How to Calculate Property Rental Yield in the UK: A Landlord's Guide

How to Calculate Property Rental Yield in the UK: A Landlord's Guide

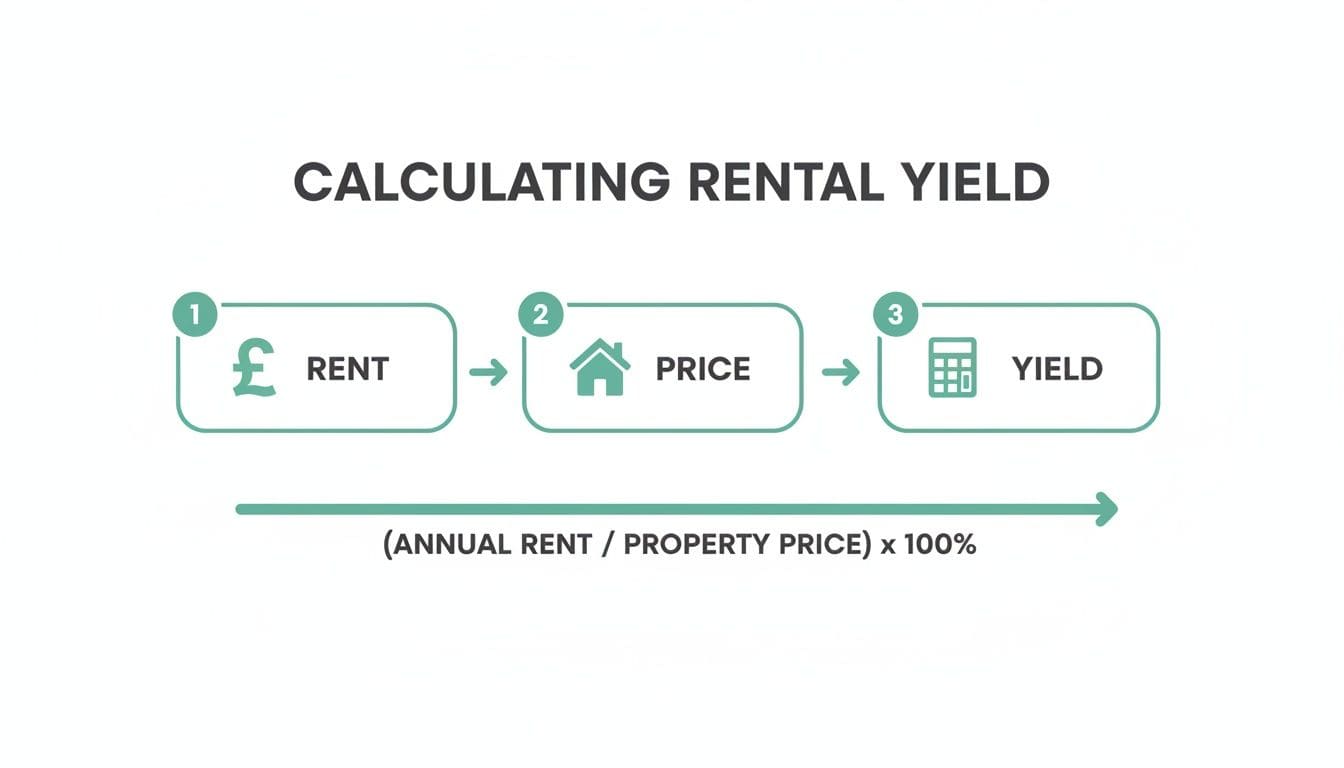

To learn how to calculate property rental yield in the UK, the quickest method is the Gross Yield formula: (Annual Rent ÷ Property Price) x 100. This calculation provides an instant snapshot, allowing you to compare potential property investments rapidly. For example, a £250,000 property renting for £1,250 a month gives a gross yield of 6%. However, this is just the starting point for a true analysis. To skip the manual calculations and get an instant, accurate analysis of any UK property deal, download the DealSheet AI app.

While that gross figure gives you a rapid snapshot, it doesn't reveal true profitability. To understand if a UK property investment is genuinely profitable, you must dig deeper into the numbers that matter: Net Yield and Cash-on-Cash Return. This guide will break down each calculation with real UK scenarios, revealing the hidden costs that separate profitable investments from costly mistakes.

This simple diagram shows you the basic inputs for that initial gross yield calculation.

At its core, yield is the relationship between the rent coming in and the price you paid. But the devil, as always, is in the detail.

Calculating property rental yield is a cornerstone skill for any UK buy-to-let investor. For instance, if you buy a flat in Manchester for £200,000 and it pulls in £12,000 in yearly rent, your gross yield is 6%. Data from the ground shows that certain postcodes can deliver yields of 7-9% using this exact calculation.

But knowing your numbers is only half the battle; you also need to know what makes a strong return in today's market. If you're wondering where the goalposts are, you might find our guide on what is a good rental yield useful.

The DealSheet AI app automates every single calculation for UK investors—from Stamp Duty and running costs to Section 24 tax implications—turning hours of painful analysis into moments of clarity. We'll show you how it works as we go through this guide.

Calculating Gross Yield for Fast Initial Screening

When you're scrolling through dozens of property listings on Rightmove or Zoopla, you need a fast, reliable way to sort the promising deals from the duds. This is where the gross yield calculation becomes your best friend. It's the essential first step in learning how to calculate property rental yield, designed for pure speed and simplicity.

Gross yield helps you answer one simple question: "Is this deal even worth a closer look?" It strips away all the complex running costs and gives you a raw, top-line figure to compare properties on a level playing field.

This metric focuses on just two numbers: the annual rental income and the property's purchase price. By ignoring expenses for a moment, you can rapidly assess a property's income-generating potential relative to its cost.

The Simple Gross Yield Formula

The calculation itself is refreshingly straightforward. You take the total rent you expect to collect over a year and divide it by the property's purchase price. Then, just multiply that figure by 100 to get your percentage.

Gross Yield Formula: (Annual Rental Income ÷ Purchase Price) x 100 = Gross Yield %

It's crucial to use the annual rent, not the monthly figure. This is a common mistake that can throw your numbers off completely. Just multiply the monthly rent by 12 to get the correct annual figure before you do anything else.

A Worked Example in Leeds

Let's put this into practice with a real-world UK scenario. Imagine you've spotted a three-bedroom terrace house for sale in a popular rental area of Leeds, like Headingley or Armley.

- Purchase Price: £225,000

- Expected Monthly Rent: £1,100

First, work out the annual rental income: £1,100 (monthly rent) x 12 (months) = £13,200 (annual rent)

Now, plug these numbers into the formula: (£13,200 ÷ £225,000) x 100 = 5.866...%

The gross rental yield for this Leeds property is 5.87% (rounded up). This single number now allows you to compare this property against others in Leeds or even in different cities like Manchester or Birmingham, without getting bogged down in the finer details just yet.

If you want to see more detailed examples, you can find them in our comprehensive UK rental yield calculator guide.

What Is a Good Gross Yield in the UK?

What you consider a "good" gross yield really depends on your investment strategy and, critically, the property's location. In the UK, there's a well-known geographical divide when it comes to yields.

- Northern England & Scotland: In cities like Liverpool, Glasgow, and Newcastle, investors often hunt for higher yields, typically aiming for 7% or more. These areas often have lower property prices relative to rental income, making strong cash flow the main prize.

- The Midlands & Wales: Areas around Birmingham and Cardiff can offer a balanced profile. Here, respectable yields often fall in the 5% to 7% range.

- South East & London: In the capital and its surrounding commuter towns, property prices are significantly higher. Yields are naturally compressed, and anything above 4-5% can be considered pretty strong. Investors in these regions are often prioritising long-term capital appreciation over immediate rental income.

Remember, gross yield is your first pass, not your final decision. A property with a stellar 9% gross yield might have hidden structural issues or be in a low-demand area, leading to high maintenance costs and painful void periods.

Conversely, a London property with a 3.5% yield might offer excellent capital growth prospects that more than make up for the lower monthly income.

This initial calculation is purely a screening tool. It helps you build a shortlist of properties that meet your baseline criteria, saving you from wasting time analysing deals that will never stack up financially.

Mastering Net Yield to Reveal True Profitability

If gross yield is the quick handshake, net yield is the deep conversation that follows. This is the metric that separates serious property investors from speculators, moving beyond an attractive top-line number to answer the most critical question of all: "Will this property actually make me money?"

Frankly, while gross yield helps you build a shortlist, net yield is what you use for deep analysis. It forces you to account for every single running cost, revealing the true profitability and cash flow potential of a deal. Ignore this step, and you're investing blind.

Net Yield Formula: (Annual Rental Income - Annual Operating Expenses) ÷ (Total Investment Cost) x 100 = Net Yield %

This formula is more involved because it reflects the reality of being a landlord. Rent doesn't just land in your bank account untouched; it gets chipped away by dozens of necessary expenses.

The Anatomy of Operating Expenses

To master the net yield calculation, you have to become a detective of costs. So many new investors get caught out by underestimating the sheer number of deductions that eat into their rental income. Let's break down the most common (and often forgotten) operating expenses you need to factor in.

This checklist covers the typical costs you'll face as a UK landlord. Forgetting even one of these can turn a profitable-looking deal into a financial drain.

Your UK Landlord Operating Expenses Checklist

| Expense Category | Description and UK Context | Typical Cost Range |

|---|---|---|

| Mortgage Interest | This is often the largest single expense. Crucially, under Section 24 rules, you can no longer deduct the full mortgage interest cost from your rental income to reduce your tax bill. You now receive a 20% tax credit instead, which is a significant consideration for higher-rate taxpayers. | Varies based on loan size and interest rate. |

| Letting Agent Fees | If you're not self-managing, you'll pay a fee. This typically includes a tenant-find fee (e.g., one month's rent) and an ongoing monthly management fee. | 8% to 15% of monthly rent for full management. |

| Insurance | Standard home insurance isn't sufficient. You need specialist landlord insurance, which covers buildings, liability, and potentially loss of rent. | £150 to £400+ per year, depending on property type and location. |

| Maintenance & Repairs | This is a big one. A good rule of thumb is to budget at least 1% of the property's value annually for repairs. For a £250,000 property, that's £2,500 a year. This covers everything from a broken boiler to a leaky tap. | 1% of property value annually or 10% of annual rent. |

| Void Periods | No property is occupied 100% of the time. You must account for periods between tenancies when no rent is coming in. Budgeting for one month of vacancy per year is a prudent approach. | 4% to 8% of annual rent. |

| Ground Rent & Service Charges | For leasehold properties (like most flats), these are unavoidable annual fees paid to the freeholder for the maintenance of communal areas. They can range from negligible to thousands of pounds. | £100 to £5,000+ per year. |

| Safety Certificates | UK law mandates several safety checks, including an annual Gas Safety Certificate (CP12) and an Electrical Installation Condition Report (EICR) every five years. | £70-£100 for Gas Safety, £150-£300 for EICR. |

Getting these expenses right is vital. While gross yield gives you a headline number, savvy UK portfolio landlords swear by net rental yield to reveal true profitability.

Recent HMRC statistics showed that UK landlords deducted a staggering £28 billion in expenses from £52 billion in rental income—an average cost ratio of 46%. This powerfully illustrates why you must move beyond gross figures to understand real returns.

Don't Forget About Acquisition Costs

A frequent and costly mistake is failing to include the upfront costs of buying the property in your total investment figure. The purchase price is only part of the story. Your 'Total Investment Cost' must also include all the one-off fees required just to get the keys.

These acquisition costs typically include:

- Stamp Duty Land Tax (SDLT): This is a significant tax on property purchases in England and Northern Ireland. For buy-to-let properties, you pay a higher rate, which can add thousands to your upfront cost.

- Legal Fees: You'll need a solicitor or conveyancer to handle the legal work of transferring ownership, which typically costs between £1,000 and £2,000.

- Survey Costs: A survey is essential to check the property's structural condition. A Level 2 or 3 survey can cost anywhere from £400 to £1,500.

- Mortgage Arrangement Fees: Lenders often charge a fee for setting up a buy-to-let mortgage, which can be added to the loan or paid upfront.

Forgetting these costs artificially inflates your yield calculation. Your true return is based on every single pound you had to spend to acquire and operate the asset. Because Stamp Duty is such a critical component, it's worth getting a precise figure; you can use our detailed guide to the Stamp Duty Land Tax calculator to work out exactly what you'll owe.

A Worked Example: A London Flat

Let's apply this to a real-world scenario to see how costs dramatically alter the final yield.

Imagine you're analysing a one-bedroom flat in Zone 3, London.

- Purchase Price: £400,000

- Monthly Rent: £1,800 (£21,600 per year)

- Acquisition Costs (SDLT, legal, etc.): £22,500

- Total Investment Cost: £400,000 + £22,500 = £422,500

At first glance, the gross yield looks appealing: (£21,600 ÷ £400,000) x 100 = 5.4%

Now, let's factor in the annual operating expenses to find the true net yield.

- Mortgage Interest: £8,000

- Letting Agent Fees (12%): £2,592

- Service Charge & Ground Rent: £2,000

- Insurance: £300

- Maintenance (budgeted): £1,500

- Void Period (budgeted 1 month): £1,800

- Safety Certs (annualised): £100

- Total Annual Operating Expenses: £16,292

With these costs, we can calculate the net rental income: £21,600 (Annual Rent) - £16,292 (Annual Expenses) = £5,308 (Net Annual Income)

Finally, we calculate the net yield using the Total Investment Cost: (£5,308 ÷ £422,500) x 100 = 1.26%

The difference is stark. The 5.4% gross yield has been whittled down to a 1.26% net yield. This figure gives you a far more honest assessment of the property's financial performance as a rental asset. This is the number you need to make an informed decision.

Unlocking Cash-on-Cash Return for Leveraged Investors

While net yield gives you an honest look at a property's operational profit, it doesn't answer the question that really matters to a leveraged investor: 'What's the return on the actual cash I've put in?'

This is where Cash-on-Cash Return (CoCR) becomes the ultimate metric. It cuts through the noise of the total property value and mortgage debt to focus purely on the performance of your capital.

For investors using finance, understanding CoCR is a non-negotiable part of learning how to calculate property rental yield properly. It reveals the true power of leverage, showing how a relatively small amount of your own money can control a much larger, income-producing asset. This is the calculation that separates the good deals from the truly great ones.

The formula is elegantly simple but incredibly powerful, focusing on your pre-tax cash flow relative to the total cash you actually invested.

Cash-on-Cash Return Formula: (Annual Pre-Tax Cash Flow ÷ Total Cash Invested) x 100 = CoCR %

Let's break down each component to make sure you get this calculation right every single time.

Defining the Two Core Components

To calculate CoCR accurately, you have to be precise about what goes into the numerator (your cash flow) and the denominator (your cash invested).

Annual Pre-Tax Cash Flow: This is the money left in your bank account at the end of the year before you've paid any income tax. Think of it as your gross rental income minus all your cash operating expenses, including your full mortgage payment (both the interest and principal components). It's essentially your net operating income minus your debt service.

Total Cash Invested: This is every single pound you personally had to pay out of pocket to acquire the property. It's not just your deposit. It's the sum of:

- Your mortgage deposit (e.g., 25% of the purchase price).

- Stamp Duty Land Tax (SDLT).

- All legal and conveyancing fees.

- Survey costs and mortgage arrangement fees.

- Any initial refurbishment costs needed to make the property rentable.

This figure represents your total "skin in the game." Getting this number right is absolutely critical for an accurate CoCR.

A Worked Example with a 75% LTV Mortgage

Let's run the numbers on a practical example to show how leverage dramatically impacts your return. We'll analyse a two-bedroom flat in Bristol purchased with a standard 75% loan-to-value (LTV) buy-to-let mortgage.

- Purchase Price: £300,000

- Monthly Rent: £1,500 (£18,000 per year)

- Mortgage: 75% LTV, meaning a £225,000 loan and a £75,000 deposit.

- Mortgage Payment (Interest-Only @ 5%): £937.50 per month (£11,250 per year).

First, let's nail down the Total Cash Invested:

- Deposit: £75,000

- SDLT (for a second property): £11,500

- Legal & Other Fees: £3,500

- Total Cash Invested: £75,000 + £11,500 + £3,500 = £90,000

Next, we calculate the Annual Pre-Tax Cash Flow. We'll use a realistic estimate for operating expenses (excluding the mortgage, which we'll handle separately).

- Annual Rent: £18,000

- Less Operating Costs (Insurance, Voids, Maintenance @ 20% of rent): £3,600

- Net Operating Income (NOI): £18,000 - £3,600 = £14,400

Now, we subtract the annual mortgage payments from the NOI:

- Annual Pre-Tax Cash Flow: £14,400 (NOI) - £11,250 (Mortgage) = £3,150

This £3,150 is the actual cash profit the property generates for you over the year.

Finally, we can calculate the Cash-on-Cash Return: (£3,150 ÷ £90,000) x 100 = 3.5%

So, for every pound you invested out of your own pocket, you're getting a 3.5% return in cash flow each year.

Why CoCR Reveals More Than Net Yield

This is where the magic happens. Let's imagine an investor bought the exact same Bristol property for £300,000 but paid entirely in cash. Their net yield would look quite strong. Their total investment cost would be £300,000 + £11,500 (SDLT) + £3,500 (fees) = £315,000.

Their net annual income (with no mortgage) would be £14,400.

The cash buyer's net yield would be: (£14,400 ÷ £315,000) x 100 = 4.57%

On paper, a 4.57% net yield looks better than the leveraged investor's 3.5% CoCR. But this comparison is misleading. The cash buyer had to tie up £315,000 of capital to achieve that return. The leveraged investor only had to deploy £90,000 of their own money.

Key Insight: The leveraged investor has freed up £225,000 in capital that can be used to purchase two more similar properties, potentially tripling their overall cash flow and diversifying their portfolio. This is the power that CoCR reveals.

This metric is especially critical when dealing with complex or short-term financing. For investors using bridging finance to secure a deal quickly before refinancing, calculating the projected CoCR is vital. You can learn more about the costs involved by using a reliable bridging loan calculator to model your initial financing expenses.

Cash-on-Cash Return is the true measure of capital efficiency. It shifts the focus from the property's performance to your money's performance. For any serious investor using finance, mastering this calculation is a fundamental step toward building a scalable and profitable UK property portfolio.

Avoiding Common and Costly Yield Calculation Mistakes

Learning how to calculate property rental yield is one thing, but sidestepping the small oversights that lead to big financial errors is another entirely. I've seen it time and again: the path to a profitable investment is littered with seemingly minor miscalculations that quietly eat away at your returns.

Knowing the common pitfalls is the first step to avoiding them.

Many investors, particularly when they're starting out, make optimistic assumptions that just don't hold up in the real world. A spreadsheet might look fantastic, but if it's built on flawed inputs, your shiny new investment could quickly become a liability.

Let's break down the most frequent—and costly—mistakes we see investors make.

Underestimating Voids and Maintenance

This is, without a doubt, the most common error. It's incredibly tempting to assume your property will be occupied 365 days a year and that nothing will ever break. This is a fantasy.

-

The Void Period Pitfall: No property has a 100% occupancy rate forever. Tenants move out, and finding new ones takes time. A prudent investor always budgets for at least one month of vacancy per year. If your annual rent is £12,000, you should be basing your calculations on £11,000 to build in a realistic buffer.

-

The Maintenance Mirage: Boilers fail. Fences blow down in a storm. Tenants report leaks. Ignoring these inevitable costs is a recipe for disaster. A widely accepted rule of thumb in the UK is the '10% rule'—budgeting 10% of your annual rent for maintenance and repairs. For a property bringing in £12,000 a year, that's £1,200 set aside for the unexpected.

Forgetting these two factors will make your net yield and cash flow projections dangerously inaccurate.

Ignoring the True Purchase Cost

Another frequent mistake is using the property's asking price or even the agreed sale price as the sole basis for your yield calculation. Your "Total Investment Cost" is always higher than the price tag you see on a property portal.

To get an accurate yield, you must include every single pound spent to acquire the asset. This means adding all acquisition costs—like Stamp Duty Land Tax (SDLT), solicitor fees, and survey costs—to the final purchase price. Failing to do so artificially inflates your return on investment figures.

For a second property in the UK, SDLT alone can add thousands of pounds to your upfront outlay. Overlooking this significantly skews your numbers and gives you a false sense of security about how well the deal actually performs.

Misunderstanding Section 24 Tax Rules

Since the full rollout of Section 24, UK landlords can no longer deduct their full mortgage interest costs from their rental income before calculating tax. Instead, you now receive a basic-rate tax credit of 20% on your mortgage interest payments.

This change has a profound impact, particularly for higher-rate (40%) and additional-rate (45%) taxpayers. It means you are taxed on your revenue before mortgage interest is accounted for, which can push some investors into a higher tax bracket and severely reduce, or even eliminate, their net profit.

Many online calculators and simple spreadsheets don't account for this critical UK-specific tax rule. Calculating your yield without modelling the impact of Section 24 can turn a profitable-on-paper deal into one that actually loses you money after tax.

How Technology Prevents These Mistakes

Manually accounting for every variable is tedious and, frankly, prone to human error. This is where tools designed specifically for property analysis become invaluable.

The DealSheet AI app, for example, is built for the UK market and prevents these mistakes by design. It automatically factors in realistic assumptions for void periods and maintenance. When you analyse a deal, it calculates the precise SDLT you'll owe and, crucially, models the impact of Section 24 on your final profit based on your personal tax rate.

This ensures your calculations are not just quick, but accurate and grounded in the realities of UK property investment.

Common Questions (and Traps) When Calculating UK Rental Yield

Even when you know the formulas, the real world of UK property investing throws up questions. The nuances of different markets, strategies, and costs can catch anyone out. Let's tackle the most common ones we see from both new and experienced investors.

Getting these details right isn't just academic—it's the difference between a deal that works on paper and one that actually puts cash in your bank account.

What Is a Good Rental Yield in the UK Today?

This is the number one question, and the only honest answer is: it depends entirely on your strategy and where you're buying. There's no single magic number, but here are the targets investors are typically chasing across the UK right now.

- High-Yield Focus (North/Midlands): In cities like Liverpool, Manchester, or Nottingham, investors are often hunting for gross yields of 7% or higher. The play here is usually all about cash flow, driven by lower purchase prices.

- Balanced Growth (South West/Major Regional Hubs): For places like Bristol or strong parts of Birmingham, a gross yield between 5% and 7% is often seen as a solid target. You're aiming for a blend of decent monthly cash flow and good prospects for capital growth.

- Capital Growth Focus (South East/London): In high-value postcodes, yields get seriously squeezed. A gross yield of 4% to 5% might be considered fantastic, because the main prize is long-term appreciation, not monthly profit.

Ultimately, a "good" yield is whatever works for your goals after you've stripped out every last cost and paid the taxman.

How Should I Factor in Refurbishment Costs?

This is a big one, especially for anyone using a BRRRR (Buy, Refurbish, Refinance, Rent) model. Forgetting the refurb budget will give you a dangerously optimistic Cash-on-Cash Return (CoCR).

Simple rule: the refurb spend is a core part of your "Total Cash Invested."

You need to add the entire renovation budget to your deposit, Stamp Duty, and legal fees. That gives you the real figure for your total cash outlay. For instance, if your deposit and fees come to £40,000 and you spend another £15,000 on a new kitchen and bathroom, your true Total Cash Invested is £55,000. Your CoCR must be calculated using that higher number.

Can I Trust the Yield Figures on Property Portals?

In a word: no. Treat the yield figures you see on portals like Rightmove or Zoopla as a vague signpost at best. They are almost always inflated, and here's why:

- They are always Gross Yields: They completely ignore the real-world costs of voids, management fees, maintenance, and insurance.

- They Use the Asking Price: The calculation is based on the asking price, not the lower price you'll hopefully negotiate.

- They Can Use Optimistic Rental Estimates: The estimated rent is often the absolute best-case scenario for the area, not the average.

Key Takeaway: Always, always run your own numbers. The advertised yield is a marketing hook, not a reliable financial metric. You have to plug the deal into the net yield and CoCR formulas to see if it actually works.

This is precisely why a proper analysis tool is so critical. It forces you to look past the shiny headline number and get to the truth of an investment's profitability.

Stop second-guessing and start making data-driven decisions. The DealSheet AI app automates every calculation we've discussed, from gross yield to post-tax cash flow, specifically for the UK market. Analyse any deal in seconds and avoid costly mistakes by downloading it from the App Store. Try DealSheet AI today.