Property Investment for Beginners UK: Your 2026 Guide

Property Investment for Beginners UK: Your 2026 Guide

Starting your property investment for beginners UK journey is about one core principle: buying assets that provide reliable income and grow in value. The key to success isn't timing the market perfectly; it's about understanding the fundamentals to make smart, data-led decisions. This guide will walk you through the essential steps, from financing and strategy to analysing your first deal for 2026.

To fast-track your analysis and evaluate potential investments in seconds, a specialist tool like the DealSheet AI app is a game-changer for any serious beginner.

Starting Your UK Property Investment Journey

This guide is your roadmap. We're going to cut through the jargon and focus on what actually matters: cash flow, capital growth, and managing your risk. The goal is to give you the strategic mindset you need to navigate the UK property market with confidence, turning your ambition into a real, tangible portfolio.

The journey starts with understanding the ground beneath your feet. For anyone looking to invest in 2026, the market is showing some reassuring signs of stability.

A Stable Foundation for New Investors

Recent market data offers a welcome bit of calm for those just starting out. The UK housing market held remarkably steady throughout 2025, with both asking prices and completed sales showing predictable patterns that should give new investors some confidence.

For instance, one set of data showed average asking prices grew by just 1.2% over the year, a sign of a maturing, less frantic market. This kind of price stability creates a much more predictable environment for a beginner trying to run the numbers on a deal and forecast their returns. You can dig into the full report and learn more about recent market stability findings here.

That stability is a huge advantage. It means you can focus on the fundamentals of what makes a good deal, rather than trying to gamble on wild market swings.

A successful property investment portfolio isn't built on speculation. It's built on a series of well-analysed, logical decisions that prioritise sustainable cash flow and long-term asset appreciation.

What This Guide Will Cover

To help you make those logical decisions, this guide breaks down the essential pillars of UK property investment for beginners. We'll walk you through:

- Core Concepts: Getting to grips with key terms like yield, ROI, and leverage without the textbook dryness.

- Investment Strategies: Comparing popular approaches like a standard Buy-to-Let versus something more involved like BRRRR.

- Financing Your Deal: Understanding the nuts and bolts of mortgages, deposits, and what lenders are actually looking for.

- Taxes and Regulations: A no-nonsense look at Stamp Duty, Section 24, and your duties as a landlord.

- Finding and Analysing Deals: A practical guide to sourcing opportunities and, most importantly, running the numbers properly.

Before we dive in, it's crucial to understand the importance of a repeatable process. Finding the right opportunities is the critical first step. You can also explore our detailed article on what professional property sourcers need to deliver to get a head start on what separates a great investment from a dud.

Understanding the Core Concepts of Property Investment

Before you can even think about analysing a deal, you need to speak the language of property. For anyone starting out with property investment for beginners UK, this is the first and most critical step.

It's not about memorising complex financial theory. It's about understanding the handful of metrics that tell you whether a property is a solid asset or a ticking financial time bomb. Think of it like learning the basic rules of a game before you start playing – once you grasp these, you can look at any opportunity and make decisions based on numbers, not just a gut feeling.

The Key Metrics on Your Deal Scorecard

When you first start looking at deals, you'll be hit with a wall of jargon. Don't worry. Most of it boils down to a few simple ideas that measure how a property performs and how your own cash is working for you.

To keep things simple, here's a quick breakdown of the core numbers you'll see on every deal analysis.

Key UK Property Investment Metrics Explained

| Metric | What It Measures | Why It Matters for a Beginner |

|---|---|---|

| Gross & Net Yield | The property's annual rental income as a percentage of its value. Net Yield includes running costs; Gross Yield does not. | Yield is like the property's annual "salary". Always focus on Net Yield – it's the realistic figure that shows what the asset actually earns after expenses. |

| Cash Flow | The actual money left in your bank account each month after collecting rent and paying all bills, including the mortgage. | This is the lifeblood of your portfolio. Positive cash flow means the property pays for itself and you. Negative cash flow means you're paying to own it. |

| Return on Investment (ROI) | The return you get on the actual cash you've put into the deal (deposit, fees, refurb costs). | ROI is your personal scorecard. It answers the most important question: "How hard is my money working?" A high ROI means your capital is being used efficiently. |

| Capital Growth | The increase in the property's market value over time. | This is your long-term wealth builder. You usually only "cash in" on this when you sell or refinance, but it's what creates serious net worth over a decade or more. |

Understanding these four concepts is non-negotiable. They are the foundation upon which every single investment decision is built. Let's dig into what they mean in the real world.

Yield: The Annual Salary of Your Property

The first term you'll hear thrown around constantly is yield. In the simplest terms, it's the return you get from rent each year, shown as a percentage of the property's price. Think of it as the annual salary your property pays you just for owning it.

You'll come across two main types:

- Gross Yield: This is the back-of-a-napkin calculation. You just take the total annual rent and divide it by the purchase price. It's easy, but it's a fantasy figure because it ignores all your costs.

- Net Yield: This is the number that actually matters. It takes the same annual rent but first subtracts all your running costs – think mortgage interest, insurance, maintenance, and agent fees – before dividing by the purchase price.

As a beginner, you should get into the habit of ignoring gross yield and focusing entirely on the net. It gives you a much truer picture of how the asset is actually performing. For a deeper dive, check out our guide on how to calculate rental yield in the UK.

ROI: The Real Scorecard for Your Cash

While yield measures the property's performance, Return on Investment (ROI) measures your performance. It cuts to the chase and answers the most important question: how hard is the actual money you pulled from your bank account working for you?

ROI calculates your annual profit (your net rental income) as a percentage of the total cash you put in. That includes your deposit, stamp duty, legal fees, and any money spent on refurbishment. It is the ultimate scorecard for your investment.

A property might have a decent 5% net yield, which sounds okay. But if you had to put in a massive deposit to get it, the ROI on your personal cash might be a dismal 2%. The best deals give you a high ROI because they make your capital work efficiently.

Capital Growth and Cash Flow: The Two Engines of Wealth

Property builds wealth in two distinct ways. Understanding the difference is mission-critical for any beginner investor in the UK.

-

Capital Growth: This is simply the increase in the property's value over time. It's a long-term play, and you typically only see the benefit when you sell or refinance. While nothing is guaranteed, UK property has a strong track record of long-term appreciation.

-

Cash Flow: This is the cash left in your pocket each month after you've collected the rent and paid every single bill, including your mortgage. Positive cash flow is the absolute lifeblood of a sustainable portfolio. It means the property funds itself and pays you an income.

On the flip side, negative cash flow means you have to top up the property's expenses from your own salary each month. That's a fragile and risky position to be in.

For almost every beginner, the safest and smartest strategy is to prioritise positive cash flow. It makes your portfolio resilient, able to withstand interest rate rises or surprise repair bills without putting your personal finances at risk. Think of capital growth as the fantastic bonus you get on top of a solid, cash-flowing foundation.

Choosing the Right Investment Strategy for You

Let's get one thing straight: there's no single "best" way to invest in property. The right path for you is the one that actually fits your bank balance, your goals, and how much time you can realistically spare. One person's perfect hands-off investment is another's missed opportunity.

The key is finding a strategy that works for your life. Before you get bogged down in spreadsheets, a tool like the DealSheet AI app can be a massive help, letting you model different scenarios and compare the numbers in minutes.

This section breaks down the most common routes you'll come across, from the steady, income-focused world of Buy-to-Let to the more intense methods designed to build a portfolio fast.

Before we dive in, here's a quick overview to help you compare the main players at a glance. Think of this as a menu to help you decide which direction to explore first.

Beginner Investment Strategy Comparison

| Strategy | Best For | Typical Upfront Capital | Time Commitment |

|---|---|---|---|

| Standard Buy-to-Let (BTL) | Beginners seeking steady, long-term rental income and gradual capital growth. | 25% deposit + stamp duty, legal fees, and a small contingency. | Low, once a good tenant is in place (especially with a letting agent). |

| Buy, Refurbish, Refinance, Rent (BRRRR) | Investors with more time who want to rapidly scale their portfolio by recycling capital. | Deposit + full refurbishment costs + holding costs for several months. | High. This is a very active, project-management-heavy strategy. |

| House in Multiple Occupation (HMO) | Investors focused on maximising monthly cash flow from a single property. | Deposit + conversion/compliance costs (can be significant). | Medium to High. Involves intensive management and strict regulations. |

| Flipping (Buy-to-Sell) | Experienced investors aiming for a quick, lump-sum profit through renovation and resale. | Purchase price + refurb costs + holding costs. Often needs cash or bridging finance. | Very High. More of a full-time job than a passive investment. |

As you can see, the trade-off is usually between your time, your capital, and the speed of your returns. Let's look at each one in a bit more detail.

Standard Buy-to-Let (BTL): The Foundation

This is the bread and butter of UK property investment and the most common place to start. The idea couldn't be simpler: you buy a property, rent it out, and the monthly rent covers your mortgage and other costs, leaving you with a profit.

- Best For: Beginners after a relatively straightforward, long-term investment focused on steady rental income and gradual capital growth.

- Time Commitment: Pretty low once a tenant is settled, especially if you hire a letting agent. The real work is finding and buying the right property.

- Capital Required: You'll typically need a 25% deposit on the property's value, plus money for Stamp Duty, legal fees, and a small emergency fund.

The appeal here is predictability. You're not trying to pull off complex financial manoeuvres; you're just providing a good home in return for a consistent income stream.

BRRRR: The Portfolio Builder

The Buy, Refurbish, Refinance, Rent (BRRRR) method is a much more active and hands-on approach. It's all about buying a property that needs work (often for less than it's worth), adding value with a good renovation, and then refinancing it based on its new, higher value. The goal is to pull out most, or even all, of your initial cash to roll into the next deal.

BRRRR is essentially a way to recycle your capital. Instead of leaving your deposit locked up in one property for years, you're actively working to get it back out so you can build a portfolio much faster than with standard BTLs.

- Best For: Investors with more time on their hands, a stomach for managing projects, and the ambition to scale up quickly.

- Time Commitment: High. This is not a passive strategy. You're finding rundown properties, managing builders, and dealing with two rounds of financing.

- Capital Required: You'll need cash for the deposit, the entire refurbishment budget, and holding costs (mortgage, bills, insurance) for the months it takes before you can refinance.

HMOs: Maximising Your Cash Flow

A House in Multiple Occupation (HMO) is a property rented out room-by-room to at least three people who aren't from the same family but share facilities like the kitchen. This strategy can squeeze out a much higher rental income from a single property compared to a standard BTL.

But there's a catch. HMOs come with far more intensive management and a mountain of extra regulations, including special licenses from your local council. They can be a cash flow machine, but they demand a lot more from you as a landlord.

Strategies like BTL and HMOs are looking particularly solid, with the rental market continuing to grow. In fact, forecasts for 2026 predict a 4.0% average increase in UK rents. Some cities are doing even better – Liverpool's rental yields are projected to hit an incredible 9.2% in 2026, showing the kind of returns possible in the right location. You can explore the full rental yield forecast for 2026 and beyond to see how different regions are stacking up.

Flipping: For Quick Capital Gains

Property flipping is a completely different beast. Here, you couldn't care less about rental income. The entire game is about making a quick, lump-sum profit. You buy a property, renovate it fast to force the value up, and sell it on the open market, ideally within a few months.

This is a high-risk, high-reward play. Your success hinges entirely on your ability to budget works accurately, manage tradespeople without delays, and read the local sales market perfectly. It's more like trading than long-term investing, and your profit gets hit with Capital Gains Tax. For most beginners, building a solid base of stable rental properties first is a much safer bet.

How to Finance Your First Property Investment

Securing the right finance is the engine that powers your property investment journey. For most beginners in the UK, this means getting to grips with a specific type of loan known as a buy-to-let (BTL) mortgage.

This isn't the same as the residential mortgage you might have on your own home. Lenders view it purely as a business transaction, and they assess it very differently.

The process might seem intimidating, but lenders are primarily interested in two things: the property's ability to generate enough rent and your credibility as a borrower. Understanding what they look for is the key to presenting a strong application and getting your first deal over the line.

The Cornerstones of a Buy-to-Let Mortgage

Lenders need to be confident that their loan is a safe bet. To do this, they have a clear set of criteria you'll need to meet. Getting your ducks in a row before you apply will make the entire process smoother and significantly increase your chances of success.

The three main pillars of any BTL mortgage application are:

- The Deposit: Unlike residential mortgages, you'll need a much larger down payment. Lenders typically require a minimum of 25% of the property's purchase price, though some may ask for more depending on the deal.

- Rental Income Stress Test: This is a crucial calculation. Lenders need to see that the expected rent can comfortably cover the mortgage payments, even if interest rates rise. They often require the monthly rent to be at least 125% to 145% of the mortgage payment, calculated at a higher "stress test" interest rate.

- Your Credit History: A clean credit file is non-negotiable. Lenders will scrutinise your financial history to ensure you have a track record of managing debt responsibly.

Lenders are fundamentally risk-averse. A strong deposit, positive rental coverage, and a clean credit score signal to them that you are a reliable and low-risk borrower, making them much more likely to approve your application.

Repayment vs Interest-Only Mortgages

When you get a BTL mortgage, you'll usually choose between two repayment structures. While a repayment mortgage (where you pay back both capital and interest each month) feels familiar, many seasoned investors opt for an interest-only mortgage.

With an interest-only product, your monthly payments only cover the interest on the loan, not the capital itself. This results in significantly lower monthly outgoings, which in turn maximises your monthly cash flow.

The trade-off is that at the end of the mortgage term, you still owe the original loan amount. This is typically paid off by selling the property or refinancing. For investors focused on generating income, this is often the preferred route.

Alternative Funding Routes

Standard BTL mortgages aren't the only way to finance a deal, especially for properties that aren't immediately rentable. For properties bought at auction or those needing a heavy refurbishment, a bridging loan is a common short-term solution.

Bridging loans are faster to arrange but come with higher interest rates. They "bridge" the financial gap until you can either sell the property (a "flip") or refinance onto a standard BTL mortgage once the works are complete.

For a more detailed breakdown, you can explore how to use a bridging loan calculator to model your costs.

Finally, a good independent mortgage broker is an invaluable ally. They have access to deals not available on the high street and can match you with lenders who understand and favour property investors. Their expertise can save you a huge amount of time, money, and stress.

Getting to Grips with UK Property Taxes and Regulations

Understanding the UK's tax and legal landscape isn't just a box-ticking exercise; it's fundamental to protecting your profits. Getting this wrong can turn a great deal into a financial headache, so it's something any serious investor needs to nail from day one.

The first major cost you'll hit is Stamp Duty Land Tax (SDLT). This is the tax paid when you buy property over a certain price in England and Northern Ireland.

Crucially for investors, any purchase of an additional residential property gets hit with a 3% surcharge on top of the standard SDLT rates. This can add thousands to your upfront costs and absolutely must be factored into your deal analysis. To avoid any nasty surprises, it's vital to learn more about what Stamp Duty Land Tax is and how it's calculated before you even think about making an offer.

The Impact of Section 24

One of the biggest game-changers for individual landlords in recent years was the introduction of Section 24, often called the 'tenant tax'. It used to be simple: you could deduct all your mortgage interest costs from your rental income before working out your tax bill.

Now, you can only claim a basic rate tax credit of 20% on your mortgage interest payments. This change has hammered higher and additional-rate taxpayers, massively increasing their taxable income and even pushing some into a higher tax bracket altogether. This is the main reason why so many investors now buy property through a limited company, where mortgage interest is still treated as a fully deductible business expense.

Operating as a limited company can be far more tax-efficient, especially if you're a higher-rate taxpayer. However, it comes with its own admin costs and sometimes higher mortgage rates. Always get advice from a qualified property accountant to figure out the right structure for your personal situation.

Capital Gains Tax and Your Duties as a Landlord

When you eventually sell an investment property, you'll likely face Capital Gains Tax (CGT) on the profit you've made. It's calculated on the difference between what you bought it for and what you sold it for. The allowance and rates can change, so you need to keep on top of the rules to manage your tax bill effectively.

Beyond the numbers, being a landlord carries serious legal duties designed to keep tenants safe. These are not optional extras; they are legal requirements.

- Gas Safety: A Gas Safe registered engineer must check all gas appliances every year, and you have to give the certificate to your tenants.

- Electrical Safety: An Electrical Installation Condition Report (EICR) is required at least every five years.

- Deposit Protection: You must protect any tenant deposit in a government-approved scheme within 30 days of getting it.

- Right to Rent: It's your job to check that your tenants have the legal right to rent in the UK.

The rental market is also getting more competitive. With over £3.2 billion poured into the UK's build-to-rent sector in 2024 alone, big corporate buyers are now hunting in the same sub-£250,000 property space as beginners. These larger players have tax structures that can make it tougher for individual landlords to compete, making sharp, accurate deal analysis more critical than ever. You can discover more insights about institutional investment trends here.

How to Find and Analyze Your First Deal

This is where the rubber meets the road. All the reading about strategies and finance boils down to one repeatable skill: finding a potential investment and running the numbers to see if it actually works. Get this right, and you have a business. Get it wrong, and you have an expensive hobby.

Mastering deal analysis is non-negotiable. It's the critical process that stops you from making emotional decisions, ensuring every purchase is driven by cold, hard data, not just a good feeling about the kitchen.

Sourcing Deals Beyond the Main Portals

Everyone starts on Rightmove or Zoopla, but the truly great deals are rarely found sitting there waiting for you. To get an edge, you need to dig a little deeper and build a network.

- Local Estate Agents: Don't just sign up for email alerts. Actually go and meet the agents in your target area. Build a real rapport and prove you're a serious buyer with your finances in order. They know about properties long before they hit the web.

- Property Auctions: Auctions can be a fantastic place to find properties below market value, but they are not for the faint-hearted or unprepared. You have to do all your homework and have your funding locked down before you even think about bidding.

- Direct-to-Vendor: This is old-school but effective. It involves contacting landlords or homeowners directly, often with leaflets or targeted letters, to see if they might consider selling. It takes more legwork but can unearth opportunities no one else knows about.

A Simple Framework for Analysing a Deal

Once you've found a potential property, you need to "analyse" it. That's just a fancy way of saying you need to calculate all the potential income against all the likely costs to see what profit is left.

Underwriting is the safety check that separates professional investors from hopeful amateurs. It forces you to account for every cost, not just the obvious ones, transforming a guess into a calculated business decision.

Here's a simplified step-by-step process to get you started:

- Calculate Gross Yield: This is your first, quick look. Take the expected monthly rent, multiply it by 12, then divide that number by the property's purchase price. It's a rough-and-ready metric for comparing the initial potential of different deals.

- Estimate All Costs: This is the most important step, and you have to be brutally realistic. Your list must include the mortgage payment, insurance, letting agent fees (which are typically 8-12% of the rent), an annual budget for maintenance, and a contingency for "voids" (those empty periods between tenants).

- Determine Net Cash Flow: Now, subtract your total monthly costs from your monthly rental income. The figure left over is your net cash flow. This is the actual profit that will land in your bank account each month.

- Calculate Your ROI: Finally, take your annual net cash flow and divide it by the total cash you actually put in (your deposit, stamp duty, legal fees, and any refurbishment costs). This number, the Return on Investment, tells you how hard your own money is working for you.

For those ready to move from theory to practice, our complete guide to analysing UK buy-to-let deals in 2026 provides a more detailed walkthrough with worked examples.

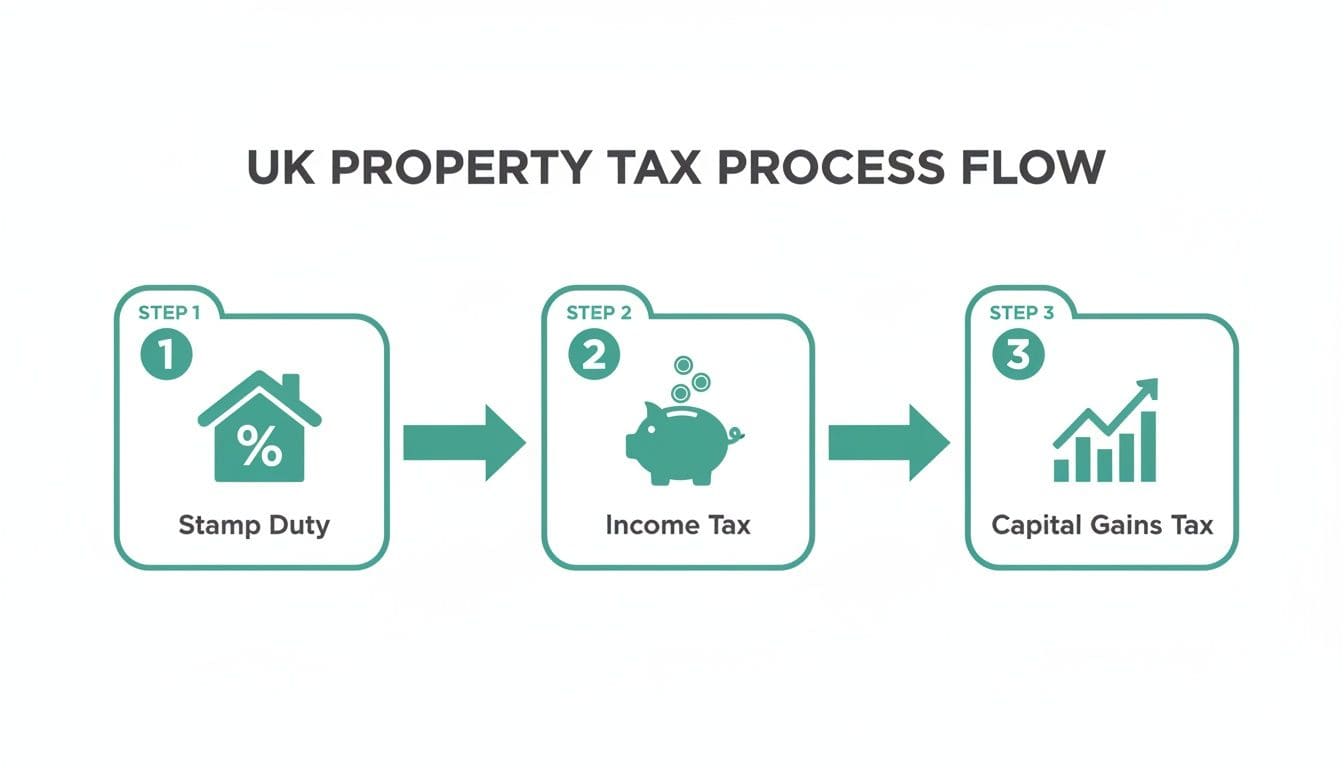

Running the numbers on a property investment means navigating a few key financial checkpoints, especially the big three UK property taxes: Stamp Duty, Income Tax, and Capital Gains Tax.

This flowchart gives you a simple map of the tax journey for a typical investor. It highlights the main liabilities you need to account for at each stage of buying, holding, and eventually selling your property.

Got Questions? Let's Get Them Answered

Diving into the world of property investment is exciting, but it's completely normal to have a few nagging questions before you take the plunge. Think of this section as clearing up the last few bits of uncertainty, so you can move forward with confidence.

We'll tackle some of the most common queries we hear from new investors, giving you straight, practical answers to get you started on the right foot.

How Much Money Do I Actually Need to Get Started?

There's no magic number, but let's talk reality. For most beginners looking to buy in 2026, you'll want to have access to between £30,000 and £50,000.

What does that cover? It's usually enough for:

- A 25% deposit on a solid starter property in an affordable UK region, likely in the £100,000–£150,000 price range.

- The legal fees and Stamp Duty Land Tax (SDLT) that come with the purchase.

- A small pot of cash set aside for any initial touch-ups or unexpected costs that pop up.

Of course, this all hinges on the property prices in the area you've targeted.

Should I Invest Through a Limited Company?

This is a big one, and the answer almost always comes down to tax. While buying in your personal name is simpler from an admin point of view, it can be a painful mistake for higher-rate taxpayers thanks to the Section 24 mortgage interest relief changes.

Here's the crucial difference: investing through a limited company lets you offset 100% of your mortgage interest against your rental income before you pay tax. If you own it personally, you only get a basic 20% tax credit on that interest.

The trade-off? Limited companies mean more paperwork and sometimes slightly less competitive mortgage rates. This isn't a decision to make lightly. You absolutely need to sit down with a specialist property accountant who can run the numbers for both scenarios and show you what makes sense for your financial situation.

What Are the Biggest Risks for a New Investor?

Every investment has risks, but the good news is that the most common traps for new property investors are avoidable with a bit of foresight. Here are the three big ones to watch out for:

- Negative Cash Flow: This is the nightmare scenario where an unexpected cost, like a new boiler, or a month without a tenant wipes out your profit and forces you to dig into your own savings. The fix? Keep a separate contingency fund with 3-6 months' worth of the property's total running costs.

- Overpaying for a Property: Getting caught up in the moment or rushing your analysis can lead you to pay more than a property is worth, kneecapping your returns from day one. You sidestep this by doing your homework properly and running your numbers conservatively, not optimistically.

- Problem Tenants: Dealing with late rent or property damage is a huge headache that can sour the whole experience. You minimise this risk with thorough tenant referencing, proper background checks, and solid landlord insurance. Don't cut corners here.

Ready to stop guessing and start analysing deals with precision and speed? The DealSheet AI app was built to give UK investors the confidence to make data-driven decisions in seconds, turning complex underwriting into a simple, repeatable process.

Stop getting bogged down in spreadsheets and start building your portfolio. Download the DealSheet AI app from the App Store and begin your 3-day free trial today.