Property Investment Calculator UK: Your 2026 Guide to Analysing Deals

Property Investment Calculator UK: Your 2026 Guide to Analysing Deals

In the UK property market, successful investing hinges on accurate financial analysis, not guesswork. The essential tool for this is a property investment calculator UK, which provides the data-driven insights needed to distinguish a profitable deal from a costly mistake. It allows you to model key metrics like cash flow, rental yield, and Return on Investment (ROI) with precision, ensuring you understand a property's true potential before you commit. For investors looking to leverage technology for faster, more accurate analysis that incorporates complex UK tax rules, the DealSheet AI app offers an immediate, actionable solution.

Why a Property Investment Calculator Is Your Most Important Tool

Trying to invest in property without the right tools is like navigating a new city without a map. You might get there eventually, but you'll probably take a few expensive wrong turns and miss the best opportunities along the way. That's what a dedicated calculator does for a UK investor: it's your data-driven roadmap.

A solid property investment calculator lets you model the metrics that actually matter—like rental yield, cash flow, and Return on Investment (ROI)—giving you an objective verdict on a deal's potential. Many investors start with spreadsheets, but they quickly become a liability. They're clumsy, prone to broken formulas, and a nightmare to keep updated with ever-changing UK tax rules.

Navigating Market Realities with Data

The UK property market is rarely predictable. Relying on intuition is a high-risk game when hard data can point you in the right direction. Just look at the recent swings: house prices hit an all-time high of 517.10 points back in October 2025. Projections from Trading Economics suggest the UK House Price Index will hover around 529.53 points in 2026, pointing to a market that's stabilising but still full of challenges.

This guide will show you how these calculators work, what numbers you need to feed them, and how to read the outputs to build a genuinely successful portfolio. If you're just getting started, our beginner property investment guide is a great place to build your foundations.

The Core Benefits of a Calculator

Using a specialised tool enforces a disciplined, methodical approach to analysing deals, making sure no critical cost gets overlooked. It's about more than just convenience.

Here are the real advantages:

- Speed and Efficiency: Analyse multiple deals in the time it would take to build one messy spreadsheet. This lets you move fast when a genuinely good opportunity comes along.

- Accuracy and Consistency: Purpose-built tools kill the risk of human error in your formulas. More importantly, they automatically apply complex UK-specific rules like Stamp Duty Land Tax (SDLT) and Section 24 mortgage interest relief.

- Clarity and Confidence: A good calculator translates a mountain of financial data into metrics you can actually use, like monthly cash flow and ROI. It empowers you to make decisions based on facts, not fear or hype.

Deconstructing the Core Calculator Inputs

The old saying in financial modelling is brutally simple: 'garbage in, garbage out'. The answers a property investment calculator UK gives you are only as reliable as the numbers you feed it. Get one cost wrong, and your entire forecast can fall apart.

A truly accurate analysis starts by getting forensic with the figures. We'll begin with the obvious ones, but the real devil is in the UK-specific details that are so easy to miss. Nailing these inputs is the difference between a realistic projection and a dangerous fantasy.

Purchase and Transaction Costs

Long before you see a penny of rent, you need to account for the total cash required to actually get the keys. This goes way beyond the headline purchase price.

- Purchase Price: This is the big number you agree to pay for the property itself.

- Deposit: The cash you're putting into the deal. For a typical UK buy-to-let mortgage, you'll be looking at somewhere between 15% and 25% of the purchase price.

- Stamp Duty Land Tax (SDLT): This is a huge one. It's a tiered tax on property purchases in England and Northern Ireland, and the rates are significantly higher for additional properties—which catches virtually every buy-to-let investor. Getting this calculation right is non-negotiable. You can dig into the specifics in our complete guide to the Stamp Duty Land Tax calculator.

- Legal Fees: You'll need a solicitor to handle the conveyancing. Budget anywhere from £850 to £2,000, sometimes more if the purchase gets complicated.

- Survey and Valuation Fees: Your mortgage lender will insist on a valuation, but it's a smart move to get your own, more detailed survey (like a HomeBuyer Report) to uncover any nasty surprises before you commit.

Financing Details

Unless you're buying with cash, your mortgage will be your single biggest outgoing. The terms you secure will make or break your monthly cash flow, so your calculator needs the exact figures.

Make sure you have these details:

- Mortgage Interest Rate: The percentage the bank is charging you. This has a direct and massive impact on your monthly profit.

- Mortgage Term: The length of the loan, which is typically 25 years in the UK for a buy-to-let.

- Arrangement Fees: These are the setup fees from the lender. They can often be added to the loan, but they are still a cost you need to account for.

Critical Operational Costs

Once you own the property, a whole new set of running costs kicks in. Underestimating these is probably the most common mistake investors make, and it's an expensive one. Any decent property investment calculator should force you to think about these to keep your numbers grounded in reality.

Factor in these key operational costs:

- Insurance: You can't use a standard homeowner policy. You need specialist landlord insurance to cover the building, your liability, and often loss of rent.

- Maintenance Provision: Things break. A sensible rule of thumb is to set aside 1% of the property's value each year for repairs. On a £200,000 property, that's £2,000 a year, or about £167 a month. Don't skip this.

- Letting Agent Fees: If you're not self-managing, your agent's fees will be a significant slice of your income. Expect to pay between 8% and 15% of the monthly rent for tenant-finding or full management.

- Void Periods: No property stays tenanted 100% of the time. To be safe, always budget for at least one month of vacancy every year.

The single most overlooked input is tax. Forgetting to model UK-specific rules like Section 24 can make a deal that looks profitable on paper a genuine loss-maker once HMRC sends the bill.

And finally, you have to consider the impact of Section 24. This is a UK tax rule that stops individual landlords from deducting their mortgage interest costs from their rental income before calculating their tax bill. Instead, you get a tax credit equal to 20% of your interest payments. For higher-rate taxpayers, this can dramatically inflate your tax liability and torpedo your profits. Any credible UK calculator must have this built in.

Mastering the Key Performance Metrics

Once you've fed all your data into a property investment calculator, it gets to work, translating those raw numbers into a handful of powerful metrics. These outputs are the verdict on your deal—but only if you know how to read the language. They tell you everything from your monthly profit to just how hard your invested cash is working for you.

Frankly, understanding these figures is what separates a hopeful speculator from a calculated investor. It's how you can compare a city-centre flat against a suburban semi-detached using the same objective rules. This is where a good calculator earns its keep.

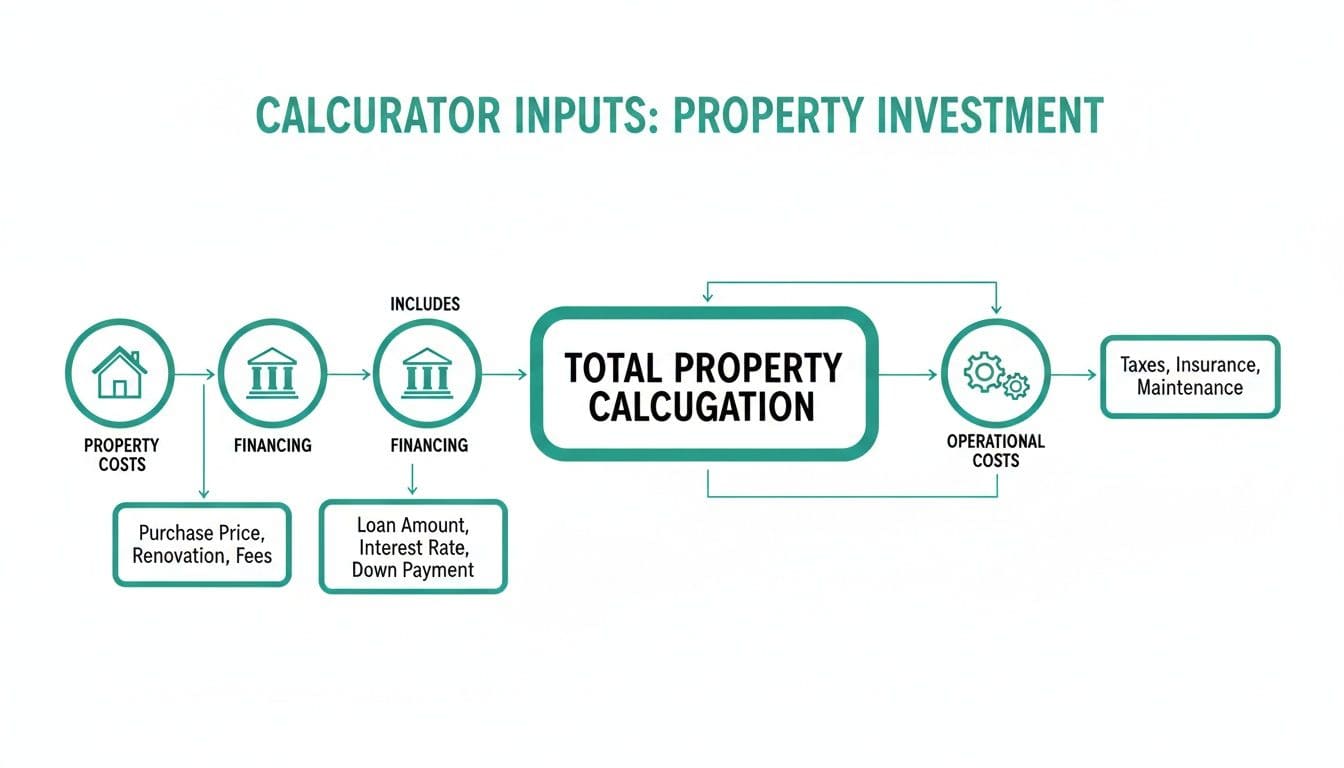

The process starts with solid inputs. As the flowchart shows, every accurate analysis is built on three pillars of data: the property's purchase costs, your financing details, and the real-world operational expenses.

Get these inputs wrong, and the outputs, no matter how precise they look, will be fiction.

Gross Yield vs Net Yield

The first metric you'll almost always see is rental yield, but it comes in two distinct flavours: gross and net. It's easy to get excited by a big gross yield figure, but be warned—it's a vanity metric that can be dangerously misleading.

- Gross Yield: This is the quick-and-dirty calculation: total annual rent divided by the purchase price. It's fine for a rapid first filter of a dozen properties, but it ignores every single cost of ownership.

- Net Yield: This is the number that actually matters. It takes your annual rent, subtracts all your running costs (mortgage interest, insurance, maintenance, voids, fees), and then divides that true profit by the total cash you actually put into the deal.

Net yield is the only honest measure of an asset's profitability. It shows you what the property is really earning after it has paid for itself. This gives you a far more realistic picture of its performance.

Focusing on net yield forces you to be brutally honest about your expenses, giving you a much clearer view of the investment's financial health. We dive deeper into the nuances in our guide on how to calculate rental yield in the UK.

Cash Flow: The Lifeblood of Your Portfolio

While yield is a percentage, cash flow is the actual, physical money left in your bank account each month after every single bill has been paid. For buy-and-hold investors, this is the most critical metric for long-term survival and growth.

Monthly Rent - (Mortgage Payment + All Operating Costs) = Monthly Cash Flow

Think about it: a property with a high yield on paper but negative cash flow is a liability, not an asset. It's actively draining your personal finances every month just to keep it afloat. A positive cash flow, even a modest one, means the property is self-sustaining and adding to your income. This provides the buffer for surprise repairs and is the absolute foundation for scaling your portfolio.

Return on Investment (ROI)

Return on Investment, which property folk often call 'Cash on Cash Return', gets right to the heart of capital efficiency. It answers one vital question: for every pound you pulled together for this deal, how many pennies is it putting back in your pocket each year?

The formula is simple: Annual Net Profit / Total Cash Invested = ROI %

'Total Cash Invested' isn't just your deposit. It's every pound you had to find to get the deal over the line and tenant-ready—your deposit, Stamp Duty, legal fees, and any refurb costs.

A strong ROI (many UK investors aim for 8% or higher) shows your capital is working hard for you. This metric is essential for comparing a property investment against other opportunities, whether that's stocks, savings accounts, or another property down the road.

The Payback Period

Finally, the payback period tells you something simple: how long will it take for the investment's net profits to repay your initial cash outlay?

A shorter payback period generally means a lower-risk investment. Your capital is returned to you faster, ready to be pulled out and redeployed into your next deal. It's a fantastic sense-check, especially for strategies like BRRRR where recycling your cash is the name of the game.

Analysing Different UK Property Strategies

The theory is one thing, but a property investment calculator only really proves its worth when you start plugging in real numbers from actual deals. Every strategy has its own financial fingerprint—a unique mix of income streams, cost structures, and risks. The right calculator lets you model these differences accurately, giving you the clarity to decide which path actually lines up with your goals.

So, let's run the numbers on four common UK property strategies to see how the analysis shifts from one to the next. We'll cover everything from a straightforward rental to a fast-paced flip. For a deeper dive into the pros and cons of each, check out our full breakdown of UK property investment strategies.

Example 1: The Classic Buy-to-Let

The standard buy-to-let (BTL) is the bread and butter of countless UK property portfolios. The game here is all about steady, long-term returns driven by rental income and gradual capital growth. For a BTL, the calculator's most important outputs are Net Yield and Monthly Cash Flow.

Let's imagine a two-bedroom terraced house in Manchester.

- Purchase Price: £200,000

- Deposit (25%): £50,000

- Stamp Duty & Fees: £8,000 (as it's an additional property)

- Total Cash Invested: £58,000

- Monthly Rent: £1,100

- Mortgage Payment (5.5% Interest-Only): £688

- Monthly Costs (Insurance, Maintenance, Voids): £200

When we plug this into a calculator, the gross annual rent is £13,200. After we subtract the yearly mortgage bill (£8,256) and running costs (£2,400), we're left with a net profit of £2,544. This breaks down to a monthly cash flow of £212 and a respectable ROI of 4.39% on the cash we put in.

Example 2: The High-Yielding HMO

A House in Multiple Occupation (HMO) means renting a property out on a room-by-room basis, usually to students or young professionals. This approach can seriously boost your rental income, but it comes with a trade-off: higher setup costs, tougher regulations, and far more hands-on management.

Let's analyse a five-bedroom HMO near the University of Nottingham.

- Purchase Price: £275,000

- Conversion & Furnishing Costs: £25,000

- Deposit (25%): £68,750

- Stamp Duty & Fees: £12,500

- Total Cash Invested: £106,250

- Rent per Room: £550/month (Total: £2,750/month)

- Mortgage Payment (6% Interest-Only): £1,375

- Monthly Costs (Bills, Council Tax, Voids, Management): £750

Here, the gross annual rent shoots up to a massive £33,000. But the annual costs are also much chunkier at £25,500 (£16,500 for the mortgage plus £9,000 for everything else). The calculator crunches the numbers to show an annual net profit of £7,500, which gives us a strong monthly cash flow of £625 and an impressive 7.06% ROI. That higher return is your reward for taking on more risk and management headaches.

Example 3: The Serviced Accommodation Unit

Serviced Accommodation (SA), or short-term lets, is a hospitality-based model targeting tourists and business travellers. You can achieve hotel-like nightly rates, but you also have to contend with fluctuating occupancy, much higher cleaning costs, and the rollercoaster of seasonal demand.

Let's model a one-bedroom flat in a tourist-heavy city like Bath.

- Purchase Price: £250,000

- Furnishing & Setup: £10,000

- Deposit (25%): £62,500

- Stamp Duty & Fees: £10,500

- Total Cash Invested: £83,000

- Average Nightly Rate: £120

- Projected Occupancy: 70% (around 21 nights a month)

- Gross Monthly Income: £2,520

- Monthly Costs (Mortgage, Utilities, Cleaning, Platform Fees): £1,700

The single most important input for an SA calculation is the occupancy rate. Being too optimistic here can quickly turn a profitable-looking deal into a money pit during the off-season. Always, always use conservative figures backed by real data.

In this scenario, our property investment calculator projects a gross annual income of £30,240. After taking off annual costs of £20,400, the net profit stands at £9,840. That means a monthly cash flow of £820 and an outstanding ROI of 11.85%. The high return reflects the fact that you're essentially running a small hospitality business, not just a simple rental.

Example 4: The Buy-to-Sell Flip

Unlike rental strategies, a flip is a short-term sprint for capital gain. The analysis completely shifts away from monthly income and focuses squarely on the final profit margin. Here, the key calculation is the Gross Development Value (GDV) minus every single cost involved.

Let's look at a three-bedroom semi-detached in Bristol that needs a complete overhaul.

- Purchase Price: £300,000

- Refurbishment Costs: £40,000

- Transaction & Holding Costs (Stamp Duty, Fees, Bridging Finance): £35,000

- Total Project Cost: £375,000

- Projected GDV (After-Repair Value): £450,000

For a flip, the calculator's job is straightforward: subtract the total costs from the end value.

£450,000 (GDV) - £375,000 (Total Costs) = £75,000 (Gross Profit)

The metric that really matters here is Return on Cost, which shows a profit of 20% (£75,000 profit / £375,000 cost). This example perfectly illustrates why a good calculator needs to be flexible enough to handle entirely different investment models—from steady cash flow to one-off, lump-sum profits.

Strategy Metric Comparison at a Glance

Each property strategy prioritises different financial outcomes and comes with its own risk profile. The table below offers a quick comparison of what investors typically focus on for each approach in the UK market.

| Strategy | Primary Metric | Typical UK ROI Range (%) | Key Risk Factor |

|---|---|---|---|

| Buy-to-Let (BTL) | Monthly Cash Flow & Net Yield | 3-6% | Tenant Voids / Arrears |

| HMO | Monthly Cash Flow & ROI | 6-12% | Regulatory Compliance & Management Intensity |

| Serviced Accommodation | ROI & Occupancy Rate | 8-15%+ | Seasonal Demand & Operational Complexity |

| Buy-to-Sell (Flip) | Return on Cost & Gross Profit | 15-25% | Market Fluctuation & Cost Overruns |

Ultimately, there is no single "best" strategy. The right one depends entirely on your financial goals, appetite for risk, and how much time you're willing to commit. A robust calculator simply gives you the tools to compare them on a level playing field.

Sidestepping the Most Common Investment Calculation Mistakes

A solid property investment calculator UK is a massive advantage in any investor's toolkit, but it isn't a magic wand. Simple, avoidable errors can completely warp your projections, turning what looks like a brilliant deal on paper into a financial nightmare.

Learning to spot these common mistakes—and sidestep them—is a critical skill for building a resilient, long-term property portfolio.

The most frequent and dangerous error? Underestimating the true cost of ownership. It's all too tempting to focus on the headline figures of rent and mortgage payments, but the devil is always in the details that chip away at your profit margin, month after month.

Underestimating Ongoing Costs

A property isn't a static asset; it's a dynamic one that constantly demands money to keep it running smoothly and legally compliant. Ignoring these smaller, recurring costs is a fast track to negative cash flow.

Three of the most commonly overlooked costs are:

- Void Periods: No property is tenanted 100% of the time. Tenants move out, and finding new ones takes time. A conservative calculator should always factor in at least one month of vacancy per year to accurately reflect lost income and the council tax you'll be liable for during that period.

- Routine Maintenance: This isn't about big disasters; it's the small stuff. The dripping tap, the faulty light switch, the annual gas safety check. A sensible rule of thumb is to budget 1% of the property's value annually for these ongoing repairs.

- Major Capital Expenditures (CapEx): This is the big one that catches so many investors out. A boiler doesn't last forever (typically 10-15 years), and neither does a roof. You absolutely must set aside funds every month for these eventual, high-cost replacements. Failing to build a CapEx fund means a sudden £3,000 boiler bill will have to come from your personal savings, wrecking your returns.

Relying on Overly Optimistic Projections

Hope is not a strategy. Another major pitfall is plugging overly optimistic figures into your property investment calculator. It's easy to get swept up by the highest potential rent an agent suggests or to assume interest rates will stay low forever.

A professional investor's forecast is built on conservative, market-validated data. Always use the average local rent for a comparable property, not the absolute peak. This grounds your analysis in reality and protects you from market fluctuations.

This is exactly where stress-testing becomes essential. A robust financial model doesn't just show you the best-case scenario; it shows you what happens if things go sideways.

Forgetting to Run Essential Stress Tests

Stress-testing isn't just a "nice-to-have"; it's a fundamental part of risk management. It means deliberately changing key variables in your calculator to see how sensitive your investment is to external shocks. It's how you prepare for the inevitable bumps in the road.

Before you even think about committing to a deal, you must run these scenarios:

- Interest Rate Rises: What happens to your monthly cash flow if your mortgage rate jumps by 1%, 2%, or even 3% when your fixed term ends? A deal that looks great today can quickly become unprofitable if you haven't accounted for future rate changes.

- Extended Void Periods: How does the investment hold up if the property is empty for two or three months instead of just one? Can you still cover the mortgage and bills without digging into your own pocket?

- Unexpected Maintenance Costs: Model a sudden, large repair bill. If a £5,000 roof repair hits in year two, does it wipe out all your profits, or does your cash flow provide a sufficient buffer?

By running these tests, you move from wishful thinking to strategic planning. You'll highlight the vulnerabilities in a deal and ensure your investment can actually withstand the market pressures that are an unavoidable part of property ownership in the UK.

Moving from Calculation to Confident Investment

The numbers on your property investment calculator look good, but a spreadsheet isn't a signed deal. This is the final, critical phase: moving from on-screen analysis to on-the-ground action. It's where you systematically prove every assumption you've made, turning a digital forecast into a tangible, confident investment.

This process is all about bridging the gap between theory and reality. A confident purchase isn't made by just trusting a calculator; it's made by proving the outputs are accurate in the real world. Think of this as your essential due diligence checklist before you commit a single pound.

Validating Your Assumptions

Your calculator's outputs are only as strong as its inputs. Now is the time to stress-test them against the local market. This isn't optional; it's the bedrock of responsible investing.

- Confirm Rental Demand: Get on the phone with at least three local letting agents. Ask them about current rental values for similar properties, typical void periods, and the kind of tenant you can expect. Their on-the-ground knowledge is pure gold for validating your income projections.

- Get Firm Renovation Quotes: If your strategy involves any kind of refurbishment, get detailed, written quotes from local tradespeople. Vague estimates are a recipe for budget overruns that can destroy your profit margin before you even start.

- Secure an Agreement in Principle (AIP): Talk to a mortgage broker and get an AIP from a lender. This confirms you can get the financing you need and locks in a realistic interest rate for your calculations, protecting you from nasty surprises down the line.

From Verification to Action

Once your core assumptions are validated, it's time for one final check. This is where a tool like the DealSheet AI app becomes invaluable. You can quickly plug in your verified numbers to see how they affect your final ROI and cash flow. More importantly, you can instantly compare your deal against other market opportunities to ensure it truly is the best use of your capital.

For a comprehensive overview of this final stage, have a look at our complete guide to analysing UK buy-to-let deals in 2026.

A truly successful investment is born from a combination of diligent digital analysis and rigorous real-world validation. One without the other is simply a gamble.

By following this two-stage process—calculate, then verify—you replace hope with certainty. You move forward not just with good numbers, but with the confidence that those numbers are grounded in reality, ready to deliver the returns you expect.

A Few Final Questions

Got a few lingering questions? Here are the straight answers to some of the most common queries investors have when they start using property investment calculators.

Just How Accurate Are These Things?

A calculator's accuracy is a direct reflection of your own research. Think of it as a powerful mirror: feed it realistic, well-researched numbers, and it will show you a reliable financial forecast. But if you put in guesswork or overly optimistic figures for rents, refurb costs, or mortgage rates, that's exactly what it will spit back out.

The tool is only as good as the data you give it. Garbage in, garbage out.

Can't I Just Use a Spreadsheet Instead?

You absolutely can, but it's a bit like navigating with a hand-drawn map when GPS exists. Spreadsheets are incredibly prone to human error – one broken formula or a misplaced decimal can turn a terrible deal into a brilliant one on paper.

They're also a nightmare to keep updated with the UK's constantly shifting tax rules like Section 24. A purpose-built property investment calculator is designed to eliminate these risks, giving you consistent, reliable outputs every single time and saving you from costly mistakes born from a simple typo.

What's a "Good" ROI for UK Property, Anyway?

There's no single magic number. A "good" Return on Investment (ROI) depends entirely on your strategy, your tolerance for risk, and the specific location you're investing in.

For a standard, vanilla buy-to-let, many UK investors won't look twice at a deal unless the cash-on-cash ROI is heading towards 8% or more.

But for strategies that demand more hands-on management and carry more risk, the goalposts move significantly:

- HMOs (Houses in Multiple Occupation): Here, you're often aiming for an ROI in the 10-15% range to make the extra effort worthwhile.

- Serviced Accommodation (SA): This is more like running a hospitality business, so the targets are much higher, often 15-25% or even more.

Ultimately, the only person who can define a "good" ROI is you. Always measure a potential deal against your own financial goals and what other investments could offer for the same level of risk and effort.

Ready to analyse your next deal with speed and confidence? The DealSheet AI app replaces fragile spreadsheets with AI-powered analysis, automatically applying UK tax rules to give you a clear verdict in seconds. Download it on the App Store and start your free trial.