is what a good buy-to-let calculator uk will give you after stripping out all your running costs. It's the true measure of a property's profitability. If you want to get this right, you can learn more about how to calculate rental yield in the UK.

How Does Section 24 Impact My Buy-to-Let Profit?

For higher and additional-rate taxpayers, Section 24 is a game-changer. It has a massive impact on your bottom line. Before this rule came in, you could deduct your full mortgage interest payments from your rental income, which lowered your taxable profit. Simple.

Now, you can't deduct that interest as a business expense anymore. Instead, you get a tax credit equal to 20% of your mortgage interest payments.

For a 40% taxpayer, this is a critical change. It means you pay tax on income that was previously shielded by interest costs, significantly reducing your final net profit and, in some cases, pushing a profitable deal into a loss-making one. It is essential your calculator models this correctly.

Can a Standard Calculator Handle HMO or BRRRR Deals?

Honestly, no. Most of the basic online calculators you find are built for simple, single-tenancy buy-to-lets. They fall apart when you throw more complex strategies at them.

- HMOs (Houses in Multiple Occupation): These deals involve multiple tenancies, much higher running costs, and specific licensing rules. A standard calculator just can't model that level of detail properly.

- BRRRR (Buy, Refurbish, Rent, Refinance, Repeat): The entire profitability of this strategy hinges on the refinance step. The amount of capital you pull back out completely changes the Return on Investment (ROI) calculation, and a basic tool won't handle that.

For these more advanced scenarios, you need something built for the job. An app like DealSheet AI has dedicated templates to accurately model the unique finances and cash flows of each strategy, so you're not just guessing.

Ready to analyse your next deal with precision and speed? DealSheet AI replaces guesswork with a powerful, UK-focused analysis engine. Get started with a free trial and see the real numbers behind any property in seconds. Download the app today from the Apple App Store.