UK Buy To Let Investment Calculator: Your 2026 Guide To Smart Decisions

UK Buy To Let Investment Calculator: Your 2026 Guide To Smart Decisions

Making a confident buy-to-let decision in the UK market starts with mastering the numbers. A powerful buy-to-let investment calculator is your most essential tool, turning a complex web of financial data into clear, actionable insights like rental yield, ROI, and cash flow, which this guide will explore. To really speed this up, advanced tools like the DealSheet AI app automate the heavy lifting; you can just drop in a property listing to see instantly if a deal is truly worth pursuing. Download the DealSheet AI app here and analyse your first deal in seconds.

Your First Step To Smarter UK Property Investment

Navigating the UK's property market requires more than just a good eye for a promising street. Success hinges on rigorous financial analysis, and that's where a proper buy-to-let investment calculator becomes your best friend. Think of it as a flight simulator for your property venture; it lets you test how an investment will perform under real-world conditions before you put your capital on the line.

Its real job is to stress-test a potential deal against all the UK-specific costs and taxes, giving you a realistic forecast of its profitability instead of leaving you to rely on guesswork. This guide will walk you through every metric, helping you make data-driven decisions that build real wealth. For anyone just starting out, getting the fundamentals right is everything, and our guide on beginner property investment offers a solid foundation.

Why Guesswork Is So Dangerous

In the past, a simple back-of-the-envelope calculation comparing mortgage cost to rent might have been enough. Not anymore. The modern UK rental market is far more complex, with things like Section 24 mortgage interest relief restrictions and fluctuating Stamp Duty Land Tax (SDLT) rates that can turn a seemingly profitable deal into a financial drain. Relying on gut feeling is a recipe for disaster.

A proper calculator forces you to account for all the variables, both the obvious and the hidden:

- Upfront Costs: It's not just the deposit. You need to factor in legal fees, surveys, and the all-important SDLT.

- Ongoing Expenses: This is where deals often unravel. A good model includes landlord insurance, maintenance budgets, void periods, and agent fees.

- Tax Liabilities: Crucially, it must model the impact of income tax and specific property regulations that can sink your returns.

The Power of Instant Analysis

The real magic of a good calculator is speed and clarity. Instead of spending hours building a spreadsheet from scratch for every potential deal, you can analyse multiple properties in minutes. This is where modern tools give you a serious edge. For instance, the DealSheet AI app takes this a step further by automating the entire process from a simple property listing.

By inputting just a URL, the AI builds a complete financial model, instantly revealing key metrics. This speed is critical in a fast-moving market where the best deals don't wait around.

Ultimately, a buy-to-let investment calculator isn't just about the numbers; it's about confidence. It replaces the anxiety of the unknown with the assurance of solid data, letting you move forward on deals backed by proof, not just hope.

Key Metrics A Buy To Let Calculator Reveals

A comprehensive calculator does more than just add and subtract; it reveals the true financial health of a potential investment. Below is a quick summary of the essential outputs and why they are so critical for making a smart decision in the UK market.

| Metric | What It Tells You | Why It's Critical For Your Decision |

|---|---|---|

| Gross & Net Yield | The headline return vs. the return after operating costs. | Gross yield is for quick filtering, but Net yield reveals the deal's real profitability before finance and tax. |

| Cash Flow | The actual money left in your pocket each month after all costs, including your mortgage. | This is the ultimate test. Positive cash flow means the property pays for itself; negative means you're subsidising it. |

| Return on Investment (ROI) | The annual profit as a percentage of the actual cash you've invested (deposit, fees, etc.). | This is the most important metric. It shows how hard your own money is working for you, allowing you to compare property against other investments. |

| Internal Rate of Return (IRR) | A more advanced metric that accounts for capital growth and the time value of money over the long term. | IRR gives you a complete picture of the investment's total return over its entire lifecycle, not just a single year. |

Understanding these metrics moves you from being a hopeful amateur to a strategic investor. They provide the clear, unbiased data you need to reject bad deals quickly and move on good ones with conviction.

Gathering The Right Numbers For Your Calculator

The old saying "garbage in, garbage out" has never been more true than for a buy-to-let investment calculator. The quality of its answers depends entirely on the quality of the numbers you feed it. To get beyond a vague guess and build a financial forecast you can actually rely on, you need to gather a specific set of numbers covering every part of your UK property deal.

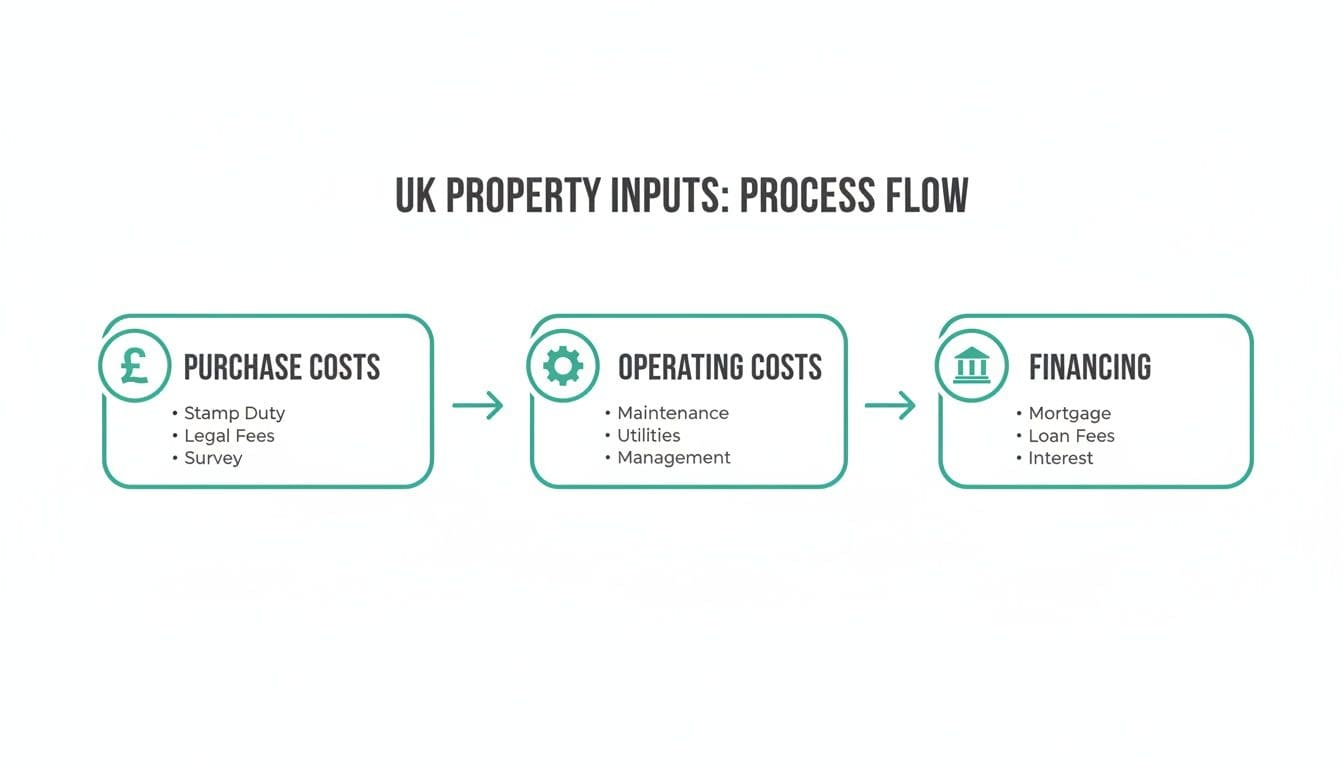

This starts with the obvious stuff, like the purchase price and your deposit. But honestly, that's just the tip of the iceberg. A proper analysis means digging much deeper into both the one-off costs to get the keys and all the ongoing expenses that will hit your bank account month after month.

Essential Upfront Purchase Costs

Before you even own the property, a handful of significant costs will inflate your total initial investment. Getting these wrong can lead to a nasty surprise and put you on the back foot from day one.

Your calculator will need inputs for:

- Stamp Duty Land Tax (SDLT): This is often the biggest upfront cost after the deposit itself. As an investor buying an additional property in the UK, you'll be on the hook for a higher rate. The exact amount depends on the property's price and your own situation, so using a dedicated tool is a must. You can learn more about this in our complete guide to the Stamp Duty Land Tax calculator.

- Legal and Conveyancing Fees: These are the fees you pay the solicitor to handle all the legal paperwork and transfer ownership. You should budget between £850 and £1,500, though this can creep up for more complicated purchases.

- Survey Costs: A property survey is your best defence against hidden structural problems. The lender's basic valuation is for their benefit, not yours. A more detailed HomeBuyer Report or a full Building Survey is a smart investment for your own peace of mind, costing anywhere from £400 to over £1,000.

- Mortgage Arrangement Fees: Lenders often charge a fee just for setting up the loan. Sometimes you can add this to the mortgage balance, but paying it upfront means you start with less debt.

Accounting For Ongoing Operational Expenses

Once the property is yours, your attention has to shift to the recurring costs that directly impact your monthly cash flow. This is where so many new landlords trip up, underestimating the little things that quickly eat into profits. A good buy-to-let investment calculator will force you to account for all of them.

Underestimating your running costs by just 5% can be the difference between a profitable investment and one that costs you money each month. Precision here is non-negotiable for an accurate forecast.

Key ongoing costs include:

- Landlord Insurance: This isn't the same as standard home insurance. It's essential for protecting your asset and covering your liabilities as a landlord.

- Maintenance and Repairs: A solid rule of thumb is to set aside 1% of the property's value every year for maintenance. For a £250,000 house, that's £2,500 a year, or about £208 per month.

- Letting Agent Fees: If you're not self-managing, agent fees for finding tenants or full management typically run from 8% to 15% of the monthly rent.

- Void Periods: It's completely unrealistic to assume your property will be occupied 100% of the time. To be safe, always budget for at least one month of vacancy per year.

- Service Charges and Ground Rent: If you're buying a leasehold property like a flat, these are mandatory annual fees that absolutely must be factored into your sums.

The Impact Of UK Tax Rules

Finally, no UK property analysis is worth its salt without considering tax—specifically, the Section 24 mortgage interest relief restrictions. If you're a landlord investing in your personal name (not through a limited company), you can no longer deduct your full mortgage interest from your rental income before calculating your tax bill. Instead, you just get a basic rate (20%) tax credit on your interest payments.

This rule change artificially inflates your taxable income. For many, it's enough to push them into a higher tax bracket, which can dramatically increase their tax liability. Any effective buy-to-let investment calculator must apply this rule correctly to show you a true picture of your post-tax profit, as it can single-handedly kill an otherwise decent-looking deal.

Translating Your Data Into Actionable Insights

So, you've gathered all your numbers. Now for the magic trick: turning that raw data into something that actually tells you whether a deal is a potential goldmine or just another money pit. This is precisely what a buy-to-let investment calculator is for. It takes your inputs—the purchase price, running costs, and mortgage details—and translates them into the language of property investment: Key Performance Indicators (KPIs).

This isn't about one single, magic number. It's a process, where each calculation builds on the last, giving you a progressively clearer picture of the deal's real-world profitability. Getting this right is what separates a confident, informed decision from a hopeful punt.

Before we dive into the outputs, it's crucial to understand the inputs. Every cost falls into one of three buckets: what it takes to buy it, what it takes to run it, and what it takes to finance it.

Get these three pillars right, and your forecast will be solid. Get them wrong, and your returns will be pure fiction.

Gross Yield: The Starting Point

The first metric any calculator spits out is the Gross Yield. Think of it as a quick, back-of-the-envelope check to compare different properties at a glance.

- How it's calculated: (Annual Rental Income / Property Purchase Price) x 100

Let's say you're looking at a property for £250,000 that could rent for £1,500 a month (£18,000 a year). The Gross Yield is a tidy 7.2%. This figure is great for an initial sift. The national average gross yield in the UK has been climbing, sitting at 6.15% in late 2023, making yields above this level particularly attractive for investors.

But—and this is a big but—Gross Yield is a deeply flawed metric on its own. It completely ignores every single running cost. A deal with a stunning gross yield can be secretly torpedoed by sky-high service charges or constant maintenance, which is why we have to dig deeper.

Net Yield: A More Realistic Picture

This is where things get more interesting. Net Yield peels back the first layer of optimism by factoring in all those operational costs we talked about—insurance, voids, management fees, and repairs.

- How it's calculated: (Annual Rental Income - Annual Operating Costs) / Property Purchase Price x 100

Stick with our £250,000 property. If you estimate your annual operating costs will be around £3,000, the Net Yield drops to 6.0%. It's a much more sober and realistic indicator of the property's underlying performance before you even think about the mortgage or tax. If you want to get into the nitty-gritty of this, our guide on how to calculate property yield breaks it down further.

Return On Investment: The Metric That Truly Matters

While Net Yield is a vital health check, the number that should really grab your attention is Return on Investment (ROI). Sometimes called 'Cash on Cash Return', this KPI tells you how hard your own cash is working for you.

ROI doesn't care about the property's total value. It focuses only on the money you've personally pulled out of your bank account—your deposit plus all the upfront fees—and measures it against the annual pre-tax profit the property kicks out. This is the ultimate measure of your capital's efficiency.

Let's put some numbers on it, using our ongoing example:

- Total Cash Invested: A 25% deposit of £62,500, plus £8,000 for Stamp Duty and legal fees, comes to £70,500.

- Annual Pre-Tax Profit: That's £18,000 in rent, minus £3,000 in running costs, and minus £9,375 in mortgage interest. Your profit is £5,625.

- The ROI Calculation: (£5,625 / £70,500) x 100 = 7.98%

This tells you that for every pound you've personally invested, you're getting just under 8p back each year before tax. This is the figure you should be comparing to other investment opportunities, whether it's stocks, shares, or another property deal.

Monthly Cash Flow And The Section 24 Impact

Finally, any calculator worth its salt has to show you the Net Monthly Cash Flow after tax. This is the money that actually hits your bank account. And in the UK, this is where your ownership structure—holding it in your personal name versus a limited company—becomes absolutely critical because of Section 24.

Let's assume our investor is a higher-rate taxpayer (40%). The difference is stark.

- As an Individual Landlord: Your tax bill is calculated on an artificially inflated income. The £9,375 in mortgage interest cannot be deducted as an expense. You only get a basic-rate tax credit to soften the blow, which often isn't enough. The result? A much smaller post-tax profit.

- As a Limited Company: The full £9,375 in mortgage interest is treated as a legitimate business expense. Corporation Tax is then paid on the much lower, true profit.

A powerful calculator will model both scenarios for you. It will lay out in black and white how holding the property in a limited company structure could dramatically improve your net profit and monthly cash flow. For many investors, seeing this side-by-side comparison is the final piece of the puzzle that decides whether a deal gets the green light or goes in the bin.

Moving Beyond Basic Spreadsheets

Free online tools and basic spreadsheets are a decent starting point for a quick glance at a property deal. But for any serious UK investor aiming to build a profitable portfolio in 2026, relying on them is like trying to navigate London with a map from the 1990s—you'll miss every crucial detail that actually determines success.

The truth is, a sophisticated buy to let investment calculator built into a modern app isn't just a minor upgrade. It's a completely different way of working.

The single biggest danger with manual spreadsheets is human error. A single misplaced formula or an incorrect Stamp Duty figure can cascade through your entire analysis, turning a confident projection into a dangerous work of fiction. This risk gets much worse when you're analysing multiple deals under pressure.

The Pitfalls Of Manual Analysis

Building your own spreadsheet from scratch is incredibly time-consuming and riddled with risk. You have to manually find, input, and constantly update every variable, from local council tax rates to the latest mortgage products. For any active investor, this creates a few huge problems.

- Inconsistent Analysis: Every spreadsheet you build might be slightly different. This makes it almost impossible to compare properties on a true like-for-like basis.

- Time Drain: Manually keying in data from a property listing on Rightmove or Zoopla eats up a shocking amount of time, slowing down your ability to vet opportunities and move quickly.

- Hidden Formula Errors: A broken cell reference or a dodgy tax calculation can go unnoticed for weeks, leading you to chase deals that are fundamentally broken from the start.

The Rise Of Automated Underwriting

This is where modern property analysis apps like DealSheet AI completely change the game. Instead of you manually typing everything in, these tools use AI to automatically pull key information straight from a property listing URL. This doesn't just save you hours of tedious work; it ensures accuracy and consistency across every deal you look at.

The UK is home to 2.82 million private landlords who collectively manage a staggering £1.6 trillion in property assets. In a market of this scale, speed and accuracy aren't just nice-to-haves; they are essential for competing effectively.

A dedicated property investment app isn't just a calculator; it's a complete analysis system. It replaces fragile, error-prone spreadsheets with a reliable, repeatable process that produces trustworthy numbers, every single time.

To help illustrate the difference, let's compare the old way with the new.

Spreadsheets Vs DealSheet AI: A Comparison For UK Investors

| Feature | Manual Spreadsheet | DealSheet AI App |

|---|---|---|

| Data Entry | Fully manual; time-consuming and error-prone. | Automated from property listings (e.g., Rightmove, Zoopla). |

| Accuracy | High risk of hidden formula errors and incorrect tax logic. | UK-specific calculations are built-in and validated. |

| Consistency | Varies from deal to deal, making comparisons difficult. | Standardised analysis ensures true like-for-like evaluation. |

| Complex Deals | Struggles with HMOs, BRRRR, and SA without complex custom builds. | Pre-built, dedicated models for advanced UK strategies. |

| Stress Testing | Possible, but requires manual changes and complex formulas. | Instant sensitivity analysis for rates, voids, and rent changes. |

| Speed | Slow; can take 15-30 minutes per deal for detailed analysis. | Fast; initial analysis can be done in under 60 seconds. |

As you can see, while a spreadsheet offers flexibility, it comes at the cost of reliability and speed—two things a professional investor can't afford to sacrifice.

Built For Complex UK Strategies

A standard spreadsheet really struggles with anything more complicated than a vanilla buy-to-let. If you're exploring strategies like Houses in Multiple Occupation (HMOs) or the popular Buy, Refurbish, Refinance, Rent (BRRRR) model, a simple calculator is completely useless.

You need a tool with built-in templates designed specifically for these strategies. Advanced apps provide pre-configured models for:

- HMOs: Handling multiple income streams, higher running costs, and specific licensing fees.

- BRRRR: Modelling the distinct financial phases for the purchase, the renovation, and the crucial refinancing step based on the property's new, higher value.

- Serviced Accommodation: Factoring in fluctuating nightly rates, higher utility bills, cleaning costs, and seasonality.

Trying to build these complex models yourself in a spreadsheet is a recipe for disaster. To get a better sense of the specific variables involved, check out our guide on how to evaluate HMOs, Serviced Accommodation, and BRRRR deals without the spreadsheet headache.

Stress-Testing Your Investment

Perhaps the most critical feature missing from basic tools is the ability to perform sensitivity analysis. A deal that looks fantastic on paper can quickly turn sour if interest rates rise or you face a long void period.

A professional-grade buy to let investment calculator lets you stress-test your numbers to reveal these hidden risks. You can instantly model scenarios like:

- What happens to my cash flow if the Bank of England base rate increases by 1%?

- Can the investment survive a three-month void period between tenants?

- How does a 10% drop in rental income affect my overall ROI?

This ability to see how your returns react to changing market conditions is what separates amateur guesswork from professional risk management. It gives you the foresight to build resilience into your portfolio, ensuring your investments can weather the inevitable economic storms ahead.

Forecasting Your Long-Term Wealth Creation

Cash flow is the lifeblood of any buy-to-let, no question. It keeps the lights on. But true, generational wealth is rarely built on monthly income alone—it's built over the long haul through capital appreciation.

A basic buy-to-let investment calculator is great for checking if a deal will wash its face year-to-year. A professional-grade tool, however, lets you zoom out and see the bigger picture over 5, 10, or even 25 years. This is how you stop thinking like a landlord and start acting like a strategic portfolio builder.

This long-term view means looking beyond the rent and factoring in sensible property price growth. Even a modest annual lift in a property's value can have a massive impact on your total returns, especially when you remember you're using the bank's money (leverage) to do it. It's this powerful combination of rental profit and capital growth that makes UK property such a compelling asset.

Using Credible Growth Forecasts

Trying to guess future house prices is a fool's game. Your analysis should be grounded in credible, data-backed forecasts from sources that do this for a living. Major UK property consultancies and lenders publish five-year forecasts all the time, based on hard economic data, supply-and-demand trends, and where they see interest rates heading.

For instance, looking out towards 2026 and beyond, some analysts see serious growth on the horizon. Savills, for example, has forecasted that UK house prices will grow by an average of 21.6% over the five years from 2025. Projections like this, often rooted in the UK's chronic undersupply of housing, are exactly why a sophisticated calculator is essential. You can find more on the market dynamics in this insightful property market analysis.

By plugging these expert forecasts into an advanced tool, you're not just guessing anymore. You're modelling how your investment could realistically perform, turning abstract predictions into concrete numbers that actually inform your strategy. This is a core part of what we cover in our guide to portfolio-level thinking for landlords.

Introducing The Internal Rate Of Return

To really get a grip on long-term performance, you need a metric that accounts for every pound in and every pound out over the entire life of the investment—including the day you eventually sell it. This is exactly what the Internal Rate of Return (IRR) does.

IRR is a far more holistic and powerful metric than a simple ROI. It calculates the annualised rate of return by considering all cash flows—your initial deposit, the ongoing net income, and the final profit from selling up—while also factoring in the time value of money.

Put simply, it tells you the true, all-in annual return on your investment from start to finish. A higher IRR means a more profitable venture over its complete lifecycle.

Modelling Scenarios With Advanced Tools

This is where a dedicated tool like the DealSheet AI app really shows its worth compared to a clunky spreadsheet. It allows you to model different growth scenarios with just a few taps, giving you a clear vision of your potential future net worth.

You can instantly see the impact of various outcomes:

- Conservative Growth: What happens if the market is sluggish, with below-average house price inflation?

- Target Growth: Let's use that credible forecast from Savills or Knight Frank and see what that looks like.

- Optimistic Growth: What would my returns be in a proper bull market?

This kind of sensitivity analysis is invaluable. It helps you understand the full spectrum of possibilities and build a strategy that's robust enough to handle whatever the market throws at it. By visualising the long-term impact of capital growth on your equity, you can make decisions that build real, lasting wealth.

Your Buy-To-Let Calculator Questions Answered

Even with a solid tool, property investing in the UK throws up a lot of questions. Getting the most out of a buy-to-let investment calculator isn't just about plugging in numbers; it's about understanding the story those numbers tell. This final section tackles the most common questions investors ask, giving you clear, direct answers so you can analyse deals with total confidence.

Think of this as the FAQ for interpreting your results. Whether you're stuck on a specific metric or wondering how to model a more creative strategy, this is the clarity you need to move forward.

What Is The Most Important Metric From A Buy-To-Let Calculator?

Most people start with Gross Yield for a quick comparison, but the single most important metric for most UK investors is the final Net Monthly Cash Flow. This is the bottom line. It's the actual money left in your bank account each month after every single cost—from the mortgage to the last penny of insurance—has been paid.

A very close second is Return on Investment (ROI), often called 'Cash on Cash Return'. This number is vital because it tells you how hard your own invested cash is working. A property with a slightly lower yield but needing far less of your own money to buy could have a much better ROI, making it the smarter investment. Your personal strategy dictates which one you obsess over.

If you're building a portfolio for passive income, monthly cash flow is king. If you're trying to grow a portfolio quickly by recycling your capital, ROI is the metric that matters most.

How Does A Calculator Handle Section 24 Tax Rules?

A proper, UK-specific calculator handles the dreaded Section 24 rules by treating mortgage interest completely differently depending on the ownership structure. For individual landlords versus those using a limited company, this distinction is non-negotiable for an accurate forecast.

Here's how a serious tool gets it right:

- For an Individual Landlord: It calculates your income tax based on gross rental income (minus operating costs, but crucially, not minus mortgage interest). It then applies a 20% tax credit for the mortgage interest against your final tax bill. This correctly models how Section 24 artificially inflates your taxable income.

- For a Limited Company: It does what makes logical sense—it deducts the full mortgage interest as a legitimate business expense before calculating the profit that's subject to Corporation Tax.

This is a massive headache to model in a spreadsheet. Advanced tools like the DealSheet AI app automate this, letting you toggle between personal and limited company structures to see which is more profitable in seconds.

How Can I Accurately Estimate Repair Costs?

Estimating future repairs is more art than science, but there are reliable methods to stop you from getting caught out. A good buy-to-let investment calculator will let you model this in a few different ways.

A widely used rule of thumb is the '1% Rule'. It's simple: budget 1% of the property's purchase price for annual maintenance.

- Example: For a property bought for £250,000, you'd set aside £2,500 per year, which is about £208 per month.

Another popular approach is to earmark between 5% and 10% of the monthly rent purely for maintenance. Which method you use depends on the property's age and condition. A brand-new build might sit at the low end of that range, but an older Victorian terrace will almost certainly need a bigger pot. The key is to be realistic and, if in doubt, conservative.

Can I Use A Calculator For HMO Or BRRRR Strategies?

Yes, but you absolutely must use a calculator specifically designed for them. Trying to shoehorn a complex strategy into a standard, vanilla buy-to-let investment calculator is a recipe for disaster. The numbers will be dangerously wrong.

These strategies have unique financial levers a basic tool just can't pull:

- For an HMO (House in Multiple Occupation): The calculator needs to handle multiple income streams (rent per room) and the much higher running costs for things like utilities, council tax, and more hands-on management.

- For a BRRRR (Buy, Refurbish, Refinance, Rent): The tool has to model the deal in distinct phases. It needs to track the initial purchase and refurb costs, then calculate a new mortgage based on the property's uplifted value, and finally project the ongoing rental cash flow.

This is exactly where specialised apps prove their worth. Tools like DealSheet AI have dedicated, pre-built models for these strategies, making sure all the unique costs, financing structures, and revenue streams are baked into the analysis from the start.

Ready to stop wrestling with basic spreadsheets and start analysing UK property deals with professional speed and accuracy? The DealSheet AI app replaces guesswork with data-driven confidence. Analyse any deal in under 60 seconds, stress-test your assumptions, and make smarter investment decisions.

Download DealSheet AI from the App Store and start your free trial today.