A Practical Guide to Property Flipping UK for Maximum Profit in 2026

A Practical Guide to Property Flipping UK for Maximum Profit in 2026

Successful property flipping UK ventures in 2026 hinge on a data-driven strategy, not just a keen eye for a bargain. To maximise profit, you must accurately calculate costs, secure the right finance, and manage renovations efficiently, focusing on regions like the North of England where lower entry costs provide better margins. This guide provides the actionable insights you need to navigate the modern market, from sourcing deals to securing a profitable exit. For precise financial modelling, the DealSheet AI app is an essential tool, allowing you to analyse any UK property flip in seconds directly from your phone.

Understanding the Modern UK Flipping Market

The world of property flipping UK investors is always shifting, constantly reshaped by the economy, tax changes, and what buyers are looking for. The core idea—buy low, add value, sell high—is timeless. But the journey to a decent profit is a lot tougher and needs a far more analytical approach than it did a few years back.

In 2026, your success lives or dies on your ability to master the numbers before you even think about making an offer. The days of relying on gut feelings are long gone.

A Market of Tighter Margins

The post-financial crisis years were a boom time for flipping, but the last few years have brought some serious headwinds. Soaring costs, especially for finance and materials, have squeezed profits hard, making precise calculations absolutely essential.

The data tells a clear story. The number of homes flipped in the UK hit a peak in 2022 at 26,340—the highest it had been since 2007. Fast forward to 2023, and that number plummeted to an estimated 16,600, the lowest in a decade. Why the dramatic drop? Soaring costs are the main culprit. Stamp Duty, for example, has rocketed by 236% over ten years, effectively halving average gross profits.

By early 2025, the reality was that only 66% of flips were profitable after accounting for stamp duty alone. This really hammers home the need for meticulous financial modelling. You can dive into the numbers yourself with the full research on the decline of flipping from Hamptons.

For today's flipper, profit is no longer found in a rising market—it's created through meticulous planning, disciplined budgeting, and a deep understanding of local supply and demand. Every pound must be accounted for from day one.

The Modern UK Property Flip Checklist

To navigate this tougher environment, you need a system. A modern property flip isn't a speculative punt; it's a well-managed project with clear, distinct phases. This table breaks down the critical stages you need to master to give yourself the best chance of success.

| Stage | Key Focus | Critical Action |

|---|---|---|

| Sourcing & Analysis | Finding undervalued assets and verifying profitability. | Use data tools to run numbers on multiple deals quickly, filtering out non-starters. |

| Finance & Acquisition | Securing fast, flexible funding. | Line up bridging or auction finance before making an offer to ensure you can move decisively. |

| Renovation | Adding maximum value within a strict budget and timeline. | Create a detailed scope of works and prioritise cosmetic upgrades with high ROI. |

| Exit Strategy | Selling quickly for the highest possible price. | Price realistically based on local comparables and stage the property effectively. |

By breaking the process down like this, you can spot and manage risks at every turn. It transforms a complex, daunting task into a manageable—and profitable—venture. The rest of this guide will give you a detailed blueprint for executing each of these stages properly.

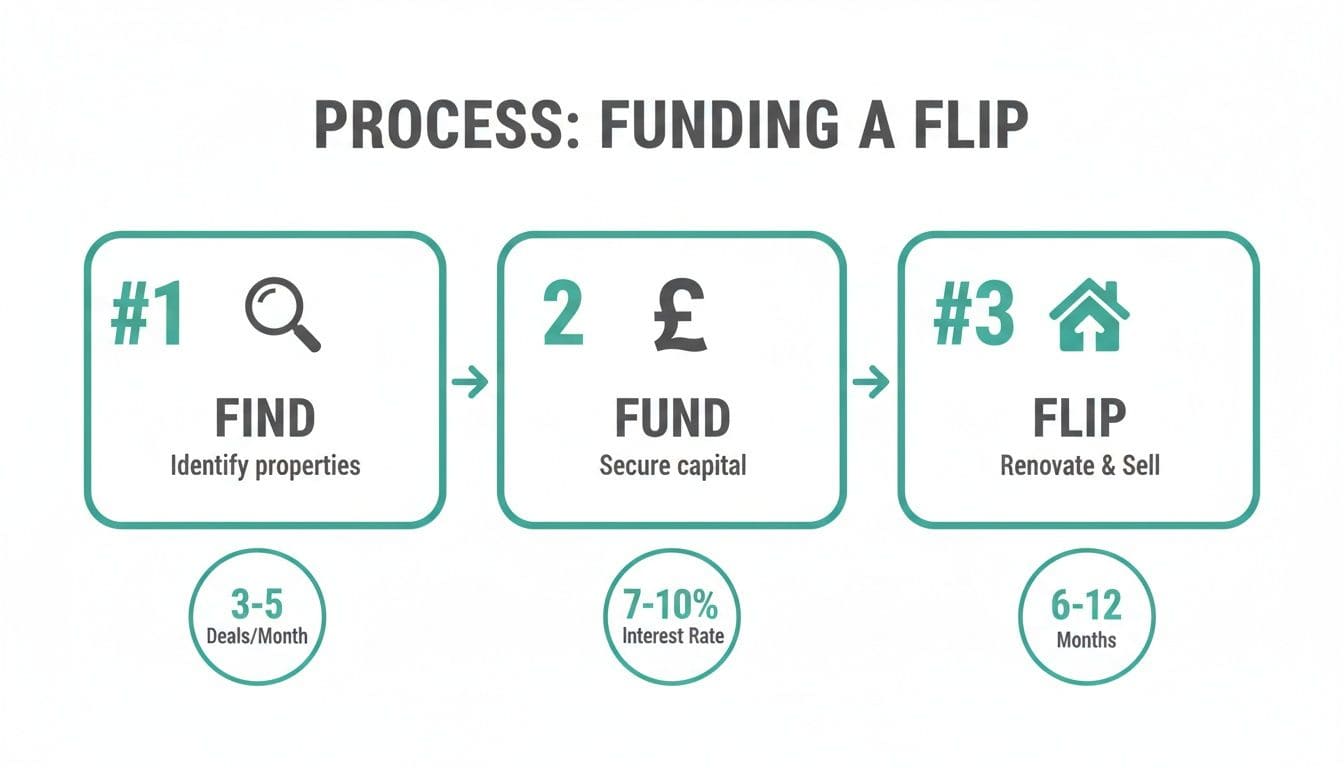

How to Find and Fund Your Next Flip

Every successful property flip starts with the same two ingredients: finding the right property and securing it at the right price. This means you have to dig deeper than the mainstream portals like Rightmove, where the real bargains are few and far between and the competition is absolutely ferocious.

Once you've got a potential deal in your sights, the next hurdle is always funding. The speed you need to move at means a traditional high-street mortgage is almost always a non-starter. They're just too slow. Getting your head around the specialist finance products designed for flipping is what lets you move quickly and with confidence.

Modern Sourcing Strategies for UK Flippers

Finding a property with genuine potential for a profitable uplift demands a proactive approach. Just scrolling through Zoopla is a recipe for overpaying or finding scraps everyone else has already passed on. Instead, you need to be looking in more fruitful places.

- Property Auctions: Auctions are the classic hunting ground for flips. You'll often find properties that are completely unmortgageable because they've been stripped out (no kitchen or bathroom, for example). This locks out typical homebuyers and opens the door for cash buyers or those with bridging finance lined up.

- Estate Agent Relationships: Don't just be another name on a mailing list; build real relationships. Let the local agents know you're a serious, chain-free buyer actively looking for renovation projects. Specifically ask about probate sales or properties that have been lingering on the market for months—these sellers are often the most motivated.

- Direct-to-Vendor Marketing: This is where you reach out to homeowners directly, maybe with a targeted leaflet drop in an area you know well. It's more legwork, for sure, but it can unearth completely off-market deals where you have zero competition.

Here's a quick rundown of what to expect from each method:

| Sourcing Method | Pros | Cons |

|---|---|---|

| Auctions | Speed, transparency, potential for deep discounts. | High pressure, requires immediate financing and deposit. |

| Estate Agents | Access to probate and motivated sellers. | Can be competitive if you're not a preferred buyer. |

| Direct-to-Vendor | No competition, potential for excellent deals. | Time-consuming, lower response rate. |

The best property flippers don't wait for deals to land in their lap; they build a system to find them. By combining these methods, you create a consistent pipeline of opportunities, which is the absolute lifeblood of any serious flipping business in the UK.

Securing the Right Finance

Once you've sourced a deal, your ability to fund it quickly is what separates you from the rest of the pack. As I mentioned, traditional residential mortgages are rarely an option due to the property's condition or the sheer speed required. For property flipping UK investors, specialist finance isn't a "nice to have"—it's essential.

The most common and effective tool in the box is a bridging loan. This is short-term finance, typically lasting anywhere from a few months up to two years. It's designed to 'bridge' the gap between buying a property and your exit, whether that's selling it on or refinancing.

Here's what the flip template in the DealSheet AI app looks like. It lets you model finance options like bridging loans in seconds.

You can plug in your numbers for the purchase, finance, and resale value to get an instant picture of the deal's profitability.

Bridging lenders really only care about two things: the property's value (both now and what it'll be worth after the refurb) and your exit strategy. They need to be completely confident that you can repay the loan, either by selling the property or refinancing onto a different mortgage product.

Key Funding Options Explained

Beyond a standard bridging loan, there are a few other routes to consider. Each has its place, depending on the specifics of the deal.

- Bridging Loans: This is the go-to for most flips. Lenders can typically offer up to 75% Loan-to-Value (LTV) and can get funds released in days, not months. Crucially, the interest is often 'rolled up' and paid at the end of the term, which protects your cash flow while you're deep in the renovation.

- Auction Finance: Think of this as a specialised bridging loan built for the tight 28-day completion deadlines of an auction. It's absolutely vital to have this pre-approved before you even think about raising your hand in the auction room.

- Cash Purchase: Using your own cash is, of course, the simplest and fastest way to buy, and it gives you immense negotiating power. The downside is that it ties up a huge amount of capital that you could be using across multiple projects. Often, the smartest play is to use your cash for the deposit and leverage bridging finance for the rest.

Understanding the nuances of each funding type lets you structure your deals for the best possible return while keeping a lid on your risk. For a deeper dive into finding even better opportunities, you might want to explore our guide on how professional property deal sourcing in the UK works.

Mastering the Numbers from Purchase to Profit

Successful property flippers live and die by their spreadsheets. In a market where margins are tighter than ever, a single miscalculation can be the difference between a healthy profit and a painful loss. Getting your numbers right isn't just a box-ticking exercise; it's the absolute foundation of your entire project.

This means you need to meticulously account for every single pound, from the initial purchase right through to the final sale. It's a numbers game, pure and simple. Playing it well means understanding the three core cost categories: acquisition, holding, and disposal.

Thankfully, you don't have to build fragile, error-prone spreadsheets from scratch. Tools like the DealSheet AI app are designed for this exact purpose. You can paste a property URL and instantly build a complete financial model, factoring in all UK-specific taxes and costs to get an immediate view of your potential return.

Deconstructing Your Purchase and Renovation Costs

The most obvious costs are the ones you face upfront. These are the "big three" expenses that will form the bulk of your initial outlay.

- Purchase Price: This is the headline figure, but the price you agree is only the beginning.

- Stamp Duty Land Tax (SDLT): An unavoidable and significant tax in England and Northern Ireland. As an investor buying an additional property, you'll be paying the higher rates, which can easily add thousands, if not tens of thousands, to your bill.

- Renovation Budget: This is the biggest variable and the easiest place to get things wrong. A light cosmetic update (think new paint, flooring, and modernising a kitchen) might cost £15,000 - £25,000 for a typical terraced house. A more substantial back-to-brick refurbishment, however, could easily sail past £50,000 - £70,000.

Getting the renovation budget right is critical. You absolutely must get quotes from trusted tradespeople before you commit to the purchase, not after.

A classic rookie mistake is underestimating the renovation spend. Always, always add a contingency fund of at least 10-15% to your calculated budget. This buffer is your safety net for the inevitable surprises, like discovering hidden damp or realising the property needs a full rewire.

The journey looks simple on paper, but robust financial management underpins every single step.

The Hidden Drain of Holding Costs

The moment you own the property, the clock starts ticking. Loudly. Every single day you hold the asset, it's costing you money. These "holding costs" are often underestimated by new flippers, but they steadily and silently erode your profit margin.

These costs include:

- Finance Costs: If you've used a bridging loan, this will be your largest holding cost by a country mile. The interest is calculated daily and can be substantial.

- Insurance: You'll need specialist renovation or unoccupied property insurance, which is considerably more expensive than a standard policy.

- Utilities: Even an empty property needs electricity and water for the trades, and you'll be paying standing charges regardless.

- Council Tax: Unless the property is genuinely derelict and has been removed from the council tax register (which is rare), you will be liable for the full bill.

The impact of holding costs is precisely why speed is everything in property flipping UK. It's no surprise that over 21% of successful flips are held for just two to three months. The goal is to minimise this financial drain.

Calculating Your Exit Costs Accurately

Finally, once the renovation is complete and you've found a buyer, there's one last set of costs to account for before you can calculate your true net profit. Don't fall at the final hurdle.

Selling costs typically include:

- Estate Agent Fees: Usually somewhere between 1% to 1.5% (+VAT) of the final sale price.

- Legal Fees (Conveyancing): Budget for around £1,000 - £2,000 for a solicitor to handle the sale.

- Capital Gains Tax (CGT): Any profit you make is potentially liable for CGT. The rate for residential property is either 18% or 24% (as of 2026), depending on your income tax band. This can take a huge bite out of your returns.

The profitability picture in UK flipping is more nuanced than many realise. Data from Q1 2025 showed that while over 80% of flips sold for a gross profit, only 66% were still in the black after stamp duty was paid. That number shrinks again once all renovation and holding costs are factored in.

Flats and terraced houses remain the most popular targets for a reason, making up 44.86% and 32.27% of flips respectively. They offer a sweet spot of purchase price and potential uplift.

Where to Find the Best Flips in the UK Right Now

Location has always been the golden rule in property, but for anyone flipping houses in the UK today, understanding the regional shifts is more critical than ever. For years, the smart money was funnelled into London and the South East, but that landscape has completely changed. Now, the real profits are being made in areas where lower purchase prices and solid local demand offer far healthier margins.

The data is clear: flipping activity is migrating north. We're seeing a sustained move into the North of England, the Midlands, and Wales, where the numbers simply make more sense. In many of these regions, you can still buy a property, complete a full refurb, and keep your total project costs low enough to minimise the stamp duty hit—a feat that's become almost impossible in the capital.

The Great Migration North

The trend is undeniable. For a long time, investors accepted razor-thin margins in London, banking on rapid house price inflation to do all the heavy lifting for them. That game is over. Today, a massive Stamp Duty Land Tax bill in a high-value area can swallow your entire profit before you've even paid the builders.

This has forced a major strategic rethink. Flippers are now targeting regions where the entry costs are lower and the potential to add value through renovation is much higher. This isn't just about finding a cheaper house; it's about finding markets where local wages and buyer demand can comfortably support the post-refurb values you need to hit.

A few key things are driving this shift:

- Affordability: Lower purchase prices dramatically reduce your initial cash outlay and, just as importantly, your SDLT bill.

- A Solid Plan B: While not the primary goal for a flip, the strong rental yields in these areas give you a viable exit if a quick sale doesn't happen. You can pivot to other property investment strategies in the UK if the market turns.

- Value-Add Opportunities: Many northern towns have an abundance of older housing stock that's perfect for a modern facelift, letting you manufacture significant value through the renovation itself.

UK Property Flipping Regional Hotspots (2025 Data)

To pinpoint exactly where the action is, we've analysed the latest flipping data. The table below breaks down the key metrics, showing a clear pattern of opportunity away from the traditional southern powerhouses.

| Region | Flip Rate (% of Sales) | Average Gross Profit | Key Driver |

|---|---|---|---|

| North East | 4.7% | £35,000 | High affordability, low SDLT impact |

| Wales | 3.9% | £42,000 | Strong demand for modernised family homes |

| Midlands | 3.5% | £48,000 | Regeneration projects, strong transport links |

| North West | 3.2% | £45,000 | Diverse city economies (Manchester, Liverpool) |

| London | 1.5% | £85,000 | High costs, huge SDLT bills eroding profits |

The data paints a stark picture: while London still offers the highest average gross profit on paper, the sheer volume of activity and the rate of successful flips are overwhelmingly concentrated in the North, Midlands, and Wales. The lower entry costs and reduced tax burdens in these areas make them far more attractive for generating consistent returns.

Identifying the Current Hotspots

So, where are the most promising postcodes right now? All the recent data points overwhelmingly to one area in particular.

The North East of England has cemented itself as the UK's flipping hotspot. In the first quarter of 2025, an incredible 4.7% of all homes sold in the region were flips—that's more than double the 2.3% average for England and Wales. This is driven by extremely affordable properties, many of which are stamp duty-exempt even for investors.

It's a world away from London, where flips have slumped to just 1.5% of sales and the average SDLT bill is a staggering £33,000. The trend is crystal clear: in 2025, 61% of all flipped properties were in the Midlands, the North, or Wales. That's a huge jump from just 50% a decade ago. If you want to dive deeper, you can learn more about these findings on investor margins to see the full picture.

For the modern flipper, the game is no longer about chasing capital growth in overheated markets. It's about manufacturing your own profit through smart acquisition and renovation in regions where the fundamental economics actually stack up.

Tailoring Your Strategy to Local Dynamics

Of course, success in these new hotspots requires more than just showing up with a budget. You need to do your homework and get to grips with the local market dynamics. A strategy that crushes it in a Welsh coastal town won't necessarily work in an industrial hub in the Midlands.

Before you even think about putting an offer in, your research needs to cover:

- Local Employment: Who are the major employers? A diverse and stable job market is what underpins local house prices and buyer confidence.

- Transport Links: Regeneration often follows infrastructure. Look for areas with new or improved train lines, roads, or public transport connections.

- Local Comparables: This is non-negotiable. You need to analyse what actually sells, not what agents are listing properties for. Dig into the Land Registry data for sold prices of recently renovated homes.

This is the kind of detailed, on-the-ground research that separates amateur speculators from professional investors. It allows you to tailor your refurbishment plans to meet what local buyers actually want and, crucially, to price your finished project accurately for a swift, profitable sale.

Managing the Renovation and Planning Your Exit

You've got the keys and the finance is in place. Now for the bit where the real value is made. The renovation is where you drag a tired, unloved property into the modern market, but it's also the stage where budgets blow out and timelines stretch into profit-eating territory.

Good management is everything here. You need a detailed plan before a single hammer swings and you need to keep a tight grip on the process from start to finish. Just as vital is having a crystal-clear exit strategy from day one, because how you plan to get out dictates many of the choices you'll make during the refurb.

Executing an Efficient and Budget-Conscious Refurbishment

The secret to a profitable refurb is simple: only spend money where it makes you money. This isn't your forever home; it's a product you're preparing for a specific market. Every pound spent must be justified by adding more to the final sale price.

Your first job is to create a detailed scope of works. This isn't just a list; it's a precise document detailing every single task, from ripping out the knackered kitchen to the final coat of satinwood on the skirting boards. This is the document you'll hand to contractors to get accurate, comparable quotes.

A vague plan gets you vague quotes and a mountain of "extras". Your scope of works needs to be so detailed that a builder knows exactly what you expect without having to guess. This discipline is what stops 'scope creep' dead in its tracks and protects your budget.

When it comes to managing contractors, regular site visits are non-negotiable. I'd recommend being on-site at least two to three times a week. This lets you check progress against your timeline, answer questions on the spot, and catch potential problems before they morph into expensive delays.

Prioritising Renovations with the Highest Return on Investment

Not all renovations are born equal. Some add serious value, while others are just money pits. For a successful property flipping uk project, you need to be ruthless, focusing your budget on the things that buyers actually care about.

- Kitchens and Bathrooms: These are the two rooms that sell houses. Full stop. A modern, clean, and functional kitchen and bathroom can be the single deciding factor for a buyer. You don't need to splash out on designer brands; smart, quality fittings from trade suppliers like Howdens or Benchmarx will give you the high-end look that buyers love.

- Kerb Appeal: First impressions are everything. Tidying the front garden, putting a fresh coat of paint on the front door, and making sure the windows are sparkling clean can add thousands to your offers for a tiny outlay. It's the easiest win in the book.

- Neutral Decor: Forget your personal taste. Your job is to create a blank canvas that appeals to the widest possible audience. Think light, neutral colours—off-whites, soft greys, that sort of thing. It makes rooms feel bigger and brighter, letting buyers imagine their own lives there.

Getting your head around refurbishment costs is absolutely critical for budgeting accurately. To get a feel for typical expenses, it's worth reviewing a detailed guide on building costs per square metre in the UK.

Crafting Your Exit Strategy: The Sale

In most cases, your exit will be a straightforward sale on the open market. The moment the dust starts to settle on the renovation, your mindset needs to switch from project manager to marketer.

Choosing the right estate agent is crucial. Don't just go with the cheapest commission. Get three local agents to value the property and ask them to back it up with hard evidence of recent, comparable sales. Go with the one who seems the most proactive, professional, and has a clear plan for marketing your specific type of property.

Staging the property for viewings can make a massive difference. At an absolute minimum, it must be spotlessly clean and completely free of clutter. If you've got room in the budget, professional staging with hired furniture can help buyers connect emotionally with the space, often leading to quicker sales and better offers.

An Alternative Exit: The BRRRR Model

While a quick sale is the classic flipping exit, it's not your only move. An increasingly popular alternative is the 'Buy, Refurbish, Refinance, Rent' (BRRRR) model. This is less of a flip and more of a long-term strategy for investors who want to build a portfolio, not just take a one-off profit.

Here's the breakdown:

- Buy: You acquire an undervalued property, often using cash or a bridging loan.

- Refurbish: You renovate it to a high standard, forcing the value up significantly.

- Refinance: Once the work is complete, a surveyor provides a new commercial valuation. You then refinance onto a standard buy-to-let mortgage based on this much higher value.

- Rent: You let the property out, and the rental income covers the new mortgage payments and other running costs.

The magic of the refinance is to pull out most, if not all, of your initial investment (your deposit and the refurb costs). This capital is then freed up to be recycled into your next project. It's a powerful way to build a property portfolio with a relatively small starting pot of cash, turning one successful flip into a long-term, income-producing asset.

Common Property Flipping Questions Answered

Diving into the world of property flipping UK can feel like staring at a mountain of questions. Before you put your hard-earned capital on the line, you need clear, straightforward answers. Whether this is your first project or you're a seasoned investor sharpening your strategy, let's cut through the noise.

This section tackles the questions we hear most often, from how much cash you really need to the gritty details of tax. The goal is to give you the confidence to navigate your projects without the guesswork.

How Much Money Do I Need to Start Flipping Houses in the UK?

There's no single magic number here. The starting capital is massively dependent on where in the country you're buying. But you'll always need funds to cover three key areas: the deposit, the renovation, and all the buying costs.

When using bridging finance, which is common for flips, expect to need a deposit of around 25% of the purchase price.

On top of that, you must have the cash ready for your entire renovation budget and all the associated fees—think legal costs, broker fees, and of course, Stamp Duty. In a lower-priced area like the North East, you might get a foot on the ladder with a pot of £30,000 to £50,000. Try that in the South East, and you'll need significantly more.

Is Property Flipping Still Profitable in the UK in 2026?

Yes, absolutely—but the game has changed. The days of buying a property, waiting six months, and letting a rising market do all the heavy lifting are long gone. Today, profit is manufactured through smart, disciplined work.

Success in 2026 boils down to three core principles:

- Buying at a serious discount to the property's true market value.

- Controlling your renovation costs with a ruthless budget and tight project management.

- Picking the right location where local demand will actually support your target sale price.

Right now, areas with lower house prices, like many parts of the North of England and the Midlands, offer far more breathing room for healthy profit margins compared to the overheated South.

What Is the 70 Percent Rule in House Flipping?

The 70% rule is a classic, back-of-the-envelope calculation used to quickly judge the maximum price you should offer on a potential flip. It's a guideline, not gospel, but it's incredibly useful for filtering deals quickly.

The formula says you should pay no more than 70% of the property's After Repair Value (ARV), minus the total estimated cost of the renovation.

Example: A property has a potential ARV of £200,000 and you reckon it needs £30,000 in repairs. The calculation is: (£200,000 x 0.70) - £30,000 = £110,000. According to the rule, £110,000 is the absolute maximum you should offer.

This rule is designed to build a solid buffer into your deal, covering your holding costs, selling fees, financing costs, and, crucially, your profit.

How Do I Avoid Paying Capital Gains Tax on a Flipped Property?

The main way you might avoid Capital Gains Tax (CGT) is by qualifying for Private Residence Relief (PRR). This tax relief is available if you have genuinely lived in the property as your main and only home for the entire time you've owned it.

But be warned: HMRC looks at these cases very, very closely.

If they suspect your main reason for buying and renovating the property was to make a profit—not to create a home for yourself—they will deny the relief. Any gain you make will then be subject to CGT.

Ready to analyse your next flip with speed and confidence? DealSheet AI replaces guesswork with data-driven insights. Download the app and start your free trial today to analyse UK property deals in seconds.