A Beginner's Guide to Investing in Property in the UK for 2026

A Beginner's Guide to Investing in Property in the UK for 2026

Investing in property for beginners in the UK is one of the most effective ways to build long-term wealth, but succeeding in 2026 requires a smart, data-led strategy. The key to getting started isn't a huge initial fortune, but a solid plan that focuses on understanding the real costs, choosing high-yield locations, and analysing deals accurately. This guide provides the actionable framework you need to navigate the UK market with confidence. For those ready to analyse deals quickly and avoid costly mistakes, tools like the DealSheet AI app are essential for underwriting any UK property in seconds.

Starting Your UK Property Investment Journey

Embarking on your property investment journey is an exciting prospect. It promises passive income, your assets growing in value, and a real sense of financial security down the line. A lot of people hear "property investing" and immediately picture London's eye-watering prices, assuming it's a game only for the super-rich.

But that's a common misconception. The reality for most successful starters is found far from the capital.

The key to investing in property for beginners often lies in picking the right location. By targeting high-yield northern cities, you can get started with a total cash outlay of around £40,000-£55,000. That's a much more achievable goal and a world away from the six-figure deposits needed down south.

This guide is your roadmap to navigating the UK market with confidence.

Understanding the Initial Capital Needed

Before you even start looking at listings, you need a crystal-clear picture of the upfront cash required. It's more than just the deposit.

For a typical buy-to-let mortgage, most lenders will ask for a 25% deposit. Let's use a standard £200,000 investment property as an example.

Initial Costs for a UK Buy-to-Let Property

| Cost Component | Estimated Amount (£) |

|---|---|

| Purchase Price | £200,000 |

| 25% Deposit | £50,000 |

| Stamp Duty Land Tax (SDLT) | £2,500 |

| Legal Fees & Surveys | £2,000 |

| Total Initial Cash Required | £54,500 |

As you can see, the deposit is the biggest chunk, but the other costs add up fast. The total cash you'll need for a £200,000 property is around £54,500. It's also worth noting that most lenders will want to see a stable personal income of at least £25,000 a year (not including any future rent) and a clean credit history. You can find more details in this guide to UK property investment for 2026.

Success in property isn't about timing the market perfectly; it's about time in the market. Your first property is the launchpad, not the final destination. The goal is to get started with a solid, cash-flowing asset that builds your foundation.

Why Your First Property Matters So Much

Your first investment property sets the tone for your entire portfolio. It's a learning experience just as much as it is a financial asset.

A well-chosen first deal builds your momentum and confidence, making the second and third purchases feel much less daunting. On the flip side, a poor first choice can be a serious setback, both financially and mentally.

This is why meticulous planning and analysis are non-negotiable from day one. A successful first purchase should tick a few crucial boxes:

- Generate Positive Cash Flow: This is fundamental. After the mortgage, insurance, management fees, and a buffer for repairs are all paid, there should be money left over in your bank account each month.

- Offer Potential for Capital Growth: While monthly cash flow is king, choosing an area with strong fundamentals for long-term appreciation is how you build real wealth. To explore potential locations, check out our guide on the best cities for property investment.

- Build Your Experience: Your first deal teaches you the real-world mechanics of being a landlord—from screening tenants to handling that dreaded late-night call about a leaky boiler.

Finding Your Ideal Investment Strategy

Right, let's get to the most important decision you'll make: how are you actually going to invest? Property isn't a one-size-fits-all game. The best path for a busy professional wanting some passive income is worlds away from what an aspiring full-time investor needs to build a portfolio quickly.

Your choice here will dictate everything that follows—your potential returns, how much time you'll spend managing things, and even the type of mortgage you can get. By getting to grips with the most common UK property strategies, you can pick an approach that genuinely fits your financial goals, the time you have available, and how much risk you're comfortable with.

The Classic Buy-to-Let (BTL)

The standard Buy-to-Let is the one everyone knows. You buy a property and rent it out to a single family or individual, usually on a long-term contract of 12 months or more. It's the foundational model of property investing for a reason.

- Best For: Beginners looking for a relatively stable and hands-off income stream.

- Pros: It's simpler to get a mortgage for, easier to manage (especially with a letting agent), and tends to attract long-term tenants, which means less hassle and fewer empty periods.

- Cons: The monthly cash flow is lower than other strategies, and your returns can get squeezed by rising interest rates and taxes like Section 24.

Think of a standard two-bedroom flat in Bristol. It's likely to generate a steady, predictable income with minimal hands-on faff. Perfect for someone building wealth alongside a demanding career.

The High-Cashflow House in Multiple Occupation (HMO)

A House in Multiple Occupation (HMO) is where you rent out a single property to multiple tenants who aren't from the same family. Each person gets their own bedroom but shares communal spaces like the kitchen and living room.

This is where you can seriously ramp up the rental income. Imagine a four-bedroom house that might rent to a family for £1,500 a month. As an HMO, you could rent each of its four rooms for £600, bringing in a total of £2,400 per month (before bills).

This strategy supercharges your cash flow, but it comes with a trade-off. HMOs demand more intensive management, are subject to stricter licensing from the local council, and have higher setup costs to meet safety regulations.

The Flexible Serviced Accommodation (SA)

Serviced Accommodation (SA), which most people associate with platforms like Airbnb, means renting out a property on a short-term basis, much like a hotel room. You're providing a fully furnished space for guests staying for a few days or weeks, not months or years.

This approach offers the potential for the highest rental income, as nightly rates are way higher than long-term rents. But it's also the most hands-on strategy by a country mile.

- Management Intensity: Very high. You're dealing with constant guest communication, cleaning changeovers, and marketing.

- Income Volatility: Your earnings can swing wildly with the seasons, and you'll have more frequent empty periods (voids).

- Regulatory Hurdles: Many UK councils are cracking down on short-term lets, so checking the local rules is non-negotiable.

An SA property in a tourist magnet like York could make a fortune during peak season but might sit empty during the quiet winter months. It's a different beast entirely.

The Powerful BRRRR Method

The BRRRR method is a powerful way to build a portfolio rapidly. The acronym stands for Buy, Refurbish, Rent, Refinance, Repeat. The whole point is to recycle your initial investment cash to use on the next deal.

Here's the simple version:

- Buy: You find and purchase a property that's a bit tired and below its true market value.

- Refurbish: You renovate it to a high standard, forcing the value up.

- Rent: You let the property out to tenants at its new, higher market rent.

- Refinance: You get a new mortgage based on the property's increased post-renovation value.

- Repeat: You pull your initial investment back out (and sometimes more) to go again on the next project.

BRRRR demands more knowledge and a bigger appetite for risk, but it's one of the fastest ways to scale. You can dig into the details of each of these approaches by exploring different UK property investment strategies in our detailed guide. Choosing the right one is your first real step to success.

Mastering the Key Financial Metrics

Successful property investing is built on solid numbers, not vague guesswork. This section is your financial toolkit, breaking down the essential metrics you absolutely must master before even thinking about making an offer.

Forget complex spreadsheets for a moment and think of it this way.

Imagine your property is a simple fruit stall. The rent you collect is the money from selling apples. But to figure out if you're actually making a profit, you have to account for the cost of the stall (your mortgage), any spoiled apples that go unsold (void periods), and the flyers you use to get customers (letting agent fees). Getting your head around these numbers is the very core of investing in property for beginners.

Decoding Rental Yield

Rental yield is usually the first metric every investor learns. It's a quick-and-dirty way to measure your annual rental income as a percentage of what you paid for the property. But there are two types, and knowing the difference is vital.

Gross Yield is the simplest calculation of them all. It's just your total annual rent divided by the purchase price. Think of it as a quick way to compare the raw potential of different properties at a glance.

But Gross Yield is a vanity metric; it ignores all your running costs. This is where Net Yield steps in, giving you a much more realistic picture of your investment's health by factoring in all the expenses.

- Gross Yield: (Annual Rental Income / Property Purchase Price) x 100

- Net Yield: ( (Annual Rental Income - Annual Operating Costs) / Total Investment Cost ) x 100

These operating costs include everything from your mortgage interest and insurance to maintenance, management fees, and ground rent.

Return on Investment (ROI): The Ultimate Profit Metric

While yield is a great starting point, Return on Investment (ROI) tells you how hard your own cash is actually working for you. For any investor using a mortgage, this is arguably the most important number on the page.

ROI calculates your annual profit against the actual cash you had to put into the deal, not the entire property value. Your "cash in" includes your deposit, stamp duty, solicitor's fees, and any money spent on refurbishment.

Imagine two properties, both generating £5,000 in annual profit. Property A required £50,000 of your cash, giving you a 10% ROI. Property B, however, only needed £25,000 of your cash to get it up and running, resulting in a much stronger 20% ROI. ROI reveals the true efficiency of your capital.

Cash Flow is King

Finally, we arrive at the lifeblood of your portfolio: monthly cash flow. This is the actual money left in your bank account each month after every single bill has been paid.

Cash Flow = Total Monthly Rent - (Mortgage Payment + Insurance + Voids Allowance + Maintenance Fund + Management Fees + Other Costs)

A property can have a fantastic-looking yield but still have negative cash flow, making it a liability, not an asset. It drains your personal finances every single month. Your goal, especially as a new investor, is to find assets that generate positive cash flow from day one. That cash flow provides a financial buffer and gives you the funds to reinvest and grow.

Let's see this in action.

Property A vs Property B Scenario

Both properties are purchased for £200,000 and rent for £1,000 per month (£12,000 per year). On the surface, they look identical.

| Metric | Property A (Modern Flat) | Property B (Older House) |

|---|---|---|

| Gross Yield | 6.0% | 6.0% |

| Monthly Mortgage | £600 | £600 |

| Monthly Insurance | £20 | £25 |

| Monthly Management (10%) | £100 | £100 |

| Monthly Maintenance | £50 (lower) | £150 (higher) |

| Total Monthly Costs | £770 | £875 |

| Monthly Cash Flow | +£230 | +£125 |

Even with the same purchase price and rent, Property A's lower maintenance costs result in nearly double the monthly cash flow. This simple example proves why you must look beyond the sticker price and gross yield to find a genuinely profitable deal.

For a deeper dive into these calculations, you can learn more about what rental yield is and how to calculate it in our complete guide.

Getting to Grips with UK Property Taxes and Finance

Let's be blunt: making money in property is one thing, but keeping it is another entirely. If you're serious about investing in property for beginners, you have to get your head around the UK's unique financial landscape. It's a non-negotiable.

Getting the tax and mortgage details right from day one is what separates sustainable portfolios from expensive cautionary tales. Overlooking a tax rule or misjudging what a lender wants are the classic mistakes that can sink an otherwise brilliant deal. This is the stuff you need to nail down before you even think about making an offer.

The Key UK Property Taxes You Can't Ignore

As a UK property investor, you'll run into a few specific taxes straight away. The first one you'll meet is Stamp Duty Land Tax (SDLT), a tiered tax you pay when you buy a property. The critical point for investors is the 3% surcharge that gets added on top of the standard rates for any second home or buy-to-let. This can easily add thousands to your upfront costs.

The biggest game-changer for individual landlords in recent years was the introduction of Section 24. This rule stops you from deducting your full mortgage interest costs from your rental income before working out your tax bill. Instead, you now just get a basic rate tax credit of 20%, which is a massive blow for higher-rate taxpayers.

This one piece of legislation has completely rewritten the playbook for many investors. To get a proper handle on how SDLT is calculated, you should check out our guide on Stamp Duty Land Tax.

Personal Name vs. a Limited Company: The Big Decision

Thanks to Section 24, one of the first major decisions you'll face is whether to buy property in your personal name or through a limited company (often called a Special Purpose Vehicle, or SPV).

- Personal Ownership: It's simpler to set up and you might find more mortgage options to start with. The catch? Your profits are taxed as personal income at your marginal rate (20%, 40%, or 45%). And if you're a higher-rate taxpayer, Section 24 will seriously limit your ability to offset mortgage costs.

- Limited Company Ownership: This structure lets you deduct all your allowable expenses, including every penny of mortgage interest, before tax is calculated. The company then pays Corporation Tax (currently 25%) on its profits. For higher earners or anyone planning to build a proper portfolio, this is often a much more tax-efficient way to operate.

Yes, running a limited company means a bit more admin, like filing annual accounts, but for serious investors, the tax advantages are often too compelling to ignore.

Securing the Right Finance

Getting a mortgage for an investment property is a different beast to borrowing for your own home. Lenders have specific buy-to-let (BTL) mortgages, and the criteria are much stricter.

First off, the deposit is bigger. While you might get a residential mortgage with a 5-10% deposit, BTL lenders will almost always demand at least 25% of the property's value. On a £200,000 property, that means you'll need a chunky £50,000 in cash for the deposit alone, before fees and stamp duty.

Second, they assess affordability differently. Lenders aren't just looking at your salary; they're focused on the property's rental income. As a rule of thumb, they'll want the monthly rent to be at least 125% to 145% of the monthly mortgage payment, which they calculate using a higher "stress test" interest rate. This gives them a safety buffer to ensure the property can still cover its costs if interest rates climb.

The UK rental market is forecast to grow from £95 billion in 2024 to over £130 billion by 2030, with over 7 million households renting. With predictions of a potential 22% cumulative house price rise by 2030, the opportunity is huge. But you can only capitalise on this growth if you understand the tax and finance rules inside out.

A Step-By-Step Guide to Your First Purchase

Right, this is where the theory ends and the real work begins. Moving from an aspiring investor to a property owner can feel like a massive leap, but breaking it down into a clear, manageable checklist strips away the overwhelm. Think of this as your roadmap, designed to guide you confidently through every stage of your first deal.

When you're investing in property for beginners, following a structured process is everything. It stops you from making costly emotional decisions and ensures you've ticked every single box. The journey from finding a deal to picking up the keys is a well-trodden path—let's walk it together.

Stage 1: Define Your Goals and Research Locations

Before you even think about scrolling through property listings, you need to know exactly what you're trying to achieve. Are you hunting for a solid monthly cash flow of £300+, or are you more focused on long-term capital growth in an up-and-coming area? Your answer here will dictate your entire search.

Once your goals are crystal clear, it's time for a deep dive into location research. You're looking for areas with strong "fundamentals":

- Strong Tenant Demand: Look for major employers, universities, hospitals, and good transport links. Where are people consistently looking to live?

- Potential for Growth: Are there any big regeneration projects or new infrastructure developments on the horizon? These are often signs of future value.

- Affordability: Does the area offer properties within your budget that can still generate a healthy return on your investment?

Stage 2: Sourcing and Analysing Deals

With your target locations nailed down, it's time to actually find potential deals. This is about more than just scrolling through Rightmove. Start building relationships with local estate agents; let them know you're a serious, finance-ready buyer. A good agent will often call you before a property even hits the open market.

As deals start landing in your inbox, you need to analyse them quickly but accurately. This is where your understanding of those key financial metrics becomes critical. A great starting point is to set your "must-have" numbers. For instance, you might decide you won't even look at a deal with a gross yield below 6% or a projected ROI of less than 15%.

Using a tool like DealSheet AI can seriously speed this up, letting you analyse a dozen properties in the time it would take to do just one manually. For a detailed walkthrough on this, check out our complete guide to analysing UK buy-to-let deals for 2026.

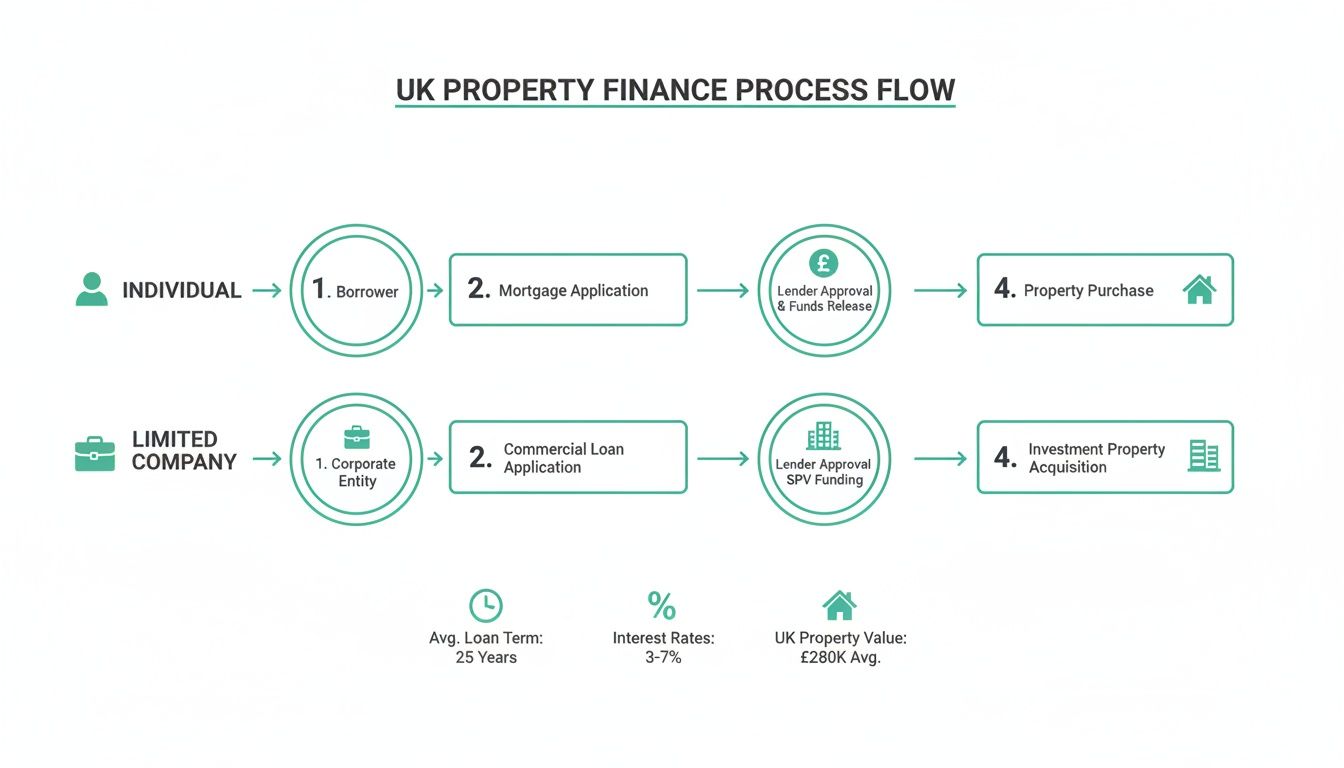

This flowchart gives a great overview of the typical financing process, whether you're buying personally or through a limited company.

As you can see, while the core steps are similar, the legal and tax considerations diverge quite a bit, which reinforces why choosing the right ownership structure from day one is so important.

Stage 3: Due Diligence and Making an Offer

Once a property's initial numbers stack up, it's time to dig deeper with due diligence. This kicks off with a viewing. Your job is to look beyond the fresh coat of paint and the nice staging.

Pro Tip: During a viewing, check for tell-tale signs of damp (musty smells, peeling wallpaper), look at the condition of the roof from the street, test the water pressure in the taps, and check the age of the boiler. These are the expensive fixes that will never appear on a standard listing.

If everything looks solid, you're ready to make an offer. Your offer should be based on your detailed analysis and what similar properties have actually sold for recently, not just the asking price. Be prepared to negotiate, but never, ever go above the maximum price your numbers can support.

Stage 4: Navigating the Legal Process

Once your offer is accepted, the legal machine grinds into action. You'll need a solicitor to handle the conveyancing—the legal transfer of property ownership. They will carry out local searches, review the contract, and raise any questions with the seller's solicitor.

At the same time, you'll be finalising your mortgage application. Your lender will conduct their own valuation survey to make sure the property is worth what you're paying for it. It's also a very good idea to commission your own independent survey, like a RICS HomeBuyer Report, to uncover any potential structural issues the lender's basic valuation might miss.

Finally, on completion day, the funds are transferred, the contracts are exchanged, and you officially become the owner of your first investment property. By following this step-by-step approach, you turn a complex procedure into a series of achievable tasks, moving you from beginner to landlord.

Using Technology to Invest Smarter, Not Harder

Back in the day, property investors got by with clunky spreadsheets, local knowledge, and a healthy dose of gut feeling. While experience and instinct still matter, today's sharpest investors use technology to make faster, more accurate decisions. This is a massive advantage when you're just starting out with investing in property for beginners in the UK.

Modern tools cut out the tedious manual work, letting you analyse dozens of potential deals in the time it once took to check just one. Speed is your competitive edge here. It stops you from missing out on a great opportunity just because you were bogged down in calculations. The goal is simple: spend less time number-crunching and more time finding genuinely profitable assets.

How AI Has Changed Deal Analysis

The days of manually building a financial model for every single property listing are thankfully over. Modern apps have completely changed the game by automating the most soul-destroying parts of the analysis process.

Imagine finding a promising property on Rightmove. Instead of firing up a blank spreadsheet, you can now just copy the listing's URL and paste it straight into an app like DealSheet AI. Within seconds, it builds a complete financial model for you.

- Automatic Data Extraction: The AI pulls the asking price, address, and other key details directly from the listing.

- UK-Specific Tax Calculations: Crucially, it automatically factors in UK-specific rules like Stamp Duty Land Tax (SDLT) and the painful impact of Section 24 on your mortgage interest.

- Instant Financial Metrics: It instantly calculates your projected Gross Yield, Return on Investment (ROI), and monthly cash flow.

This screenshot from the DealSheet AI app shows a clear, side-by-side comparison of two different investment properties.

The key insight here is how quickly you can see which property offers a better ROI and higher monthly cash flow, allowing for an immediate, data-driven decision.

From Analysis to Action

Beyond that first look, technology helps you manage and grow your portfolio more effectively. You can stress-test your numbers against potential interest rate rises, seeing exactly how a 0.5% or 1% increase would hit your monthly profits. That kind of foresight is invaluable for managing risk.

Modern investment tools aren't just about speed; they're about confidence. They give you a consistent, reliable framework for every deal, replacing fragile spreadsheets with professional, data-backed outputs.

When you're ready to get financing, these tools can generate professional, one-page PDF reports that clearly present your deal's viability to a mortgage broker or investment partner. By adopting this tech-first approach, you move from second-guessing your numbers to making confident, well-informed investment decisions right from your very first deal.

A Few Final Questions for New Investors

Getting started in UK property always throws up a few common questions. This final section tackles the ones that come up time and time again, giving you some straight answers to help you get going with a bit more confidence.

How Much Money Do I Actually Need to Start?

There's no magic number here, but a realistic starting point for your first deal in the UK is somewhere between £40,000 and £55,000.

Where does that figure come from? It's what you'd typically need to cover the upfront costs for a decent property in one of the more affordable, high-yielding cities. It usually breaks down into:

- A 25% deposit on a property in the £150,000-£200,000 range.

- The 3% Stamp Duty Land Tax (SDLT) surcharge that applies to second homes.

- Solicitor fees, survey costs, and a small pot of money for unexpected snags.

And remember, this is separate from your personal finances. Lenders will also want to see that you have a stable income, usually over £25,000 a year, before they'll even consider your application.

Should I Buy in My Personal Name or a Limited Company?

This is a massive decision, and it pretty much all comes down to tax.

Buying in your personal name is simpler to get started. The admin is easier. But your profits get taxed as personal income at your marginal rate (20%, 40%, or 45%). Thanks to the Section 24 tax changes, if you're a higher-rate taxpayer, you can no longer deduct your full mortgage interest costs, which can absolutely hammer your profitability.

A limited company structure lets you deduct all allowable business expenses—including the full whack of your mortgage interest—before you pay any tax. The company's profits are then hit with Corporation Tax. For higher earners or anyone serious about building a proper portfolio, this is almost always the more efficient way to go.

What Is a Good Rental Yield for a Beginner?

What's considered a "good" rental yield really depends on where you're buying. In London and the South East, where property prices are sky-high, a gross yield of 3-4% is pretty standard.

But for a beginner who wants to see positive cash flow from day one, you should be aiming much higher. A gross yield of 6% or more is a far better target. Plenty of investors are hitting 7-9% by focusing on cities in the North of England, the Midlands, and Scotland, where the balance between property prices and rental demand is much sweeter.

Just remember to always calculate your net yield. That's the number that tells you the real return after all your costs are paid.

Ready to stop guessing and start analysing deals with real confidence? The DealSheet AI app helps UK investors analyse any property in seconds, factoring in all the key metrics and UK-specific taxes we've talked about.

Analyse your first deal for free and see how quickly you can make data-driven decisions. Download the app today from the Apple App Store.