Maximise Your UK Property Returns With Our Buy To Let Yield Calculator Guide for 2026

Maximise Your UK Property Returns With Our Buy To Let Yield Calculator Guide for 2026

Before you even think about putting an offer on a UK property, you need to run the numbers. The headline metric everyone talks about is rental yield, but a basic buy to let yield calculator can be dangerously misleading if you don't understand what it's really telling you. This guide provides the answer by breaking down the essential formulas for gross yield, net yield, and ROI, ensuring you can accurately assess any deal. For investors who need to analyse properties in seconds, the DealSheet AI app automates this entire process, instantly calculating yields, cash flow, and tax implications straight from a property listing.

Your Guide to Property Investment Calculations

Getting into UK property investment is about more than just finding a promising house on a nice street. It's about mastering the numbers that actually drive your returns. Too many new investors get fixated on the purchase price and the potential monthly rent, completely overlooking the web of hidden costs that will eat into their profits.

Relying on a simple buy to let yield calculator without understanding the crucial difference between gross and net figures is one of the most common pitfalls out there. This guide is here to demystify these essential calculations once and for all. We'll break down the formulas you need, explain why a property's advertised potential and its real-world performance are two very different things, and give you the tools to assess any deal with genuine confidence.

Why Accurate Calculations Matter

In the competitive UK property market of 2026, the margin for error has shrunk. A small miscalculation can be the difference between a high-performing asset that generates consistent cash flow and a financial millstone that drains your bank account month after month. Getting these metrics right isn't just a "nice to have"—it's non-negotiable.

Here's why you absolutely have to master the maths:

- It sets realistic expectations. Good analysis helps you see past the sales pitch and understand what your actual monthly and annual return will look like after all the bills are paid.

- It lets you compare apples with apples. You can accurately stack different properties up against each other, ensuring you pick the one with the best genuine potential, not just the one with the flashiest brochure.

- It's essential for securing finance. Lenders want to see robust financial projections. When you can present detailed yield and cash flow analysis, it proves you're a serious, well-prepared investor they can trust.

- It underpins your entire strategy. Knowing your numbers inside-out allows for much better long-term planning, like setting up a sinking fund for major repairs or spotting opportunities to boost your returns.

For anyone just starting out, getting a firm grip on these fundamentals is the first real step towards building a successful portfolio. A solid foundation in analysis is what prevents those costly early mistakes and sets you on a path to sustainable growth.

This article will give you the knowledge you need to use any buy to let yield calculator effectively. Before we dive into the formulas, our guide on property investment for beginners in the UK provides some excellent foundational context.

We'll kick things off by defining the most common—and most frequently misunderstood—metric you'll encounter: gross yield.

Understanding Gross Yield: Your Starting Point

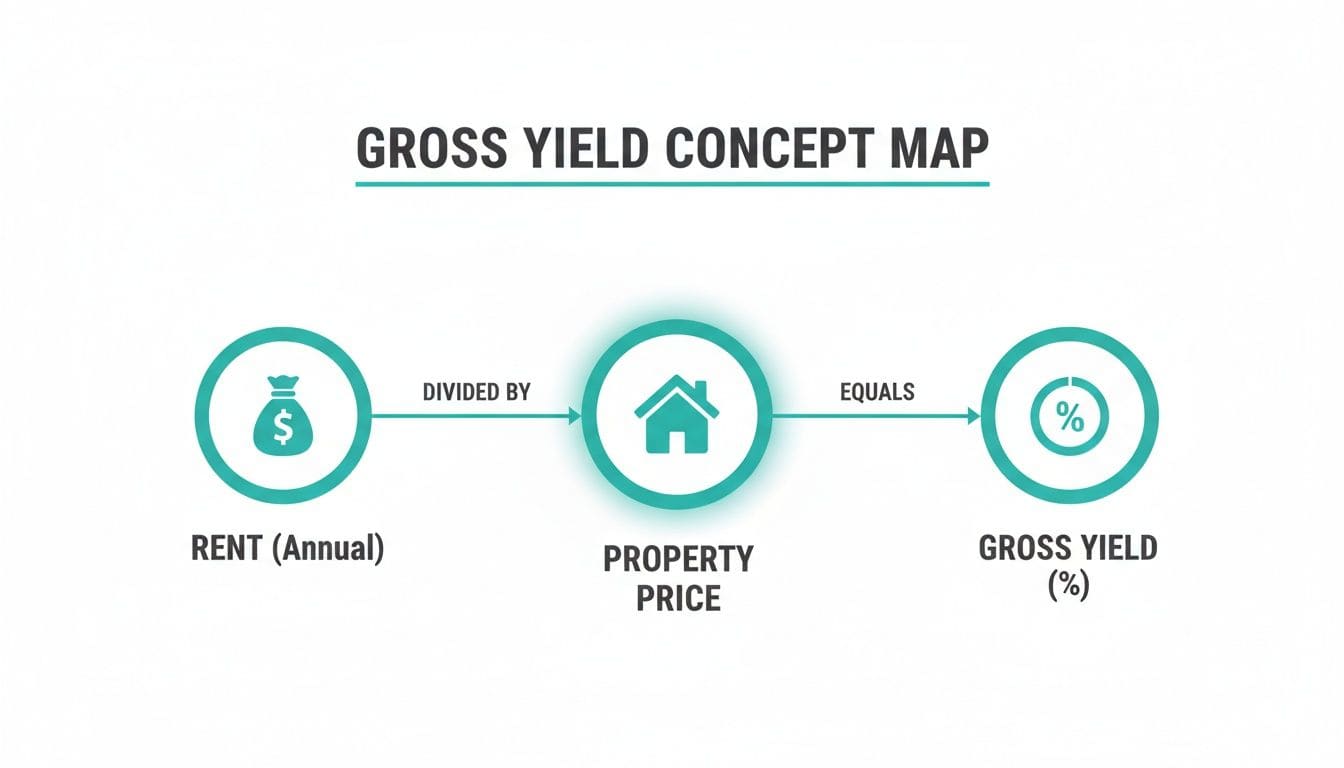

Gross yield is the first metric every property investor bumps into. It's the headline figure you'll see plastered over property listings, and for good reason: it gives a quick, high-level snapshot of a deal's income potential relative to its price.

Think of it like a company's total revenue before any costs are taken out. It's an essential starting point, but it never, ever tells the whole financial story.

Using a buy to let yield calculator for gross yield is perfect for one thing: creating an initial shortlist. It lets you quickly weed out properties that don't meet a basic income threshold, saving you from wasting hours doing a deep dive on deals that were never going to work.

The Gross Yield Formula Explained

The calculation for gross yield is beautifully simple, which is why it's used so often for those first back-of-the-envelope comparisons. It completely ignores all the running costs and just looks at the relationship between the rent and the property's price.

The formula is dead easy:

(Annual Rental Income / Property Purchase Price) x 100 = Gross Yield %

This basic calculation gives you a clean percentage you can use to compare different properties at a glance. For a deeper look at the mechanics, you can calculate rental yield in the UK with our detailed guide.

A Real-World UK Example

Let's put this into practice with a real UK example. Imagine you're looking at a two-bedroom terraced house up in Newcastle upon Tyne.

- Purchase Price: £180,000

- Monthly Rent: £950

First, we need to work out the annual rental income: £950 (monthly rent) x 12 (months) = £11,400 (annual rent)

Now, we just plug those numbers into the gross yield formula: (£11,400 / £180,000) x 100 = 6.33% Gross Yield

This figure is genuinely useful for spotting areas with strong rents relative to property prices. For instance, recent data showed the North East of England had the UK's highest average gross rental yield. This blew London's average out of the water, where sky-high property prices hammer down returns. You can dig into these regional rental yield findings on Statista.

The DealSheet AI app makes these key metrics easy to see, so you can understand a property's headline potential in seconds.

As the screenshot shows, this is the first number you see—the foundation for the much deeper financial analysis that has to follow.

The Limitations of Gross Yield

While its simplicity is a strength, it's also its biggest weakness. The gross yield calculation pretends that the unavoidable costs of owning a rental property in the UK simply don't exist.

Gross yield is an optimist's metric. It shows you the best-case scenario before reality kicks in. True profitability is only revealed once you subtract the inevitable expenses.

These costs are everything from mortgage interest and letting agent fees to maintenance, voids, and insurance. As we're about to see, these expenses can dramatically slash your actual return. This is precisely why relying only on a gross buy to let yield calculator can lead to disastrous investment decisions. It's a great filtering tool, but it should never be the final word.

Calculating Net Yield to Find True Profitability

If gross yield shows you the optimistic, brochure-version of a deal, net yield gives you the grounded reality. This is the metric that separates hopeful speculators from serious investors, because it reveals your actual return after all the real-world costs are stripped out.

Frankly, any buy to let yield calculator that only shows the gross figure is hiding the most important part of the story.

Net yield answers the one question that really matters: "After paying for everything, what profit does this property actually generate?" This figure is what determines whether an investment will build your wealth or just become an expensive hobby.

The basic gross yield calculation is a simple starting point, as this graphic shows. It's the foundation we're about to build on.

Now, let's get real and introduce the costs that define your actual profitability.

The Net Yield Formula Unpacked

The formula for net yield is more involved because it has to account for the unavoidable costs of being a landlord in the UK. Getting this right is everything.

The formula is: ((Annual Rental Income - Annual Operating Costs) / Total Investment Cost) x 100

It looks similar to the gross calculation, but two new ingredients completely change the flavour: Annual Operating Costs and Total Investment Cost. Nail these, and you'll be able to use any buy to let yield calculator with confidence.

Defining Your Annual Operating Costs

'Annual Operating Costs' are all the recurring expenses you'll pay just to keep the property running and legally let. These aren't optional extras; they are the cost of doing business and they will hit your bank account.

A typical list for a UK landlord in 2026 would include things like:

- Letting Agent Fees: If you use an agent for finding tenants or full management, expect to pay between 10% and 15% of the monthly rent.

- Landlord Insurance: Absolutely essential for protecting the building and covering your liability. It's a non-negotiable annual expense.

- Safety Certificates: You're legally on the hook for valid Gas Safety (CP12), Electrical Installation Condition Report (EICR), and Energy Performance Certificate (EPC) documents.

- Maintenance and Repairs: A solid rule of thumb is to budget 1% of the property's value each year for things that break. For our Newcastle example, that's around £1,800.

- Service Charges and Ground Rent: If you're buying a leasehold flat, these fees for communal upkeep are unavoidable.

Calculating Your Total Investment Cost

The second critical tweak is switching from 'Purchase Price' to 'Total Investment Cost'. This number represents every single pound you had to spend to get the keys and make the property ready for tenants, not just the price on the sales agreement.

Your Total Investment Cost is the true financial barrier to entry. It's the property price plus all the upfront fees, taxes, and fix-up costs needed to get the property tenant-ready.

This includes:

- Purchase Price: The price you agreed to pay for the property itself.

- Stamp Duty Land Tax (SDLT): A major tax on property purchases in England and Northern Ireland, which includes a 3% surcharge for any additional properties.

- Solicitor and Legal Fees: The cost for all the conveyancing work.

- Initial Refurbishment Costs: Any money spent on a fresh coat of paint, new carpets, or repairs needed before a tenant can even think about moving in.

A Worked UK Example From Gross to Net

Let's go back to our £180,000 house in Newcastle. It had a promising 6.3% gross yield, but what happens when we apply the net yield formula? Let's see the real return.

Total Investment Cost:

- Purchase Price: £180,000

- SDLT (including 3% surcharge): £6,500

- Solicitor Fees: £1,500

- Initial Refurbishment: £3,000

- Total Investment Cost = £191,000

Annual Operating Costs:

- Letting Agent Fees (12% of £11,400 rent): £1,368

- Insurance: £300

- Safety Certificates & Maintenance Budget: £1,800

- Total Annual Costs = £3,468

Now, let's plug those numbers into the net yield formula: ((£11,400 - £3,468) / £191,000) x 100 = 4.15% Net Yield

And just like that, the appealing 6.3% has dropped to a much more sober 4.15%. This is exactly why you must calculate net yield. It gives you the unvarnished truth about how your investment is really performing.

Factoring in Mortgage Costs and UK Taxes

Once you move past net yield, you start hitting the two forces that really shape a UK investor's returns: financing and taxes. For most of us, a mortgage is what gets the deal done, so its costs have to be accounted for with precision. At the same time, UK tax rules—especially Section 24—can completely change your final profit.

These aren't optional extras in your calculations; they are the absolute core of any realistic financial forecast. A simple buy to let yield calculator that ignores them is painting a dangerously incomplete picture of your investment's health. Learning how to model these factors is what separates a sustainable portfolio from a financial headache waiting to happen.

The Impact of Section 24 on Your Profit

Section 24, sometimes nicknamed the "tenant tax," fundamentally changed the game for individual landlords in the UK. Before it came in, you could deduct your entire mortgage interest from your rental income before calculating your tax bill, just like any other business expense. Simple.

That's no longer the case. Now, individual landlords must declare all their rental income, pay tax on the lot, and only then get a basic rate tax credit of 20% on their mortgage interest costs.

This change hits higher-rate (40%) and additional-rate (45%) taxpayers the hardest. They pay tax on their income at their higher personal rate but only get tax relief at the basic 20% rate. It can even push some basic-rate taxpayers into the higher bracket, a nasty effect known as "fiscal drag" that can slash their actual take-home profit.

Mitigating Section 24 with a Limited Company

One of the most common ways to deal with Section 24 is to buy and hold property inside a limited company, often called a Special Purpose Vehicle (SPV).

When you operate through a limited company, the Section 24 rules don't apply. This means you can treat mortgage interest as a full-blown business expense again, deducting the entire interest cost from your rental income before your Corporation Tax bill is worked out.

But going down the limited company route isn't a silver bullet. You need to weigh up a few things:

- Different Mortgage Rates: Lenders often charge higher interest rates and chunkier fees for limited company mortgages compared to personal buy-to-let deals.

- Additional Admin: Running a company means more paperwork. You'll be filing annual accounts and confirmation statements with Companies House, which adds time and cost.

- Extracting Profits: Getting your money out of the company isn't as simple as taking it from your bank account. Drawing profits as dividends is subject to its own personal tax rules, which requires careful planning.

Planning for Voids and Capital Expenditures

Beyond financing and tax, a truly solid financial model has to account for the inevitable bumps in the road. Even the best properties will have empty periods or need a major repair at some point.

Void periods are the times when the property is empty between tenancies, bringing in zero income. A sensible, conservative approach is to assume one month of voids per year. That means you calculate your income based on 11 months of rent, not 12.

Just as important are capital expenditures—those big, infrequent costs like a new boiler, a roof repair, or a kitchen refresh. These can wipe out months of profit in one go if you haven't planned for them. This is where a 'sinking fund' becomes your best friend.

The Importance of a Sinking Fund

A sinking fund is really just a dedicated savings pot for covering those major future repairs. By putting aside a small slice of the rent each month (say, 5-10%), you build a financial buffer. It's what ensures you can handle a £3,000 boiler replacement in 2026 without derailing your investment or having to find the cash overnight.

For investors with larger portfolios, modelling these variables accurately is non-negotiable. For example, experienced landlords managing 10-50 units find that advanced tools give them game-changing stress-testing capabilities. They can analyse multiple deals, apply real finance terms (with average buy-to-let rates hovering around 4.87%), and instantly see where profits get eaten up by that Section 24 tax cliff.

And don't forget, big upfront costs like Stamp Duty Land Tax are a huge part of your initial calculation. For a detailed breakdown, our comprehensive Stamp Duty Land Tax calculator guide will make sure your starting figures are spot on. A robust buy to let yield calculator has to account for every single one of these pressures to give you a forecast you can actually trust.

Moving Beyond Yield to ROI and Cash Flow

While net yield gives you a far more honest picture of a property's performance than its gross cousin, it isn't the final word. The sharpest investors I know focus on two even better metrics that cut right to the chase: Return on Investment (ROI) and Cash Flow.

Think of it this way: using a buy to let yield calculator to find the net yield is crucial, but it doesn't answer the most important question for any investor using a mortgage: "How hard is my actual cash working for me?"

This is where ROI comes in. It measures your return not against the property's total value, but against the real money you've had to pull out of your own pocket.

Understanding Return On Investment

ROI is a game-changer because it zeroes in on the efficiency of your invested capital. For anyone using a mortgage, this calculation is non-negotiable. It's the metric that truly reveals the power of leverage, showing how a fairly modest net yield can translate into a fantastic return on your cash.

The formula itself is pretty straightforward:

(Annual Pre-Tax Cash Flow / Total Cash Invested) x 100

Let's quickly break down those two key components:

- Total Cash Invested: This is the sum of every penny you spend upfront. It includes your mortgage deposit, Stamp Duty Land Tax (SDLT), solicitor fees, broker fees, and any cash you spend on an initial refurbishment. It's your total "skin in the game."

- Annual Pre-Tax Cash Flow: This is your net rental income after you've also paid your monthly mortgage costs. It's the profit left sitting in the bank before you have to worry about the tax man.

From a 4% Yield to a 12% ROI: A UK Example

Let's go back to our £180,000 Newcastle property, which we already worked out had a 4.15% net yield. Now, let's see what its ROI looks like with a typical 75% loan-to-value (LTV) mortgage.

First, we need to calculate the Total Cash Invested:

- Mortgage Deposit (25% of £180,000): £45,000

- SDLT: £6,500

- Solicitor Fees: £1,500

- Initial Refurbishment: £3,000

- Total Cash Invested = £56,000

Next, we calculate the Annual Pre-Tax Cash Flow:

- Annual Rental Income: £11,400

- Annual Operating Costs (agent fees, insurance, etc.): £3,468

- Annual Mortgage Payments (assuming a £135k mortgage at 5% interest-only): £6,750

- Annual Pre-Tax Cash Flow = £11,400 - £3,468 - £6,750 = £1,182

Now, we can plug those numbers into the ROI formula:

(£1,182 / £56,000) x 100 = 2.1% ROI

That's a much lower figure, and it perfectly demonstrates how sensitive your returns are to mortgage rates. If the rate was lower, say 3.5%, the annual payments would drop to £4,725. Suddenly, the ROI jumps to an impressive 5.8%. This sensitivity is exactly why tracking ROI is essential for any leveraged investment.

Your initial refurbishment budget also heavily influences these figures. For more detailed insights on budgeting accurately, understanding the typical building costs per square metre can be a huge help.

Yield vs ROI vs Cash Flow Explained

It's easy to get these terms mixed up, but they each tell a different part of the story. Understanding all three is what separates amateur landlords from professional investors.

| Metric | What It Measures | Key Question It Answers |

|---|---|---|

| Net Yield | The property's unleveraged profitability | "How profitable is the asset itself, ignoring my mortgage?" |

| ROI | The efficiency of your invested cash | "How hard is my own money working for me?" |

| Cash Flow | The monthly surplus or deficit | "Does this property pay for itself and put money in my pocket?" |

Ultimately, a good investment needs to perform well across all three metrics. A high yield is meaningless if bad financing leads to negative cash flow and a poor ROI.

Why Monthly Cash Flow Is King

While ROI gives you a brilliant annual performance metric, monthly cash flow is the absolute lifeblood of your investment portfolio.

It's the money left in your bank account each month after the rent has landed and every single bill—including the mortgage—has been paid. Simple as that.

A positive cash flow means the investment is self-sustaining and actively putting money in your pocket. A negative cash flow means you are topping it up from your own funds each month just to keep it afloat—an unsustainable position for almost every investor.

Tracking this monthly figure is critical for your financial stability. It determines whether your buy-to-let is a genuine asset that supports you or a liability that drains you. For any deal you analyse in 2026, your buy to let yield calculator must ultimately prove that the investment will generate positive cash flow, month in, month out.

Using Modern Tools for Smarter Investments

Let's be honest. Manually hammering out yields, ROI, and cash flow for every potential property is more than just slow—it's a minefield of costly human errors. The days of wrestling with fragile, complicated spreadsheets are numbered. For today's UK investor, modern, automated tools are simply a better way to work.

Most of the basic online tools you'll find are little more than a simple gross buy to let yield calculator. They miss the crucial details of UK financing and tax, giving you a dangerously optimistic number. That headline figure ignores the real-world costs that actually determine if a deal works, from Stamp Duty Land Tax to the brutal realities of Section 24.

From Manual Labour to Automated Analysis

This is where advanced analytical tools completely change the game for investors in 2026. Instead of burning hours typing in data and double-checking formulas, you can generate a comprehensive financial model in minutes. This frees you up to focus on what actually matters: making smart investment decisions.

Think about the typical workflow. You're sourcing data, crunching various metrics, and trying to forecast what might happen next. Automation handles these repetitive tasks with a speed and accuracy that's impossible to match by hand, especially when you're trying to compare multiple properties at once.

The Power of AI-Driven Insights

Modern tools like the DealSheet AI app are built from the ground up for the UK market, automating the entire analysis process. You can just feed it a property listing URL, and the AI intelligently extracts the data it needs to build a complete financial forecast.

It goes far beyond a basic buy to let yield calculator by:

- Applying UK-Specific Rules: It automatically calculates the correct SDLT for your situation and models the precise impact of Section 24 tax rules on your bottom line. No guesswork.

- Generating Instant Models: It delivers a full breakdown of gross yield, net yield, cash flow, and ROI, giving you a complete picture of the investment's health.

- Enabling Rapid Comparison: This is where the real power lies. You can analyse dozens of potential deals in the time it would take to manually model just one. This allows you to compare opportunities side-by-side with consistent, reliable data.

By removing the friction of manual data entry and complex calculations, investors can move faster and with far greater confidence. This technology empowers you to spot the high-performing assets and discard the unprofitable ones before you invest any significant time or money.

This technological leap means you can make data-backed decisions in minutes, not hours. The automation does the heavy lifting, ensuring your assumptions are grounded in realistic UK costs and tax laws. You can see the specific property investment analysis features of DealSheet AI and discover how it streamlines this critical process.

Still Got Questions About Rental Yield?

Even with the best tools in hand, a few questions pop up time and again for UK property investors. Let's tackle the most common ones to help you sharpen your analysis and invest with more confidence.

What Is a Good Rental Yield in the UK for 2026?

Honestly, a 'good' yield totally depends on your strategy and where you're buying. As a general rule of thumb, many UK investors aim for a gross yield of 6% or more. You'll often see numbers like this in places like the North East, where lower house prices make it easier to achieve stronger returns on paper.

But the number that really matters is the net yield. Once you've stripped out all your running costs, landing a net yield in the 4-5% range is a pretty solid and realistic goal for many. In high-growth areas like London, investors might knowingly accept a much lower net yield—sometimes just 2-3%. They're playing a different game, betting that the appreciation in the property's value will deliver most of their profit over the long run.

Ultimately, a great investment isn't just about yield; it's about striking the right balance between healthy cash flow and the potential for solid capital growth.

How Should I Factor Void Periods into My Calculation?

If you want a realistic forecast, you have to plan for the time your property might sit empty between tenants. It's a reality of being a landlord. A common and sensible approach is to assume you'll have one month's void period each year.

This means you should calculate your annual income based on 11 months' rent, not 12. Simple, but it makes a huge difference.

Another way to do it is to shave a percentage off your total potential rent, usually somewhere between 5% and 8%. Whichever method you choose, plugging this into your buy to let yield calculator makes your final net yield figure far more reliable.

Can I Improve My Buy to Let Yield?

Absolutely. You're not just a passive observer here; you can actively pull levers to improve your property's yield. The most obvious one is raising the rent, but you have to be careful. Get too greedy and push it beyond local market rates, and you could end up with a long, expensive vacancy that wipes out any gains.

A smarter strategy is often to focus on reducing your running costs. This can mean:

- Refinancing your mortgage to lock in a better interest rate.

- Shopping around for a more competitive landlord insurance policy.

- Self-managing the property to eliminate letting agent fees, but only if you genuinely have the time and know-how.

Beyond that, making smart, cosmetic upgrades can often justify a higher rent, giving a direct boost to your overall yield and return on investment.

Stop second-guessing and start making data-backed decisions. The DealSheet AI app replaces fragile spreadsheets with a powerful, UK-focused buy to let yield calculator. Analyse any deal in seconds and see the real numbers before you invest. Download DealSheet AI and start your free trial today.