What Is Loan to Value Ratio? A UK Investor's Guide for 2026

What Is Loan to Value Ratio? A UK Investor's Guide for 2026

When you're looking at property finance, you'll hear one term more than any other: what is loan to value ratio? Put simply, the Loan to Value (LTV) ratio is the percentage of a property's value that a lender is willing to finance with a mortgage; the rest is your deposit. Understanding this single metric is the key to unlocking better mortgage deals and building a successful UK property portfolio. For instant, actionable insights on any UK property deal, the DealSheet AI app calculates LTV and all other crucial metrics for you in seconds. This guide will delve deeper into everything you need to know.

Understanding Loan To Value Ratio And Why It Matters

A lower LTV can secure you better interest rates, which directly boosts your monthly cash flow and overall returns. For savvy UK investors, getting a grip on what the loan to value ratio really means is crucial for sizing up deals quickly and accurately.

The Foundation Of UK Property Finance

The loan to value ratio is the bedrock of mortgage lending in the United Kingdom. It's how a lender measures their risk.

A high LTV, say 90%, means the lender is fronting almost the entire purchase, leaving you with just 10% equity. If property prices dip, their loan could suddenly be worth more than the house itself—a nasty situation known as negative equity.

On the other hand, a low LTV of 60% means you've put down a chunky 40% deposit. That large equity stake makes you a much more attractive borrower because the lender's risk is massively reduced. It's why they reward lower LTVs with their most competitive interest rates.

Why LTV Is A Critical Metric For Investors

For a property investor, LTV is way more than just a number to get a mortgage. It dictates several key outcomes of your investment:

- Access to Better Deals: A lower LTV opens the door to cheaper mortgage products. That means less money going to the bank and more net profit in your pocket each month.

- Leverage Control: It defines how much of the bank's money you're using versus your own. While higher leverage can amplify returns on the way up, it also magnifies risk on the way down.

- Refinancing Power: This is a big one for strategies like BRRRR. When you add value to a property through refurbishment, its new, higher valuation allows you to remortgage at a lower LTV, releasing tax-free capital to fund your next project.

Understanding this metric is a foundational step. If you're just starting out, you can explore this further in our complete guide to investing in property for beginners.

"A good rule of thumb is that an LTV-to-CAC ratio of three or higher is attractive and indicates a scalable business where you'll be able to cover your marketing costs, overhead, and still make a profit."

Now, that quote is from a different business world, but it highlights a universal truth: the ratio of value to cost is a core measure of a venture's health. In property, your LTV directly influences your borrowing cost, making it a pivotal factor in the long-term profitability and sustainability of your portfolio. Mastering it is non-negotiable for success.

How to Calculate LTV with Real UK Property Examples

Right, let's get into the numbers. The good news is that the loan-to-value ratio formula is refreshingly simple. It's a core piece of any deal analysis, and you'll use it constantly.

Here's the calculation:

(Loan Amount / Property Value) x 100 = LTV (%)

All this formula does is tell you what percentage of the property's value the lender is covering. The rest is your bit—the deposit or your equity in the deal. Let's walk through a couple of practical, UK-focused scenarios to see how it plays out in the real world.

A Standard Buy-to-Let in Leeds

Let's say you've found a solid buy-to-let flat in Leeds valued at £200,000. You've got a £50,000 deposit saved up and ready to go. To get the keys, you'll need a mortgage for the rest.

- Property Value: £200,000

- Your Deposit: £50,000

- Loan Amount Needed: £150,000 (£200,000 - £50,000)

Now, we just plug those numbers into the LTV formula:

(£150,000 / £200,000) x 100 = 75% LTV

This 75% LTV is bread and butter for UK buy-to-let mortgages. Most lenders are very comfortable at this level, which means you'll have plenty of competitive mortgage products to choose from. Getting these numbers right is non-negotiable, which is why a good UK property investment calculator is such a vital bit of kit for any serious investor.

To make the calculation crystal clear, here's a quick table showing the simple Leeds deal alongside a below-market-value scenario.

LTV Calculation Examples for UK Investment Scenarios

| Scenario | Property Value | Desired LTV | Loan Amount | Required Deposit |

|---|---|---|---|---|

| Standard BTL (Leeds) | £200,000 | 75% | £150,000 | £50,000 |

| BMV Purchase (e.g., Auction) | £150,000 | 75% | £112,500 | £37,500 |

As you can see, the value directly impacts the loan size and the cash you need to bring to the table. The lender always bases their loan on their valuation, not necessarily what you paid.

A More Complex Auction Deal in Birmingham

Now for something with a few more moving parts. You've just won a property at auction in Birmingham for £120,000. It's a wreck and needs a full refurb, which you've budgeted at £30,000. Once the work is done, you're confident it'll be valued at £190,000. This is a classic BRRRR (Buy, Refurbish, Rent, Refinance) play.

The "value" part of LTV changes depending on which stage you're at.

Phase 1: The Purchase To buy it, you'll probably use a short-term bridging loan. If the bridger offers 70% LTV against the purchase price:

- Loan Amount: £84,000 (70% of £120,000)

- Your Initial Capital: £36,000 (deposit) + £30,000 (refurb funds) = £66,000

Phase 2: The Refinance Fast forward a few months. The refurb is done and the property now has a new, higher value of £190,000. You apply for a standard buy-to-let mortgage to pay off the expensive bridging loan. If you target a 75% LTV mortgage on the new value:

- New Mortgage Amount: £142,500 (75% of £190,000)

- Capital Released: £142,500 - £84,000 (to repay the bridge) = £58,500

In this BRRRR scenario, you've successfully pulled out most of your initial £66,000 investment, ready to deploy it on the next project. This is how portfolios are scaled.

Asking Price vs. Bank Valuation: The Only Number That Matters

Here's a critical point that catches out new investors all the time. Which 'value' should you use in your sums? The seller's asking price, your offer price, or the bank's official valuation?

It's always the lender's valuation. A lender will only base their loan amount on what their appointed surveyor says the property is worth.

It doesn't matter what you've agreed to pay. If you offer £210,000 for a property that the bank's surveyor only values at £200,000, the lender will calculate their 75% LTV loan on the lower £200,000 figure. That means you'd have to find an extra £10,000 out of your own pocket to bridge the gap. This is what we call a down-valuation, and it's a deal killer if you're not prepared for it.

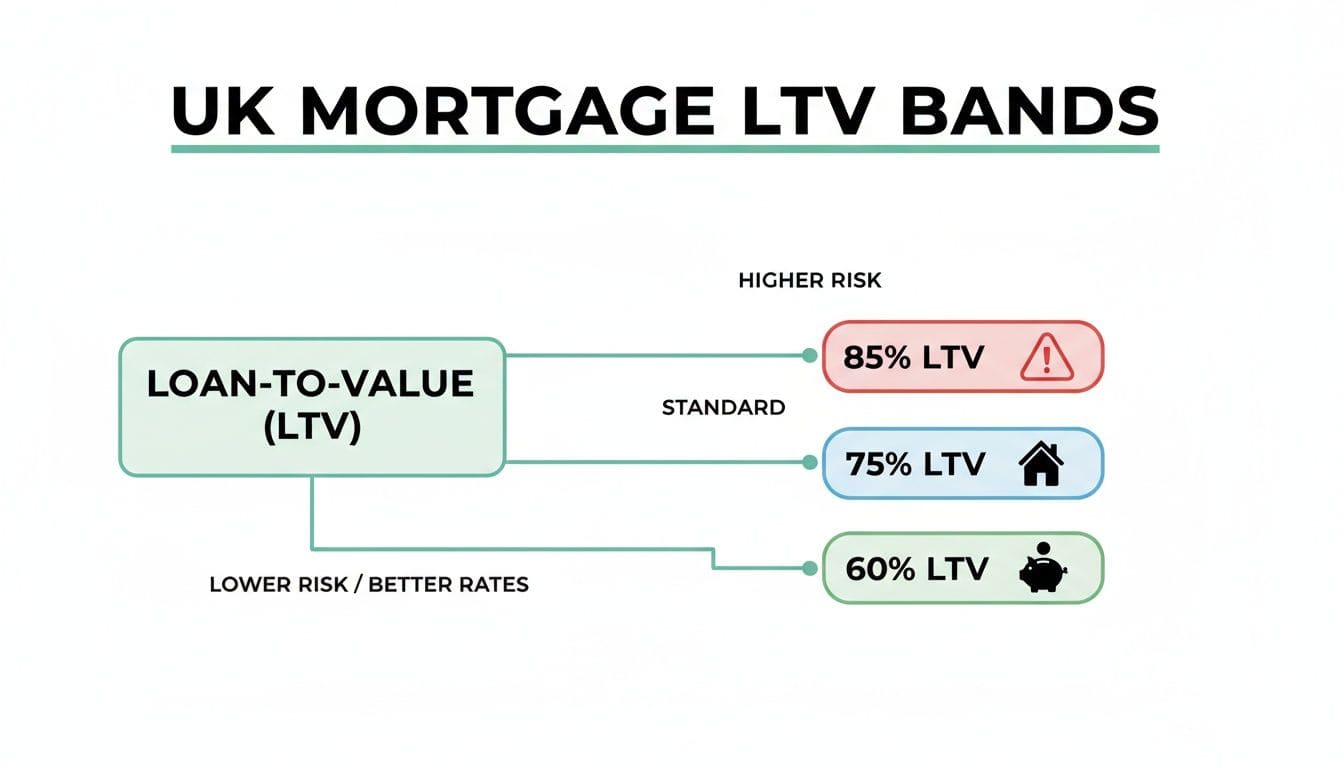

Getting Your Head Around UK Mortgage LTV Bands

When you're dealing with UK lenders, it's a mistake to think of the loan-to-value ratio as a smooth, sliding scale. It's not. Instead, lenders package their mortgage products into distinct LTV bands. Think of them like tiers. Shifting from a higher band to a lower one—even by a tiny margin—can unlock significantly better interest rates and more flexible terms.

This isn't just some technical detail; it's a fundamental part of your financing strategy. A small bump in your deposit could be all it takes to drop into a more attractive tier, potentially saving you thousands over the life of your mortgage.

The Key LTV Thresholds for UK Investors

For property investors, the LTV bands you'll come up against time and time again are 85%, 80%, 75%, and 60%. Each one signals a different level of risk for the lender and, in turn, a different cost of borrowing for you.

- 85% LTV: This is pretty much the ceiling for buy-to-let mortgages, usually only offered by specialist lenders. It lets you use the most leverage but comes with the steepest interest rates and the toughest stress tests.

- 75% LTV: This is the bread and butter of the UK buy-to-let world. A huge number of lenders play in this space, making it a competitive and common sweet spot for investors.

- 60% LTV: Dropping to this level often gets you access to the best deals on the market. Lenders see a 40% deposit as very low risk, and they reward you with their most preferential rates.

The logic is simple: the more of your own cash you put into a deal, the lower your LTV, and the less risk the bank takes on. They pass that reduced risk straight back to you in the form of a lower interest rate.

This tiered system is a massive feature of the UK lending scene. You can see how much it matters in recent data. At the end of 2023, the vast majority of new mortgages were granted at LTVs of 75% or less. This shows a clear pattern of borrowers stretching to find bigger deposits just to hit those better-priced tiers. You can dig into more of this data and find detailed insights on mortgage statistics from Uswitch. The trend just confirms how vital it is to aim for these key thresholds when you're planning your investments.

LTV Bands Across Different Finance Products

While the concept of LTV bands is universal, the actual percentages change depending on the type of finance you're after. The risk profile of the deal dictates the numbers, and getting to grips with these differences is crucial for picking the right funding.

Buy-to-Let and HMO Mortgages

For standard buy-to-let (BTL) and Houses in Multiple Occupation (HMO) properties, 75% LTV is the most common ceiling. You might find specialist lenders willing to push to 85%, but the choice of products gets much thinner, and the affordability calculations become a lot more demanding. For portfolio landlords trying to maximise cash flow, a common strategy is to target a 60% or 65% LTV on remortgages to lock in the lowest possible interest payments.

Bridging Loans and Auction Finance

Bridging finance plays by slightly different rules. Lenders in this space often talk about LTV against the purchase price or the open market value—whichever is lower. A typical bridging loan might go up to 75% LTV, but if it's a riskier project, like a wreck bought at auction that needs a full gutting, the LTV offered might drop to 65% or 70%.

The BRRRR Strategy LTV Sweet Spot

If you're using the Buy, Refurbish, Rent, Refinance (BRRRR) strategy, your entire project hinges on the refinance stage. The goal is to exit your short-term finance onto a standard BTL mortgage once you've forced the property's value up. The crucial bit is making sure the final loan, based on a 75% LTV of the new, higher value, is big enough to pay back the bridge and pull out your initial capital. Hitting that post-renovation LTV target is absolutely critical to making the whole thing work.

LTV vs LTC vs Gearing: Decoding Key Finance Metrics

To really get to grips with property finance, you have to speak the lender's language. While knowing what is loan to value ratio is the first step, it's only one piece of the puzzle. Two other critical metrics, Loan to Cost (LTC) and Gearing, give you different—but equally vital—perspectives on a deal's financial health.

Looking beyond LTV is what separates a surface-level analysis from a professional one. When you understand when and how to use each of these three metrics, you can make sharper, more profitable decisions and properly assess the risk you're taking on.

Loan to Cost (LTC): The Developer's Metric

While LTV measures your loan against a property's current market value, Loan to Cost (LTC) measures the loan against the total cost of the project. This is the go-to metric for developers, flippers, and anyone doing a serious refurbishment.

So, why the distinction? Because for a project, the purchase price is just the start of the story. The total project cost includes a whole host of other expenses that lenders need to see covered.

- Purchase Price: The headline figure for buying the property.

- Acquisition Costs: Things like Stamp Duty Land Tax (SDLT), legal fees, and survey costs.

- Renovation Budget: All the cash allocated for construction, materials, and labour.

Lenders use LTC to make sure you have enough of your own capital—your 'skin in the game'—invested across the entire project, not just the initial purchase. A development finance lender might offer 80% LTC, which means you'd need to fund the remaining 20% of the total project costs yourself. For anyone taking on a major project, understanding the projected final value is also crucial, which you can dive into in our guide on what is Gross Development Value.

Gearing: The Portfolio View

If LTV looks at a single property and LTC examines a single project, Gearing (often called leverage) zooms out to give you a bird's-eye view of your entire portfolio. It simply measures your total debt against the total value of your assets.

Gearing (%) = (Total Debt / Total Portfolio Value) x 100

This metric is essential for portfolio landlords. It shows how much of your property empire is funded by debt versus your own equity. A high gearing ratio, say above 80%, signals significant risk to lenders. If the market takes a downturn, your equity could get wiped out fast. On the other hand, a low gearing ratio, like 50%, shows a robust, stable portfolio with a healthy safety buffer. Managing your overall gearing is a core part of long-term risk management.

The infographic below shows the common LTV bands that directly influence the gearing on your individual properties.

As you can see, risk drops as you move from high LTV bands like 85% to safer, lower bands like 60%, which in turn unlocks better mortgage rates.

Comparing LTV, LTC, and Gearing for UK Investors

Knowing which metric to apply is the sign of a sharp investor. Using the wrong one can lead to a flawed analysis and poor decisions. The table below breaks down the key differences to help you choose the right tool for the job.

| Metric | What It Measures | Primary Use Case |

|---|---|---|

| Loan to Value (LTV) | The loan amount relative to the property's current market value. | The default for most property finance, especially standard buy-to-let purchases and remortgages. |

| Loan to Cost (LTC) | The loan amount relative to the total project cost (purchase + fees + refurb). | Essential for property flips, developments, and BRRRR deals where significant capital expenditure is needed. |

| Gearing | Total debt across all properties relative to the total value of your entire portfolio. | Used for portfolio health checks, refinancing strategies, and securing further funding for expansion. |

By using LTV for individual deals, LTC for projects, and Gearing for your overall strategy, you build a complete financial picture. This multi-faceted view allows you to spot opportunities and manage risks far more effectively than relying on a single number ever could.

Actionable Ways to Improve Your LTV

Securing a better loan to value ratio isn't just about having more cash; it's about deploying smart, proactive investment strategies. A lower LTV makes you a much more attractive borrower, unlocking better interest rates and strengthening your financial position from day one.

While the most obvious route is simply finding a larger deposit, savvy UK investors have several other tools at their disposal to improve their LTV. These tactics focus on either increasing the 'value' part of the equation or reducing the 'loan' part, giving you far more control over your financing.

Increase Your Deposit

This is the most direct way to lower your LTV. Putting more of your own money into the deal reduces the amount you need to borrow, which is a straightforward way to cut the lender's risk.

It's also the quickest path to dropping into a more favourable LTV band, such as from 75% down to 60%, where the best mortgage rates are often found. For example, on a £200,000 property, a £50,000 deposit gives you a 75% LTV. By stretching to an £80,000 deposit, your LTV drops to 60%, potentially saving you a significant amount in interest payments over the mortgage term.

Source Below Market Value Deals

A more sophisticated strategy is to purchase property Below Market Value (BMV). This means acquiring an asset for less than its official surveyed valuation, creating instant equity on the day you complete. Lenders typically calculate LTV based on the lower of the purchase price or the valuation, but having that built-in equity makes your application much stronger.

Imagine a property with a market value of £250,000. You manage to negotiate a purchase price of £225,000. If you need a loan for £187,500, the lender sees this as a 75% loan against the £250,000 valuation. But you only had to find a deposit of £37,500—effectively achieving a high-leverage deal at a prime LTV.

This is a powerful way to reduce the cash you need to bring to a deal while still securing a favourable LTV in the lender's eyes.

Force Appreciation Through Refurbishment

For investors using the BRRRR (Buy, Refurbish, Rent, Refinance) method, improving your LTV is the entire point of the refinance stage. By carrying out a strategic refurbishment, you can significantly increase a property's market value.

When it comes time to refinance, the lender will base their new mortgage offer on this higher, post-renovation valuation. This allows you to secure a larger loan amount while maintaining a standard LTV, like 75%, which is central to recycling your capital. You might use a short-term bridging loan to buy and renovate, then refinance onto a standard mortgage to pay back the bridge and pull your initial investment back out.

If you're considering this route, it's wise to get familiar with how a bridging loan calculator works to accurately model your costs.

Ultimately, these strategies show you have more control over your loan to value ratio than you might think. By increasing your deposit, hunting for BMV deals, or forcing appreciation through smart renovations, you can actively engineer a better financial outcome for every property you buy.

Ditching the Spreadsheet: Automating Your LTV Analysis with DealSheet AI

Let's be honest. Manual calculations are slow, they're repetitive, and they're a breeding ground for human error. In a UK property market that moves at pace, spending hours plugging numbers into a spreadsheet for every potential deal is a sure way to miss out on the best opportunities.

Speed and accuracy are your real competitive advantages. This is where the right tool completely changes your workflow. Imagine analysing the full financial picture of a property deal in seconds, not hours. Modern tools turn the entire process of calculating the loan to value ratio and modelling different outcomes from a chore into an automated, error-free system.

Instant Analysis Straight From a Property Link

The process can be ridiculously simple. With an app like DealSheet AI, you just paste a property link from a portal like Rightmove or Zoopla. The AI instantly pulls the key data—purchase price, location, bedroom count, and more. That alone cuts out the manual data entry, which is often the first major bottleneck.

From there, you can model different LTV scenarios with just a few taps. Want to compare a standard 75% LTV mortgage against a more aggressive 80% LTV option? You can see the knock-on effects across all your key metrics in an instant.

- Cash Flow Impact: See immediately how a higher loan amount hits your monthly profit after all costs are paid.

- Return on Investment (ROI): Understand how different levels of leverage change your overall returns on the cash you've put in.

- Stress Testing: Analyse how resilient your deal is to future interest rate changes at various LTVs.

Making Decisions with Data, Not Guesswork

This isn't just about convenience; it's about being able to make faster, data-driven decisions with real confidence. Keeping an eye on official lending trends gives you the context for these decisions. For instance, looking ahead to 2026, analysts will be watching to see if the surge in gross mortgage advances seen in late 2025 continues, indicating a dynamic market. In such conditions, investors who can quickly analyse the loan to value ratio are better placed to adapt and secure good terms on their next Buy-to-Let or flip.

Below is a screenshot from the DealSheet AI app, showing how it lays out a clear financial summary for a potential investment.

As you can see, it clearly lays out vital metrics like net cash flow, yield, and return on investment, turning complex calculations into an easy-to-read dashboard. This allows you to compare multiple opportunities side-by-side, using consistent and accurate data for every single one.

By automating LTV calculations and scenario modelling, you free up your time to focus on what truly matters: finding great deals and building your portfolio. Let the technology handle the number crunching, so you can handle the strategy.

This approach gives you a critical edge. You can analyse more deals, make offers faster, and build your portfolio on a solid financial foundation. To see how this works in practice, you can learn more about the app's powerful features and how they apply to different UK investment strategies.

Your LTV Questions, Answered

Alright, we've been through the mechanics of loan to value, the calculations, and how it plays into different lending scenarios. Let's wrap up by tackling the questions that come up time and time again from UK property investors.

Think of this as the quick-fire round. No waffle, just straight answers to help you lock in the concepts for your next deal.

What's a Good LTV for a UK Buy to Let Mortgage?

For a standard buy-to-let mortgage in the UK, 75% LTV is the magic number. It's the industry benchmark and the ceiling for what most mainstream lenders are comfortable with. This makes it the go-to target for investors wanting to make their deposit stretch as far as possible while still getting access to decent finance.

But is it the best LTV? Often, no. If you've got the cash to drop your borrowing to 60% LTV, you'll find lenders suddenly start offering much more attractive interest rates. A lower LTV means less risk for them, and they reward you for it. This can seriously boost your monthly cash flow and build a bigger buffer into your investment.

You might see specialist lenders advertising deals up to 85% LTV, but be warned. Those products always come with a sting in the tail – higher rates, stricter stress tests, and bigger fees. The right LTV really boils down to your strategy: are you trying to maximise leverage to grow faster, or maximise monthly profit to stay safer?

Does My Personal Credit Score Affect My LTV Ratio?

Your credit score doesn't change the LTV formula itself—that's just simple maths. But your credit history is absolutely critical in deciding whether a lender will even offer you a mortgage at your target LTV.

Think of it this way: a strong credit score is your ticket to the best deals, especially at higher LTVs like 75%. If your credit history is patchy, lenders see you as a bigger risk. To protect themselves, they might cap the maximum LTV they'll offer you. This could mean you're forced to find a much larger deposit to get the deal over the line or have to turn to more expensive specialist finance.

Can I Get a 100 Percent LTV Mortgage for an Investment Property in the UK?

In a word: no. The days of 100% LTV mortgages for investment properties vanished after the 2008 financial crisis, and they aren't coming back. That kind of lending is now seen as far too risky.

Every UK mortgage lender now insists that property investors have some 'skin in the game'. As a rule of thumb, this means putting down a deposit of at least 25% of the property's value, which pegs your mortgage to a 75% LTV.

The closest you can get to a "no money left in" deal these days is by using a strategy like BRRRR (Buy, Refurbish, Rent, Refinance, Repeat). With this approach, you buy a property, add value through refurbishment, and then refinance based on its new, higher valuation. If you play your cards right, you can pull out most, or sometimes all, of your initial capital. But you absolutely still need the funds to buy and refurbish the property in the first place.

Ready to stop guessing and start analysing property deals with precision? The DealSheet AI app automates your LTV calculations and provides a complete financial breakdown in seconds. Download it today from the App Store and start your free trial.