A Modern Guide to Buying Off Plan Property in the UK in 2026

A Modern Guide to Buying Off Plan Property in the UK in 2026

Buying a property off-plan in the UK is a strategy where you commit to purchasing a home before it's built, often securing it with just architectural drawings and a developer's reputation. It offers a unique chance to lock in today's price for a future asset, potentially gaining capital growth during construction. However, this path is laden with risks, such as market downturns and construction delays. This guide provides the answer to navigating this complex process, breaking down every step into a clear, actionable roadmap for UK investors. To instantly stress-test the numbers on any potential deal, savvy investors now use tools like the DealSheet AI app to ensure their decisions are backed by solid data.

What Buying Off-Plan Really Means for UK Investors

At its heart, buying off-plan is an act of faith—but it has to be faith backed by some seriously rigorous due diligence. You are committing a huge amount of capital to a property that only exists on paper, banking on the promise that it will be delivered exactly as specified, on time, and for the price you agreed. It's a bit like getting a bespoke suit made; you agree on the design, the materials, and the price upfront, then you have to wait patiently for the final product to be tailored.

For UK property investors, this has long been a go-to strategy for buying off plan. The main attraction is the potential for capital appreciation while the builders are still on site. If the property market climbs between you exchanging contracts and the day you get the keys, you could be sitting on an asset worth more than you paid for it from day one.

The Market Context for 2026

But let's be clear, the landscape for buying off-plan has changed. The UK market has been through a dramatic shift, with recent history telling a story of a major cooldown. Back in 2016, off-plan sales hit their zenith, accounting for 49% of all new-build homes sold before completion. Fast forward to 2024, and that figure had collapsed to just 31%—the lowest it had been since 2012. This significant drop has reshaped how both developers and investors approach new-build strategies. As we look towards 2026, the market is adjusting to a new normal, where diligent analysis is more critical than ever. Discover more insights about these UK market trends.

This shift doesn't mean the strategy is dead in the water. Far from it. What it really means is that you need to be much more careful with your analysis and have a far deeper understanding of the risks. A more selective market can actually create some fantastic opportunities for savvy investors who do their homework properly.

A successful off-plan investment isn't just about betting on market growth. It's about meticulously vetting the developer, understanding the legal contract, and ensuring the numbers work under various economic scenarios.

Buying Off Plan At A Glance

To make sure we're on the same page, let's break down exactly what buying off-plan entails. This table summarises the core concepts, benefits, and risks you'll be dealing with.

| Aspect | Description |

|---|---|

| Commitment | You agree to buy a property based solely on plans and renders before it's built. |

| Payments | A reservation fee is followed by a 10-20% deposit on exchange, with the rest due at completion. |

| Pricing | The purchase price is fixed at exchange, protecting you from rises but exposing you to falls. |

| Timeline | The build period can be long, from several months to a few years, demanding a long-term view. |

| Potential Upside | Possibility of capital growth during construction and securing a brand-new, high-spec asset. |

| Key Risks | Developer failure, construction delays, market downturns, and financing issues at completion. |

Understanding these fundamentals is the first step. It's not a get-rich-quick scheme; it's a calculated investment that demands patience and a clear head.

The Core Concepts You Need to Grasp

To really get your head around the mechanics, it helps to break it down into its most basic parts. Here's a quick summary of what buying off-plan involves:

- Early Commitment: You agree to purchase a property before it's physically complete, often working from just floor plans and slick computer-generated images.

- Staged Payments: The process kicks off with a small reservation fee, followed by a much larger deposit (usually 10-20%) when you exchange contracts. The final balance is only due when the property is finished and ready to move into.

- Fixed Purchase Price: You lock in the price on the day you exchange. This is great if the market goes up, but it also means you're exposed if prices fall before completion.

- Long-Term Horizon: The gap between exchange and completion can be anything from a few months to a couple of years. This isn't a quick flip; it requires a genuine long-term investment mindset.

Navigating the Off-Plan Purchase Journey Step by Step

Buying a property off-plan isn't like a typical house purchase. It's a structured journey with clear milestones, but it plays out over a much longer timeline that's dictated by the construction schedule. Patience and a clear head are essential. Knowing the roadmap from day one is the key to managing your expectations and moving through the process with confidence.

It all starts with finding a promising development and doing some serious homework on the developer and the location. This is where you dig into their track record, read reviews, and really analyse the area's growth potential. Our guide on what property sourcers need to deliver can help you spot a quality opportunity from a dud.

Stage 1: Reserving Your Plot

Once you've picked out the specific unit you want, the first small financial step is paying the reservation fee. This is usually a modest sum, somewhere between £500 and £2,000, and it effectively takes the property off the market for a set period, typically 28 days.

This fee is usually taken off the final purchase price, but be warned: it can be non-refundable if you get cold feet and pull out. As soon as you've paid it, the clock starts ticking for you to get your finances in order and instruct a solicitor.

It's absolutely critical to appoint a solicitor who specialises in new-build conveyancing. They'll be familiar with the complex contracts and tight deadlines involved in buying off-plan, providing a crucial layer of protection.

Stage 2: The Legal Process and Exchange of Contracts

This is the most critical phase of the entire process. Your solicitor will get the legal pack from the developer's team and will start digging into the details, conducting searches, and raising enquiries. They'll scrutinise the contract, the lease (if it's a flat), and all the planning permissions to make sure everything is watertight.

At the same time, you need to be securing a formal mortgage offer. Once your solicitor is happy and your funding is approved, you'll move to the exchange of contracts. This is the point of no return. You'll pay the main deposit—usually 10% of the purchase price—and you are now legally bound to buy the property. Backing out after this stage comes with serious financial penalties.

Stage 3: The Construction Period

After you've exchanged contracts, the waiting game begins. The developer gets to work building your property, a process that can take anywhere from six months to over two years. During this time, you should be getting regular construction updates.

This is the period where you hope to see some capital appreciation. The market's performance during this long wait is a huge factor in whether your investment pays off. Looking ahead to 2026, economists are forecasting a period of stabilised interest rates and modest, single-digit house price growth across the UK. This creates a potentially favourable environment for off-plan investors who lock in prices early, but it also means that the days of guaranteed double-digit annual gains are likely behind us, making careful project selection even more important.

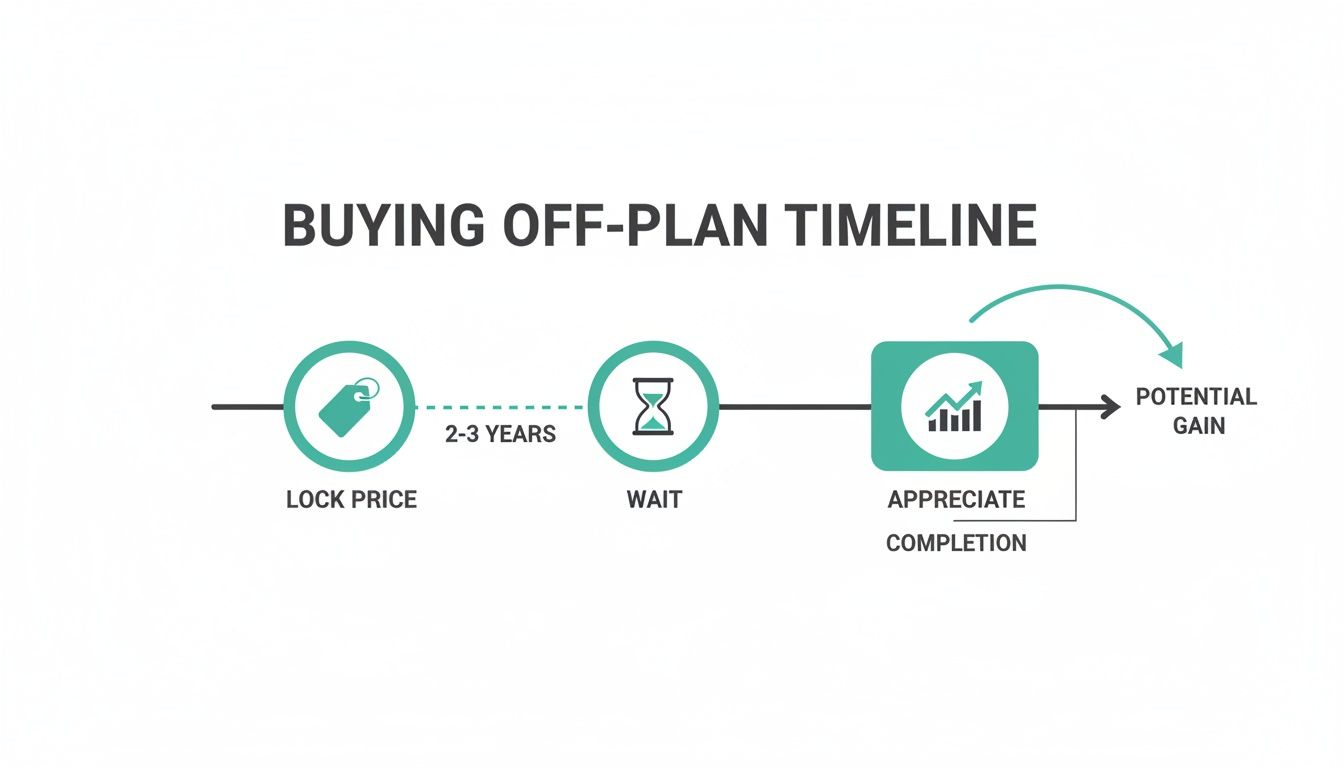

The timeline below gives you a clear visual of the off-plan journey, from locking in your price to the potential for growth during the build phase.

This visual highlights the passive nature of the investment while construction is underway, where the main goal is for the asset's value to grow without you having to do anything.

Stage 4: Completion and Handover

As construction finally wraps up, the developer will issue a 'notice to complete'. This is a formal notification giving you a fixed period, usually 10 working days, to transfer the rest of the money. Your solicitor will handle the final legal bits and pieces and get your ownership registered with the Land Registry.

Before this happens, you'll have two important jobs to do:

- Finalise Your Mortgage: Your original mortgage offer may have expired by this point. You'll need to re-engage with your lender to make sure your funds are ready to be drawn down.

- Conduct a Snagging Survey: You'll be invited to inspect the property just before completion. It's highly advisable to hire a professional snagging inspector to identify any defects—from minor cosmetic issues to more significant problems—which the developer is contractually obliged to fix.

Once the funds have been transferred, you've officially completed the purchase. You can collect the keys to your brand-new property, bringing your off-plan journey to a successful close.

Weighing the Rewards and Risks of Buying Off Plan

Every property strategy with serious upside has a catch, and buying off plan is the perfect example. It's a game of trade-offs. To make a smart decision, you need to cut through the glossy brochures and get a clear-eyed look at both sides of the coin. This isn't an emotional choice; it's a calculated one based on genuine opportunities versus very real potential pitfalls.

On one hand, the rewards can be substantial. On the other, the risks can have painful financial consequences if you don't see them coming. Let's break down exactly what you're weighing up.

Weighing the Risks and Rewards of Off-Plan Investment

Before we get into the nitty-gritty, it's helpful to see the core arguments for and against laid out side-by-side. This table gives you a quick snapshot of the balance you need to strike.

| Pros (Potential Upside) | Cons (Potential Downside) |

|---|---|

| Lock in a price today and potentially gain equity from a rising market during the build. | You're stuck with the agreed price even if the market falls, risking negative equity on day one. |

| You get a brand-new, energy-efficient property that attracts premium tenants. | The final quality might not match the slick brochure, and snagging can be a major headache. |

| Early buyers can often customise finishes, creating a bespoke home or rental unit. | Construction delays are common, which can torpedo your mortgage offer and financial plans. |

| A 10-year structural warranty (like NHBC) provides peace of mind against major defects. | The developer could go bust, leaving you in a long and stressful fight to recover your deposit. |

Ultimately, a successful off-plan investment isn't about hoping for the best; it's about rigorously planning for the worst while positioning yourself to capture the upside.

The Potential Rewards of Buying Off Plan

The main pull of buying off plan is, without a doubt, financial. Investors are drawn in by the chance to lock in a price years ahead of time and watch the market work in their favour before they even own the keys.

- Capital Appreciation During Construction: This is the big one. You agree a price today for a property that might not be finished for two years. If the market climbs during that time, you could be sitting on a tidy paper profit the moment you complete.

- Securing a Brand-New Property: You'll be the very first person to live there. That means modern kitchens and bathrooms, high energy efficiency, and zero wear and tear. For landlords, a pristine new-build often attracts higher-quality tenants and can command a premium rent.

- Customisation Options: Get in early enough, and you'll often get to pick your own finishes. We're talking kitchen worktops, flooring, and paint colours, letting you tailor the place to your own taste or create a neutral palette perfect for the rental market.

- Structural Warranties: Almost every new-build in the UK comes with a 10-year structural warranty from a provider like the NHBC. This is a huge safety net, protecting you from the financial nightmare of major structural defects.

The Inherent Risks You Must Consider

While the upside looks tempting, the risks involved demand your full attention. This is where inexperienced investors get caught out, blinded by the potential rewards.

The biggest mistake an investor can make is to focus solely on the potential upside without rigorously stress-testing the downsides. A successful off-plan strategy is built on mitigating risk, not ignoring it.

Understanding these risks is your first line of defence.

- Market Downturns: This is the flip side of capital appreciation. If property prices fall while your home is being built, you're still legally bound to buy it at the higher price you agreed to. You could find yourself in negative equity from the moment you get the keys.

- Construction Delays: Delays are almost a given in the building trade. A project getting pushed back by months—or even a year—can wreak havoc on your finances, especially your mortgage offer, which will likely expire after six months.

- Financing Issues: Your mortgage offer in principle is a snapshot in time, based on your finances today. If your circumstances change, or if lenders tighten their criteria before completion, you could find yourself unable to get the mortgage you need. This is a critical risk that could force you to pull out and lose your deposit.

- Quality Discrepancies: The finished property can sometimes be a let-down compared to the slick CGI images and swanky show home. The quality of the final finish can vary, and what you see in the brochure isn't always what you get. To get a better handle on this, it helps to understand the latest trends in UK building costs per square metre.

- Developer Insolvency: It's rare, but it happens. The developer could go bust before your property is finished. While your deposit should be protected by the warranty provider, getting your money back can be a long, drawn-out, and stressful affair.

Securing Finance and Understanding UK Tax Rules

Two of the biggest hurdles you'll face when buying off-plan are getting the right mortgage sorted and making sense of UK tax law. First up, we need to untangle the mortgage maze, which is a unique headache for new-builds. Most mortgage offers simply expire after six months, creating a massive problem when construction can drag on for a year or even longer.

This section gives you proven strategies for dealing with this timing mismatch, from finding specialist brokers to building yourself a solid financial safety net. We'll then break down UK Stamp Duty Land Tax (SDLT), explaining exactly when you have to pay it and how the rates apply to you, so you can budget accurately and avoid any nasty surprises down the line.

The Off-Plan Mortgage Maze

Getting a mortgage for an off-plan property isn't as simple as it is for a house that's already built. The main problem is the shelf-life of a mortgage offer. Most UK lenders will only give you an offer that's valid for six months. Since many off-plan projects take 12-24 months to finish, your first mortgage offer will almost certainly be dead and buried before the property is ready.

This timing gap creates a huge risk. When you have to re-apply for the mortgage closer to completion, you'll be put through a whole new round of financial checks. If your personal situation has changed – maybe you've switched jobs or your income has dipped – or if the bank has tightened its lending rules, your application could be rejected. This leaves you unable to complete the purchase and at very real risk of losing your entire deposit.

Strategies for Managing Mortgage Risk

So, how do you bridge this gap and protect your investment? It all comes down to proactive planning. Just crossing your fingers and hoping for the best is not a strategy.

- Work with a Specialist Broker: A mortgage broker who lives and breathes new-builds is worth their weight in gold. They have relationships with lenders who offer more flexible products, like mortgages with longer validity periods (some go up to 12 months) or those who are simply more clued-up on the off-plan process.

- Maintain Financial Stability: It's absolutely critical to keep your finances as boringly stable as possible between exchanging contracts and completing the purchase. Avoid taking on new debt, don't change jobs if you can help it, and make sure your credit score stays healthy. Lenders will put your affordability under the microscope again right before completion.

- Build a Contingency Fund: You must have a financial buffer. If the lender's surveyor down-values the property at completion, you will have to find the cash to cover the shortfall yourself. Aim to have extra reserves to handle this, or to stomach a potential rise in interest rates when you re-apply.

Securing a mortgage for an off-plan purchase is a two-stage process. The first approval gets you to the exchange of contracts, but the final, binding approval only happens just before completion. Treat them as two separate financial hurdles to clear.

Understanding UK Stamp Duty Land Tax (SDLT)

The other big financial consideration is Stamp Duty Land Tax, or SDLT. A common mistake people make is thinking you pay this tax when you exchange contracts. That's wrong.

SDLT is only payable upon the legal completion of the property purchase. You have 14 days from the completion date to file your SDLT return and pay HMRC what you owe. Your solicitor will usually handle the paperwork for you, but the bill is all yours. You can learn more by checking out our comprehensive guide on what Stamp Duty Land Tax is.

The amount you pay is based on the purchase price you locked in when you exchanged contracts, not what the property might be worth at completion. The rates are tiered, so you pay different percentages on different parts of the property's price. What's more, if this purchase means you now own more than one property, you will almost certainly have to pay the 3% higher rate surcharge for additional homes. Factoring this into your budget from day one is non-negotiable.

Your Essential Due Diligence Checklist

Think of this as your shield against a bad investment. When you're buying off plan, a glossy brochure and a smooth sales pitch are not enough to protect your capital. A thorough due diligence process is the single most important thing you can do to separate a prime opportunity from a potential disaster.

This isn't about just ticking boxes; it's about building a complete, objective picture of the investment before you commit a single pound. Following this checklist will help protect your deposit and ensure you're backing a project with a high probability of success. It covers everything from putting the developer under the microscope to vetting the legal documents and analysing the long-term prospects of the location itself.

Scrutinising the Developer

The success of any off-plan project rests almost entirely on the developer. Their experience, financial health, and reputation are the best indicators you have of whether they'll actually deliver on their promises. You're not just buying a future property; you're entering into a long-term partnership with the company building it.

Your investigation should include:

- Track Record Analysis: Look at their previously completed projects. Are they of high quality? Were they delivered on time? Search for online reviews, news articles, and forum discussions about their past work.

- Site Visits: If you can, go and visit one of their finished developments. Speak to residents if the opportunity arises. This gives you a real-world feel for the quality of their construction and finishing that marketing materials can easily hide.

- Financial Health Check: Your solicitor can run checks on the developer's company structure and financial stability through Companies House. Look for signs of financial distress or a history of failed ventures.

- Warranty Provider: Confirm they are using a reputable 10-year structural warranty provider, such as the NHBC or Premier Guarantee. This is a non-negotiable safety net.

Vetting the Legal Pack

Your solicitor is your most important ally in this process. They are responsible for dissecting the legal contract and flagging any clauses that could put you at a disadvantage. It's absolutely crucial to use a solicitor with specific experience in new-build conveyancing, as standard contracts are often weighted heavily in the developer's favour.

The legal pack is where the developer's promises are put into writing. Your solicitor's job is to ensure there are no loopholes that could allow for changes to the specification, indefinite delays, or unfair penalties.

Key areas for your solicitor to review include:

- The Contract: Scrutinise clauses related to the completion date, the developer's right to alter plans or materials, and your rights if they fail to deliver.

- The Long-Stop Date: Make sure there is a reasonable 'long-stop date'. This is the final deadline by which the developer must complete the property, after which you can cancel the contract and get your deposit back.

- Leasehold Terms: If it's a flat, check the length of the lease, the ground rent terms (especially any aggressive review clauses), and the estimated service charges.

- Planning Permissions: Verify that full and final planning permission has been granted for the entire development, not just outline permission.

Analysing the Location and Market

Finally, you have to look beyond the four walls of the development itself and analyse the investment potential of the surrounding area. A beautiful new flat in a poorly connected area with no amenities is unlikely to see strong capital growth or rental demand.

You can explore how developers assess a project's potential in our guide to understanding Gross Development Value.

Your location analysis should confirm:

- Local Infrastructure: Are there good transport links, schools, and shops nearby? Are there any planned infrastructure projects (like a new train line) that could boost values?

- Rental Demand: Research the local rental market. Is there strong demand for the type of property you are buying? Check platforms like Rightmove and Zoopla for comparable rental prices.

- Regeneration Plans: Is the area part of a wider regeneration scheme? Large-scale investment can significantly lift property values over the long term.

- Market Comparables: Look at the prices of similar new-build and second-hand properties in the immediate vicinity to ensure you are not overpaying.

How to Analyse Off-Plan Deals with DealSheet AI

When you're buying off-plan, your edge comes down to just two things: how fast you can analyse a deal, and how accurate those numbers are. The days of wrestling with clunky spreadsheets to guess a property's future potential are well and truly over. To keep up, you need a tool that turns a developer's brochure into hard financial data in seconds, not hours.

This is where the right technology gives you a serious advantage. Instead of plugging in dozens of variables by hand, purpose-built apps let you model a deal's real-world viability almost instantly. It's not just about saving time; it's about applying an institutional-grade level of scrutiny to every opportunity, making sure your decisions are backed by solid numbers, not just a gut feeling.

From Brochure to Balance Sheet in Seconds

The initial analysis of an off-plan deal is often a massive bottleneck. You get a glossy marketing brochure with a purchase price, a floor plan, and some very optimistic rental figures. The real challenge is translating that sales pitch into a proper financial forecast that accounts for every single UK-specific cost and tax.

DealSheet AI was built to solve this exact problem. You can simply upload a PDF of the developer's marketing pack or even just a screenshot of the property details. The app's AI gets straight to work, pulling out the key data points—purchase price, number of bedrooms, location—and instantly building a deal analysis for you.

The goal is to move beyond the developer's sales pitch and build your own independent financial model. Technology allows you to do this almost instantly, giving you the clarity needed to decide whether to pursue the deal or walk away.

This automated process completely slashes your due diligence time. What used to take a whole evening battling a spreadsheet can now be done in the time it takes to make a coffee. This lets you sift through more opportunities and focus your energy only on the ones that actually stack up.

Modelling Growth and Stress-Testing for Reality

A credible analysis has to go far beyond a simple yield calculation. When you're buying off-plan, you absolutely must model future scenarios and stress-test the investment against potential market shocks. This is where a dedicated tool becomes indispensable.

Within DealSheet AI, you can model all sorts of outcomes for your investment. The dashboard instantly crunches the key metrics like ROI and cash flow, automatically factoring in all the UK-specific costs like SDLT, giving you the confidence to make quick, informed decisions.

You can tweak your assumptions for capital growth during the construction phase to see how different market movements would affect your equity position when you finally get the keys.

More importantly, you can stress-test the deal against future interest rate hikes. With rates projected to shift, understanding how a rise of 1% or 2% would hammer your monthly cash flow is critical. This feature helps you pinpoint the deal's break-even point, making sure your investment stays profitable even if borrowing costs creep up.

Exploring the full range of DealSheet AI features shows you how to build this kind of resilience into your portfolio. It's all about having confidence in your numbers and being able to quickly filter out the deals that don't meet your risk-reward criteria.

Common Questions About Buying Off Plan Property

Even with a solid strategy in place, a few nagging questions always seem to pop up when you're sizing up an off-plan deal. It's completely normal. This is where we tackle the most common queries we hear from UK investors, giving you direct, clear answers to help you get past any lingering uncertainties before you take the plunge.

Can I Pull Out of an Off Plan Purchase in the UK?

In short, yes—but it can be an incredibly expensive decision. If you get cold feet after paying a reservation fee but before you've exchanged contracts, you'll almost certainly lose that fee. It's painful, but manageable.

The real trouble starts if you try to pull out after exchanging contracts. At this point, the consequences are severe. You will absolutely forfeit your entire deposit, which is usually 10% of the property's price. To make matters worse, the developer could even sue you for any additional losses they suffer trying to sell the property to someone else. It's a move that should only ever be considered a last resort.

What Happens If the Property Value Drops Before Completion?

This is one of the biggest risks in the off-plan game, and you need to go into it with your eyes wide open. You are legally locked in to complete the purchase at the price you agreed when you exchanged contracts. It doesn't matter if the market has fallen since then.

Here's the crucial part: your mortgage lender will base their loan offer on a fresh valuation conducted just before completion. If that valuation comes in lower than the price you're contracted to pay, it creates a funding gap. You are personally on the hook to find the cash to cover that shortfall.

A long-stop date is a critical safety net in your contract. It provides an ultimate deadline for completion, protecting you from indefinite delays and giving you a clear exit path if the project stalls.

What Is a Long Stop Date in an Off Plan Contract?

Think of the 'long-stop date' as your ultimate get-out-of-jail-free card. It's a non-negotiable clause in your purchase contract that sets the final, absolute deadline by which the developer must finish the property.

If the developer blows past this date, you typically gain the legal right to walk away from the deal (or 'rescind' the contract) and get your full deposit back. It's vital that your solicitor makes sure this date is reasonable and properly protects your interests from never-ending delays.

How Do I Deal with Defects or Snagging in a New Build Property?

Just before completion, the developer will invite you for a pre-completion inspection. My advice? Don't go alone. It is well worth the money to hire a professional snagging inspector for this visit. They have a trained eye and will create a detailed, impartial list of every single defect, from tiny cosmetic flaws to more serious issues.

The developer is then legally required to fix everything on that list. For long-term peace of mind, nearly all new builds in the UK also come with a 10-year structural warranty, like an NHBC Buildmark policy. This is your protection against any major structural problems that might appear down the line.

Take the guesswork out of your investment analysis. With DealSheet AI, you can underwrite any off-plan opportunity in seconds and make decisions with confidence. Download the app and start your free trial today at DealSheet AI on the App Store.