A UK Guide for Property Investment Beginners in 2026

A UK Guide for Property Investment Beginners in 2026

For property investment beginners in the UK, the path to success in 2026 is clear: acquire assets that generate monthly income while growing in value. This is achieved by mastering core investment strategies and leveraging modern tools to analyse deals efficiently. Instead of battling with complex spreadsheets, savvy investors now use tools like the DealSheet AI app, which can analyse a potential UK investment in seconds from just a property link, empowering you to make confident, data-driven decisions. Download the app here and start your free trial.

Your Starting Point for UK Property Investment

Stepping into the world of UK property investment can feel like learning a new language. But at its heart, the principle is incredibly straightforward. You are buying a real, tangible asset to do two jobs: generate a steady income from rent and, hopefully, increase in value over the long term. This powerful combination of cashflow and capital appreciation is why property remains a cornerstone of wealth creation for so many.

For property investment beginners, the first and most crucial step is to build a solid base of knowledge before you even think about putting down a deposit. This means getting comfortable with the language of deals, understanding the different ways to invest, and figuring out how to finance your first purchase. Think of this guide as your roadmap, designed to demystify these concepts and give you a clear, actionable plan.

Why Property Remains a Strong Choice

Despite what you might hear about market ups and downs, UK property consistently proves its resilience and potential for solid returns. Take the 12 months leading up to February 2025, for example, where the overall UK real estate market delivered an 8.1% total return. That figure, which combines both rental income and capital growth, is a stark reminder of why property is such an attractive asset class, especially when compared to more volatile options.

It's this blend of stability and growth potential that makes it such an excellent vehicle for hitting long-term financial goals.

The core challenge for a new investor isn't finding a property; it's learning how to recognise a good deal. This requires understanding the numbers behind the listing price, from rental yield to ongoing costs and tax implications.

Building Your Foundational Knowledge

To win at this game, you have to learn the rules first. Before you start scrolling through Rightmove, it's essential to get a firm grip on the core concepts that separate a successful investment from an expensive mistake.

This means you need to get your head around:

- Understanding Key Metrics: Terms like Yield, ROI (Return on Investment), and Cashflow are the vital signs of any property deal. You have to know what they mean and how to calculate them.

- Choosing a Strategy: Will you go for a simple Buy-to-Let, or something more hands-on like a property flip? Your personal goals, budget, and appetite for risk will point you down the right path.

- Navigating UK-Specific Rules: Regulations like Stamp Duty Land Tax (SDLT) and the infamous Section 24 mortgage interest relief rules will directly hit your bottom line. They must be factored into every single calculation.

To dive deeper into any of these topics, the guides on the DealSheet AI blog are a great place to start. For now, this guide will walk you through each of these areas, giving you the foundational knowledge you need to get moving.

Understanding the Language of Property Deals

Before you can spot a good deal, you need to speak the language. For any property investment beginner in the UK, getting this right is the difference between making money and losing it. The single biggest mental shift is to stop thinking of a property as a home and start treating it like a small business.

The rent you collect is your revenue. Your mortgage, maintenance, agent fees, and insurance are your expenses. What's left in your bank account each month is your cash flow – and that's the ultimate measure of a successful rental.

Gross Yield vs Net Yield

You'll see properties advertised everywhere with a "gross yield". This is just the annual rent divided by the purchase price. It's a quick, back-of-the-envelope number, but honestly, it's mostly a vanity metric. It can be dangerously misleading.

Gross yield ignores every single real-world cost of owning that property. A far more honest and useful figure is the net yield. This calculation forces you to factor in all your operating expenses, giving you a true picture of how hard your money is actually working.

Key Takeaway: Always, always focus on the net yield. It makes you account for every cost, from the mortgage interest right down to the small repairs, preventing nasty surprises later on.

Getting your yield calculations right is a foundational skill. For a proper breakdown of the numbers, you can learn more about how to calculate rental yield in the UK in our dedicated guide. It's essential for analysing deals with the precision you'll need in 2026.

The Two Pillars of Property Wealth

Your returns from property investment really stand on two pillars. It's crucial to understand how they work together.

- Capital Appreciation: This is simply the increase in the property's market value over time. While it's never guaranteed, UK property has historically been a strong long-term asset for growth. Think of this as your long-term wealth builder.

- Rental Income (Cash Flow): This is the monthly profit you make after every single bill is paid. This is what keeps the lights on, covers any unexpected costs, and provides you with a passive income stream right now.

A truly great investment delivers on both. It provides positive cash flow month after month while its value quietly grows in the background, creating a seriously powerful wealth-building engine.

Navigating UK Tax and Regulations

Getting your head around the UK's specific rules is non-negotiable. Two of the biggest ones you have to understand from day one are Stamp Duty Land Tax (SDLT) and Section 24.

- Stamp Duty Land Tax (SDLT): This is a tax you pay when buying a property in England and Northern Ireland. For investment properties, you pay a higher rate than you would for your own home. This can add thousands of pounds to your upfront costs and must be baked into your budget from the very start.

- Section 24: Often called the "tenant tax," this rule fundamentally changed how landlords are taxed. You used to be able to deduct all of your mortgage interest from your rental income before calculating your tax bill. Now, you get a tax credit based on 20% of your interest payments instead.

This change means higher-rate taxpayers can pay dramatically more tax than before, sometimes enough to turn a profitable property into a loss-making one. It is absolutely critical to run your numbers with Section 24 in mind to see if a deal actually works for your financial situation. Getting this wrong is one of the most common and costly mistakes new investors make.

Choosing Your First Investment Strategy

Deciding on your first move in property isn't about finding the one "best" strategy. It's about finding the best strategy for you. Your finances, your long-term goals, and—crucially—how much time you can actually commit will point you in the right direction.

Think of this as your roadmap to the most common UK property investment strategies. The goal is simple: to give you enough clarity to choose the right launchpad for your own journey, whether that's a steady long-term income generator or a faster, more hands-on project.

The Classic Buy-to-Let (BTL)

This is the quintessential starting point for most new investors, and for good reason. The concept is straightforward: you buy a property and rent it out to a tenant, usually a single family or a couple. The aim is to generate positive cashflow each month after all your costs are paid, while the property's value (hopefully) grows over time.

This approach is perfect for investors looking for a relatively hands-off, long-term investment that builds wealth steadily. A single BTL won't make you rich overnight, but it's a reliable and manageable way to get started.

A Buy-to-Let is like planting an oak tree. It won't provide shade overnight, but with time and patience, it grows into a strong, valuable asset that can provide for years to come.

The UK market has strong foundations for this strategy. Projections show the residential property sector is set to climb from around £95 billion in 2024 to over £130 billion by 2030, fuelled by huge rental demand from over 7 million renting households. That signals a robust, long-term runway for BTL investors. You can explore the full UK real estate market projections here.

Houses in Multiple Occupation (HMOs)

An HMO involves renting out a single property on a room-by-room basis to multiple, unrelated tenants. Think of the classic student house or a shared home for young professionals. Because you're collecting rent from several individuals in one building, the potential cashflow is significantly higher than a standard BTL.

Of course, that higher return comes with more work. Managing an HMO means juggling multiple tenancies, dealing with higher tenant turnover, and navigating stricter regulations and licensing rules from the local council. It's a much more active form of investment, best suited for those willing to put in the extra management effort for a bigger monthly reward.

The BRRRR Method

BRRRR is an acronym that stands for Buy, Refurbish, Rent, Refinance, Repeat. It's a powerful way to scale a portfolio quickly without needing a huge pot of cash for every single purchase.

Here's the process broken down:

- Buy: You find and purchase a property that needs work, often securing it below its potential market value.

- Refurbish: You renovate the property to a high standard, forcing its value up significantly.

- Rent: You find tenants and let the property out.

- Refinance: You get a new mortgage on the property based on its new, higher valuation, allowing you to pull out some of your initial investment.

- Repeat: You use the cash you've pulled out to fund the deposit for your next project, and the cycle begins again.

The magic of BRRRR is in recycling your initial capital, allowing you to build a portfolio with a relatively small starting investment. It's a high-intensity strategy that demands a good eye for a deal, accurate budgeting, and solid project management skills.

Property Flipping

Flipping is a completely different beast. Instead of renting a property out for income, you buy it, renovate it, and sell it on quickly for a profit. This is a short-term, active strategy that's all about generating capital gains.

This path suits people with a flair for design, a strong network of tradespeople, and the ability to manage a renovation on a tight schedule and budget. The rewards can be substantial lump sums of cash, but the risks are higher too. A delayed project, an unexpected cost, or a sudden dip in the housing market can wipe out your profit margin in a heartbeat. Flipping is less about passive income and all about active project management.

To help you decide, here's a quick comparison of these popular strategies.

UK Property Investment Strategy Comparison

This table breaks down the key differences between the strategies, helping you see at a glance which one might align with your resources and goals.

| Strategy | Best For | Typical Cashflow | Effort Level |

|---|---|---|---|

| Buy-to-Let (BTL) | Beginners, long-term wealth building, relatively passive income. | Low to Moderate | Low to Medium |

| HMO | Maximising monthly cashflow from a single property. | High | High |

| BRRRR | Rapidly scaling a portfolio with a limited starting pot. | Moderate to High | Very High |

| Property Flip | Generating lump-sum profits through active renovation. | None (Profit on sale) | Very High |

Ultimately, there's no right or wrong answer. The best strategy is the one that fits your life, your finances, and your appetite for risk. For a deeper dive, check out our in-depth guide that details more UK property investment strategies and how to select the right one.

How to Finance Your First UK Property

Getting the money together for your first deal is often the biggest hurdle for new property investors in the UK. The whole process can feel a bit intimidating, but the minute you grasp the key differences between financing an investment and buying your own home, you're halfway there. It all starts with the Buy-to-Let (BTL) mortgage.

A BTL mortgage is a specialist loan designed purely for landlords. Unlike the residential mortgage you might have on your own home, lenders will scrutinise the property's potential rental income just as closely as they look at your personal finances. They need to be absolutely sure the rent will comfortably cover the mortgage payments, which means the lending criteria are quite different.

Understanding Buy-to-Let Mortgages

The first major difference you'll hit is the deposit. While you might buy your own home with a 5% or 10% deposit, for a BTL mortgage, lenders will typically demand a minimum of 25% of the property's value. This is known as the Loan-to-Value (LTV) ratio. So, for a £200,000 property, you'd need to find a £50,000 deposit.

Lenders also have much stricter affordability checks, and they use a specific tool called an Interest Coverage Ratio (ICR). This calculation is their way of making sure the expected rental income is significantly higher than the mortgage payment—usually by around 125% to 145%. This creates a vital buffer to cover any void periods or unexpected repair bills.

Key Takeaway: Lenders aren't just lending to you; they are investing in the property's business potential. Your application has to prove that the asset itself is a sound, profitable venture that can easily support its own financing costs.

Putting together a strong application really just means having your financial house in order. Lenders will want to see:

- A solid credit history.

- Proof of a stable personal income (often a minimum of £25,000 per year, completely separate from any rental income).

- A detailed budget for the purchase, including funds for Stamp Duty, legal fees, and a contingency fund. To learn more, check out our guide on what Stamp Duty Land Tax is and how it works.

Exploring Alternative Financing Tools

While BTL mortgages are the most common route, they aren't your only option. Sometimes, a deal needs a more specialised or short-term funding solution to get it over the line, especially for properties that aren't in a rentable condition from day one.

One of the most powerful tools in an investor's kit is the bridging loan. This is a short-term loan, typically lasting up to 12 months, designed to "bridge" a financial gap. It's perfect for situations where a standard mortgage just won't work.

Think about these scenarios where a bridging loan is invaluable:

- Auction Purchases: Auctions demand you complete the purchase in a ridiculously tight timeframe, usually just 28 days. A bridging loan can provide the necessary capital almost instantly.

- Properties Needing Renovation: If a property is uninhabitable—say, it has no kitchen or bathroom—you simply can't get a standard BTL mortgage on it. A bridging loan lets you buy it, complete the renovation work, and then refinance onto a traditional BTL mortgage once the property is ready for tenants.

Sure, bridging loans come with higher interest rates and fees. But what they give you is the speed and flexibility to secure deals that many other investors have to pass on. Understanding how and when to use these alternative financing methods can give you a serious competitive edge.

How to Analyse a Property Deal in Minutes

The ability to size up a deal quickly and accurately is what separates successful investors from everyone else. For property investment beginners in the UK, this is the single most important skill you can build.

Forget about wrestling with clunky, error-prone spreadsheets. One wrong formula in those things can lead you down a path to a truly disastrous decision. In 2026, the game is all about speed and precision.

This is how you turn what feels like a complex financial exam into a simple, two-minute job. Modern tools are built to do the heavy lifting, giving you the data-backed confidence you need to make a smart offer.

From Listing to Analysis in Seconds

Imagine you're scrolling through Rightmove and a promising-looking two-bed terrace catches your eye. The old way? You'd have to start manually copying the price, guessing the rent, and plugging numbers into a spreadsheet, desperately trying to remember every single potential cost.

Today, the process is worlds apart. With an app like DealSheet AI, you just copy the property listing's URL from the portal and paste it straight in. The AI gets to work instantly, pulling all the crucial information—purchase price, address, and property type—to build a complete financial forecast from the ground up.

This approach saves an incredible amount of time. But more importantly, it strips out the risk of human error. It means every single deal you look at is analysed using the same consistent, reliable methodology.

Seeing the Numbers That Truly Matter

Once the data is in, the app automatically crunches the critical metrics that tell you if a deal is actually worth your time. You don't just see a simple gross yield; you get a full breakdown of the figures that define a profitable investment.

This includes:

- Net Yield: The true measure of profitability after all the operational costs are stripped out.

- Return on Investment (ROI): A clean percentage showing you exactly how hard your invested cash is working for you.

- Monthly Cash Flow: The pounds and pence you can expect to have left in your bank account after the mortgage and all other bills are paid.

Here's an example of what that instant analysis looks like inside the DealSheet AI app.

The screenshot gives you a clear, at-a-glance summary of a potential deal, putting vital metrics like cash flow and ROI front and centre so you can make a quick first judgement.

Stress-Testing Your Potential Investment

A good deal looks great on paper. A great deal holds up when you apply a bit of pressure. The UK property market is always moving, and you need to be ready for change. What happens if interest rates creep up by another 1%? What if the property sits empty for two months between tenants?

Figuring out these scenarios by hand is tedious and complicated. A powerful analysis tool, however, lets you "stress-test" your investment with just a few taps. You can adjust sliders for mortgage rates, void periods, and maintenance costs to see exactly how those variables hit your bottom line.

This isn't just about crunching numbers; it's about building resilience into your portfolio. Stress-testing lets you find a deal's breaking point before you've committed a single penny, giving you an enormous strategic advantage.

By understanding how sensitive a deal is, you can confidently walk away from fragile investments and focus on those with a robust financial buffer. For anyone who wants to dive deeper into the calculations, our guide on choosing the best investment property calculator in the UK breaks down the key formulas in more detail. This data-driven approach transforms deal analysis from guesswork into a science, empowering you to invest with genuine confidence.

Your Step-by-Step Action Plan to Get Started

Information is only powerful when you act on it. So let's turn everything you've learned into a clear, sequential plan—a personal checklist to take you from property investment beginner to confident property owner by 2026.

The whole process starts long before you even think about viewing a property. It begins with getting your own house in order.

1. Define Your Financial Goals and Prepare Your Deposit

First things first: get specific about what you're actually trying to achieve. Are you aiming for a certain monthly cash flow to supplement your income, or is this all about a long-term capital growth target for retirement? Nailing this down will shape every single decision that follows.

Next, it's all about the deposit. For a typical UK buy-to-let mortgage, you'll need at least 25% of the property's value. Don't forget to budget for the extra costs like Stamp Duty Land Tax and solicitor fees on top. Start saving diligently and get all your financial documents ready to go.

2. Build Your Professional Team

You absolutely cannot succeed in property alone. At a bare minimum, you need two key professionals in your corner from day one:

- A Specialist Mortgage Broker: They have access to landlord-specific mortgages and rates you simply won't find on the high street. Their expertise in navigating the complex lending criteria for investors is invaluable.

- A Property-Savvy Solicitor: Don't just pick any high-street conveyancer. Find one who specialises in investment properties. Their experience can be the difference between a smooth, fast transaction and a costly, drawn-out disaster.

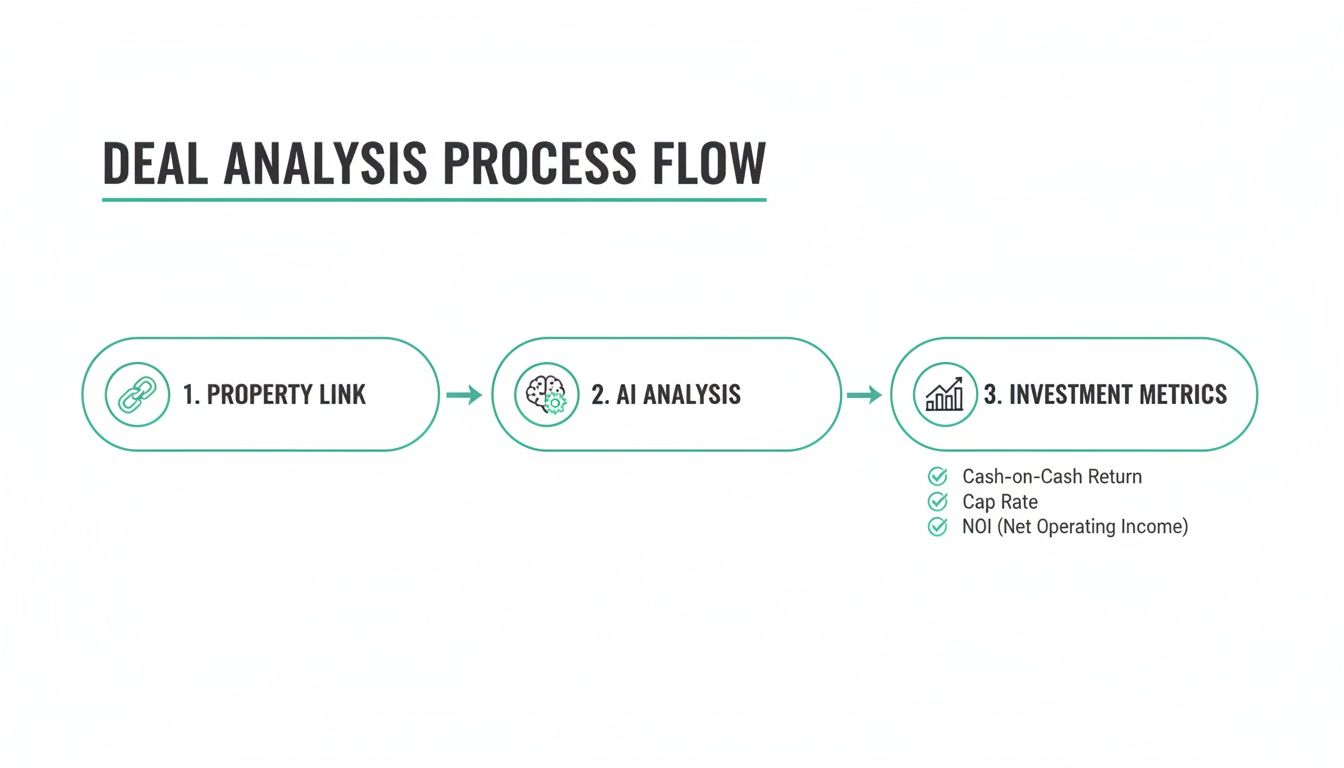

3. Find Promising Areas and Analyse Deals

With your finances sorted and your team ready, now the fun part begins: researching locations that fit your strategy. Look for areas with rock-solid rental demand, great transport links, and clear signs of economic growth or regeneration.

Once you spot a potential property, it's time to analyse it rigorously. The infographic below shows the modern, streamlined way you can crunch the numbers on a deal using an AI-powered tool.

This shows how you can go from a simple property link to a full breakdown of all the key investment metrics in seconds. It's about removing the guesswork and avoiding manual errors in your spreadsheets.

4. Make a Smart Offer and Complete the Purchase

Your offer should always be based on your detailed analysis, not the asking price. Let the numbers guide you.

Once your offer is accepted, your solicitor and mortgage broker will take the lead, guiding you through the legal maze and financial hurdles to get you to completion. Even in a more stable market, solid fundamentals matter more than ever. Provisional data shows average UK house prices rose 3.0% to £273,000 in the year to August 2025, which provides a steady backdrop for new investors. You can discover more about the latest UK house price trends here.

Frequently Asked Questions

Let's tackle some of the most common questions I hear from investors just starting out in the UK property scene. Getting your head around these fundamentals early on can save you a world of pain and costly mistakes down the road.

How Much Money Do I Really Need to Start?

It's the million-dollar question, isn't it? Well, not quite a million, but it's definitely more than just the deposit. While a Buy-to-Let mortgage typically requires a 25% deposit, that's just the headline figure. The real number includes all the costs needed to actually get the keys.

Think of it this way: you need to budget for the entire transaction, not just the down payment. This means factoring in:

- Stamp Duty Land Tax (SDLT): This is a hefty tax on property purchases, and remember, the rates are higher for second homes and investment properties. It's a significant cost.

- Solicitor Fees: You'll need a good solicitor to handle the legal side of the purchase, known as conveyancing.

- Mortgage Arrangement Fees: Most lenders charge a fee for setting up your loan.

- Contingency Fund: This is non-negotiable. It's your buffer for any immediate repairs, essential furnishings, or nasty surprises you discover after you take ownership.

So, what's a realistic starting pot? To cover all of this for a sensible, entry-level UK investment property, you're realistically looking at a budget in the range of £30,000 to £50,000.

Which UK Areas Are Best for Beginners in 2026?

Rather than getting obsessed with chasing specific "hot" postcodes, which often means you're already too late, the real skill is learning to spot the characteristics of a solid investment area. This is a skill that will pay dividends for your entire investing career.

Focus your energy on places with strong fundamentals. You're looking for clear evidence of high and consistent rental demand. Are there major regeneration projects underway, either public or private? How are the transport links? Is the local job market growing?

Cities across the North West, Yorkshire, and the Midlands often tick these boxes, delivering much healthier rental yields compared to the overheated markets in London and the South East. This makes them a popular and effective starting ground for new investors.

The goal is to invest where the economy is growing and people want to live, not just where house prices have recently jumped. Look for sustainable growth drivers, not speculative hype.

What Are the Biggest Risks I Should Prepare For?

Smart investing isn't about avoiding risk; it's about understanding and planning for it. This is what separates a sustainable portfolio from a gamble. The biggest dangers aren't always dramatic market crashes, but the more mundane, cash flow-killing problems that catch new investors out.

The main operational gremlins to watch out for include:

- Underestimating Refurbishment Costs: Always, always get detailed quotes from tradespeople and then add a 15-20% contingency fund on top for the inevitable "while you're at it" problems.

- Long Vacant Periods: In the industry, we call these 'voids'. Every single month a property sits empty, it's not just losing you income; it's actively costing you money in bills and council tax.

- Unexpected Major Repairs: A boiler giving up the ghost or a serious roof leak can easily cost thousands and wipe out your entire profit for the year.

- Rising Interest Rates: If your mortgage rate goes up, your monthly payment follows. This can quickly squeeze your profit margin or even push you into negative cash flow.

The good news is you can guard against these with proper due diligence. That means commissioning a detailed survey, building realistic budgets from day one, and properly stress-testing your numbers. You need to know that your deal still works even if rates rise or you face a couple of empty months.

Ready to analyse your first deal with confidence? Stop wrestling with spreadsheets and let DealSheet AI do the heavy lifting. Get instant, UK-specific financial analysis from any property link to make smarter, faster investment decisions. Download the DealSheet AI app and start your free trial today.