A Modern Guide to Calculating Rental Yield UK in 2026

A Modern Guide to Calculating Rental Yield UK in 2026

Figuring out how to calculate rental yield is the single most important metric for any UK property investor. It's the number that tells you, in simple terms, how hard your money is actually working. The basic formula is straightforward: Gross Yield = (Annual Rental Income ÷ Total Property Cost) x 100, giving you a quick way to filter deals. To get the real story of an investment, however, this article will guide you through calculating the all-important 'net' yield—the figure that truly defines your cash flow.

For serious investors looking to analyse deals quickly and accurately, tools are now making this much easier. For instance, the DealSheet AI app can automate these critical calculations straight from a property listing, ensuring you get a robust analysis in seconds instead of fiddling with a spreadsheet.

Your Foundational Metric: Rental Yield Explained

Think of rental yield as the compass for your entire property journey. It's a simple percentage that measures the annual return you're getting from rent, relative to what the property cost you to acquire. In essence, it's the interest rate on your investment—a higher yield means your capital is generating more income.

This one metric helps you cut through the emotional noise and market hype. A property might be in a fantastic area and look great on paper, but if the yield is poor, it simply might not be the right fit for your goals, especially if you're focused on generating a regular income.

Nailing this calculation is the first real step toward building a profitable portfolio. If you're just getting started, our complete guide on investing in property for beginners is a great place to build your knowledge.

Gross vs. Net: The Crucial Difference

When you're calculating rental yield, you'll constantly hear two terms: gross and net. Understanding the difference isn't just a nice-to-have; it's non-negotiable for any serious UK investor.

-

Gross Yield is your top-level, quick-and-dirty calculation. It only looks at the total annual rent against the total property cost (that's the purchase price plus buying costs like Stamp Duty and legal fees). It's perfect for rapidly sifting through dozens of potential deals to see which ones are even worth a second look.

-

Net Yield gives you the real-world picture of profitability. This is where you subtract all your running costs—things like mortgage interest, insurance, management fees, and a budget for maintenance—from the annual rent before you do the calculation. This is the number that tells you what cash will actually end up in your bank account.

A high gross yield can be seriously misleading. A property might look tempting with a 9% gross yield, but once you factor in high service charges or hefty maintenance costs, its net yield could plummet to a much less attractive 3-4%. Always, always dig deeper to find the net figure.

Why Regional Yields Vary So Much in the UK

Calculating rental yield in the UK has become a cornerstone of savvy property investing, and it's amazing how much returns can differ from one region to another. Data consistently shows that certain postcode districts, especially in the North of England, can deliver gross yields that blow London's typical 3-5% out of the water.

It's not uncommon to see hotspots in the North East and North West hitting yields of around 7-9%. This regional variation is why local knowledge and analysis are so powerful.

At a Glance: UK Gross Rental Yields in 2026

To give you a clearer picture, here's a rough guide to what you might expect across different parts of the UK. Remember, these are just typical ranges for 2026 and your own due diligence is what counts.

| UK Region | Typical Gross Yield (Buy-to-Let) | Typical Gross Yield (HMO) |

|---|---|---|

| North East | 7.5% - 9.5% | 11% - 15% |

| North West | 7.0% - 9.0% | 10% - 14% |

| Yorkshire & Humber | 6.5% - 8.5% | 10% - 13% |

| Scotland | 7.0% - 9.0% | 11% - 14% |

| West Midlands | 6.0% - 7.5% | 9% - 12% |

| East Midlands | 5.5% - 7.0% | 9% - 11% |

| South West | 4.5% - 6.0% | 7% - 10% |

| South East | 4.0% - 5.5% | 6% - 9% |

| London | 3.5% - 5.0% | 5% - 8% |

As you can see, the strategy and location combine to create a huge range of potential outcomes. A high-yielding HMO in the North East looks very different on paper to a buy-to-let flat in the South East, which might offer lower income but stronger capital growth prospects.

Your First Calculation: A Practical Gross Yield Walkthrough

Theory is one thing, but nothing beats running the numbers on an actual deal. Let's get practical and walk through a gross yield calculation for a typical two-bedroom flat in a popular northern city like Leeds. This is where you see why the purchase price is only ever part of the story.

To get a realistic gross yield, you first need to work out the Total Property Cost. This isn't just the price you agree with the seller; it has to include all the upfront costs of acquisition that optimistic online listings conveniently ignore.

Tallying Up the Real Purchase Costs

Imagine you've found a great-looking flat with an agreed purchase price of £180,000. Before you can even think about rent, you've got to add the costs of actually buying the thing.

Here's a realistic breakdown for a first-time buy-to-let investor in 2026:

- Purchase Price: £180,000

- Stamp Duty Land Tax (SDLT): £7,900 (This includes the 3% second home surcharge).

- Legal Fees (Conveyancing): £1,500

- Survey Charges: £600

Add those up, and your actual Total Property Cost is £190,000—a full £10,000 more than the headline figure. Using this higher, more accurate number is fundamental to a proper yield calculation.

For another layer of analysis, it's worth understanding how other key metrics like a rent-to-value calculator can complement your assessment.

Calculating the Annual Rental Income

Next up, you need a credible figure for the annual rent. After researching comparable properties on the same streets and checking what's recently let, you determine a realistic market rent is £950 per calendar month (PCM).

To get the annual figure, it's a simple multiplication:

£950 (Monthly Rent) x 12 = £11,400 (Annual Rental Income)

Bringing It All Together for Gross Yield

Now we have the two critical figures for the gross yield formula: the true total cost and the total annual income.

The formula is: (Annual Rental Income ÷ Total Property Cost) x 100 = Gross Yield

Let's plug in our numbers from the Leeds flat example:

** (£11,400 ÷ £190,000) x 100 = 6.0%**

So, the true gross yield for this property is 6.0%. This is a solid, factual starting point. It gives you a clear basis for comparing this deal against others before you even begin factoring in the running costs that will ultimately determine your net profit.

Moving Beyond Gross to Find Your True Profitability

While gross yield is a great first filter for shortlisting properties, it's the net yield that tells you the real story. This is the figure that successful investors obsess over because it represents the actual cash hitting your bank account after all the bills are paid.

Getting this right is absolutely central to calculating rental yield in the UK accurately. To find your net yield, you have to methodically subtract every single operational cost from your gross annual income. This process is what turns a promising headline number into a realistic projection of your investment's performance.

Itemising Your Operational Costs

Let's break down the typical expenses you'll need to account for. These are the recurring costs that will chip away at your rental income throughout the year. Forgetting even one of them can completely skew your numbers and lead to a nasty surprise down the line.

Common operational costs for a UK buy-to-let usually include:

- Letting Agent Fees: Typically 8-12% of the monthly rent for a full management service.

- Landlord Insurance: Absolutely essential cover for buildings, contents, and liability.

- Maintenance & Repairs: A sensible budget is crucial here. Many experienced investors set aside 10% of the annual rent, or 1% of the property's value each year, just for this.

- Ground Rent & Service Charges: These are mandatory for leasehold properties like flats and can vary massively.

- Void Periods: It's just smart business to budget for at least one month per year where the property might be empty between tenancies.

This list isn't exhaustive, either. You might also have costs for gas safety certificates, energy performance certificates (EPCs), and potential licensing fees depending on your local council. For a deeper dive, our buy-to-let profit calculator can help you model all these expenses in detail.

The Impact of Mortgage and Tax

For most investors, the single biggest outgoing is the mortgage payment. It's vital to remember you only subtract the interest portion of the payment for this calculation, not the capital repayment. Capital repayment isn't an expense; it's you paying off your own loan.

Furthermore, individual landlords in the UK have to contend with the massive impact of the Section 24 tax rules. You can no longer deduct your mortgage interest as a business expense. Instead, you get a basic rate tax credit of 20% on your interest payments. This makes your taxable income look higher and can seriously dent your final net profit, especially if you're a higher-rate taxpayer.

A Net Yield Calculation in Action

Let's go back to our £180,000 Leeds flat, which had a gross yield of 6.0% based on £11,400 in annual rent. Now, let's factor in the real-world running costs to find its true profitability.

Here's a realistic annual cost breakdown:

- Mortgage Interest: £4,800 (on a £135k interest-only mortgage at 3.55%)

- Letting Agent Fees (10% + VAT): £1,368

- Service Charge & Ground Rent: £1,200

- Landlord Insurance: £250

- Maintenance Budget (5% of rent): £570

- Void Period Provision (1 month's rent): £950

Total Annual Costs = £9,138

Now we can figure out the net income: Net Annual Income = £11,400 (Gross Rent) - £9,138 (Costs) = £2,262

And finally, we can calculate the net yield:

Net Yield = (Net Annual Income ÷ Total Property Cost) x 100

(£2,262 ÷ £190,000) x 100 = 1.19%

Suddenly, that promising 6.0% gross yield has become a much more sober 1.19% net yield. This is the stark reality of property investment, and it demonstrates precisely why net yield is the only figure that truly matters when you're assessing cash flow.

Adapting Your Yield Calculations for Different Strategies

A standard buy-to-let is a solid way to invest, but it's far from the only game in town. As you start exploring more complex models like Houses in Multiple Occupation (HMOs) or Serviced Accommodation (SA), your approach to calculating yield has to evolve. Each strategy has a completely different income structure and cost profile that demands its own tailored analysis.

Getting this right is what separates an amateur from a professional investor. While the core principles of Gross and Net Yield stay the same, the inputs you use will change dramatically. You need to be confident you're comparing apples with apples, whether you're looking at a terraced house for a family or a city-centre flat for short-term lets.

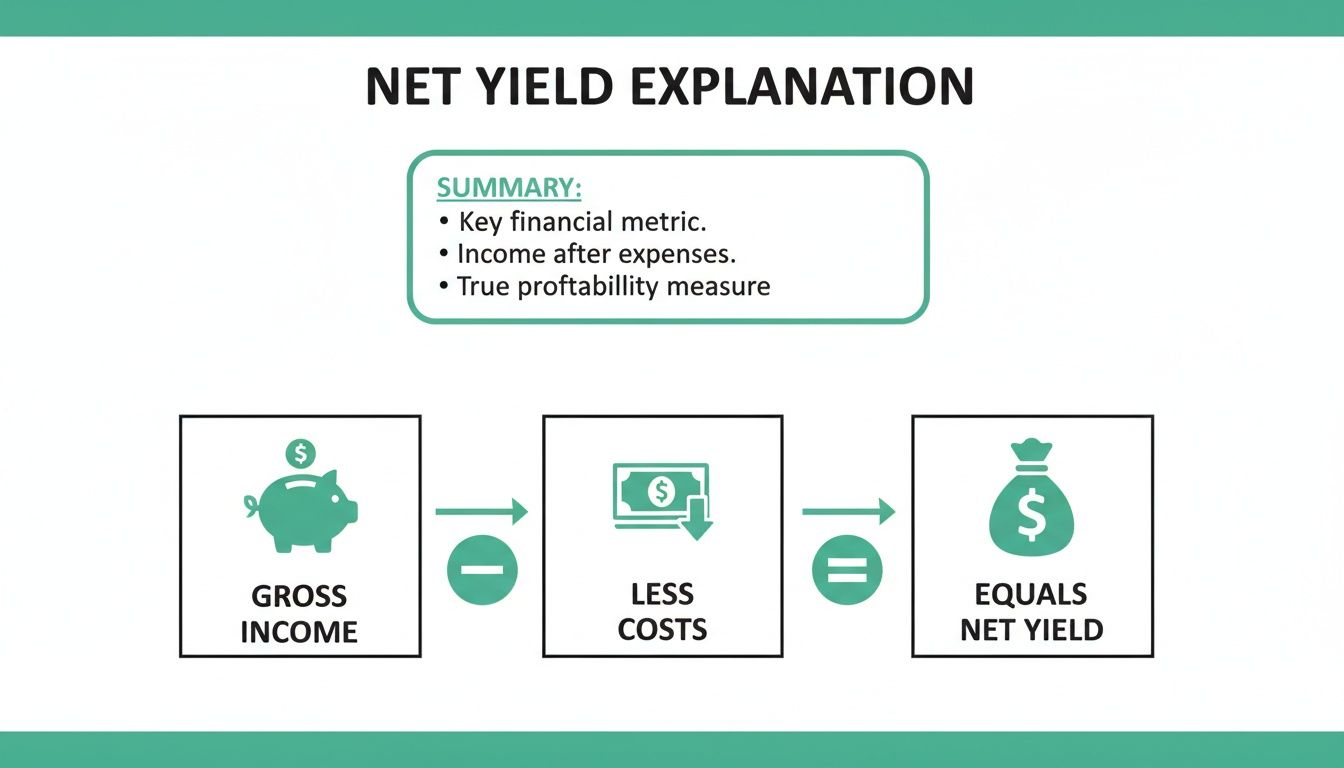

This visual breaks down the simple but powerful logic behind net yield.

As the graphic shows, your real profit is what's left after every single operational cost has been paid.

Calculating Yield for a House in Multiple Occupation (HMO)

With an HMO, you aren't letting the property to a single household; you're renting out individual rooms. This immediately changes the income side of the equation. Your annual rental income is the sum of all the rooms' rent combined.

On the flip side, HMOs almost always come with higher operational expenses. Landlords are typically on the hook for council tax and all utilities (gas, electricity, water, and broadband)—costs that a standard BTL tenant would cover themselves. You also have to factor in specific HMO costs like licensing fees, more frequent maintenance due to higher tenant turnover, and potentially more robust insurance policies.

Let's look at an example.

HMO Example: Imagine a 5-bedroom HMO purchased for a total cost of £250,000. Each room rents for £550 per month.

- Gross Annual Income: (5 rooms x £550) x 12 = £33,000

- Gross Yield: (£33,000 ÷ £250,000) x 100 = 13.2%

That impressive gross figure is pretty typical for HMOs and can easily catch your eye. However, after deducting a realistic £12,000 for bills, management, voids, and maintenance, the Net Annual Income drops to £21,000.

This brings the Net Yield to 8.4%. It's still a strong return, but it really highlights why a thorough cost analysis is non-negotiable. To dig deeper into this specific strategy, check out our guide on student accommodation as an investment.

Calculating Yield for Serviced Accommodation (SA)

Serviced accommodation, or short-term lets, operates much more like a hospitality business than a traditional rental. Forget monthly rent; your income is based on nightly rates, which can swing wildly with seasonality, local events, and even the weather. The most critical variable here is the occupancy rate.

Your gross income calculation should be: (Average Nightly Rate x Number of Nights Booked). A realistic occupancy forecast is absolutely vital. Assuming 100% occupancy is a rookie mistake and a recipe for disaster. A figure between 65-80% is a much more sensible starting point for any serious analysis.

Costs are also significantly higher and more varied. You'll be paying for all utilities, professional cleaning between every single guest, booking platform commissions (which can be 15% or more), and potentially higher management fees from specialist SA agents who know the market.

To show how the costs can really differ, here's a quick comparison of the unique operational expenses you'll face with each strategy.

Unique Costs Across UK Investment Strategies

| Expense Category | Standard Buy-to-Let | HMO | Serviced Accommodation |

|---|---|---|---|

| Utilities & Council Tax | Typically paid by the tenant | Usually paid by the landlord (all-inclusive rent) | Always paid by the landlord |

| Management Fees | 8-12% of monthly rent | 12-18% due to higher tenant turnover and complexity | 15-25% from specialist agents, plus platform fees (e.g., Airbnb) |

| Cleaning | End-of-tenancy clean, often paid by tenant | Communal area cleaning (weekly/fortnightly) paid by landlord | Professional cleaning and linen changeover between every guest, paid by landlord |

| Furnishings & Consumables | Unfurnished or basic furnishings | Fully furnished rooms and communal areas | Fully furnished and equipped, plus consumables (toiletries, coffee, etc.) |

| Licensing & Compliance | Standard landlord requirements | Mandatory HMO Licence in many areas, plus stricter fire safety standards | Short-term let licences in some areas (e.g., Scotland), planning considerations |

This table makes it clear why you can't just apply a standard BTL cost model to an HMO or SA deal—the numbers simply won't be accurate. You have to account for these specific, higher operational burdens to get a true picture of your net yield.

What a Good UK Rental Yield Actually Looks Like

Once you've got your head around the rental yield formulas, the next question is always the same: what number should I actually be aiming for?

The honest answer is, there's no single "good" figure. A target yield is completely personal, tied directly to your investment strategy and the specific locations on your radar.

Many UK investors are chasing a gross yield of 6-8% or more, which naturally pulls them towards high-cash-flow areas. But don't make the mistake of thinking a lower yield is automatically a bad deal. A 4% yield on a flat in a prime London postcode could be a phenomenal long-term hold if you're confident in its capital growth prospects.

This brings us to the fundamental trade-off every single investor has to make: balancing immediate cash flow (yield) against long-term growth (appreciation).

Navigating the Yield vs Growth Trade-Off

The UK property market has a pretty clear geographical divide on this front. High-yield hotspots are often found in northern cities and parts of the Midlands, where property prices are lower relative to the rent you can achieve. Think cities like Liverpool, Manchester, and Glasgow, which frequently give investors the chance to secure strong monthly cash flow from day one.

On the flip side, London and the South East typically offer much lower yields. Here, the sheer cost of property means the rental income is a smaller slice of the asset's value. The strategic play in these markets is less about monthly profit and more about banking on long-term capital growth, where property values have historically climbed more steeply.

Choosing between high yield and high growth is the central strategic decision for any UK property investor. It's essential to align your property search with this choice from the very beginning. If your goal is to replace your salary with rental income, you'll naturally focus on high-yield areas. If you're playing a longer game to build wealth through asset value, lower-yield, high-growth locations suddenly become much more attractive.

Understanding Current UK Market Dynamics for 2026

Recent market trends have added another interesting layer to this. An eye-opening statistic has been how dramatically rent growth has outpaced property prices in some regions.

For instance, the Office for National Statistics' Index of Private Housing Rental Prices (IPHRP) has shown persistent annual increases. Looking ahead to 2026, with rents potentially consuming over 30% of average incomes in most areas, tenant demand is expected to remain incredibly strong as home ownership remains a challenge for many. This powerful rental growth means that even in traditionally lower-yield areas, the numbers are starting to look more compelling for investors who acquire property at the right price.

This is why calculating rental yield UK is not a static skill; it must be applied within the context of the current market. To dig into this topic a bit deeper, check out our detailed guide on what constitutes a good rental yield.

The key takeaway is simple: you have to run your own numbers diligently. A property's real potential is often hidden just beneath the surface of those broad regional averages.

Common Questions We Hear About Rental Yield

Even when you've got the formulas down, some questions pop up repeatedly when calculating rental yield in the UK. Nailing these details is what separates a solid analysis from a costly mistake. Let's tackle the most common points of confusion.

Does Rental Yield Include Potential Capital Gains?

No, and this is probably the most important distinction to get straight. Rental yield is a pure cash flow metric. It's all about the income from rent measured against what the property cost you to acquire.

Capital gains—the profit you make when the property's value goes up over time—is a completely separate part of your overall return on investment (ROI). It's critical to keep these two separate. Yield tells you how the asset performs month-to-month, which is exactly what it's designed to do.

How Does Section 24 Impact My Net Yield?

For any individual landlord with a mortgage, Section 24 has a direct and often brutal impact on your net yield. The rules stop you from deducting your mortgage interest as a business expense before calculating your tax bill.

Instead, you get a 20% tax credit on your interest payments. This makes your taxable income appear much higher, which can easily push you into a higher tax bracket and demolish your final take-home profit. To get a true picture of your financial position, any credible net yield calculation has to account for this increased tax liability.

It's incredibly easy to underestimate the sting of Section 24. For a higher-rate taxpayer, this tax change alone can be the difference between a profitable investment and one that's barely washing its own face—or even losing money each month. Always model this cost carefully.

How Often Should I Re-Calculate My Yield?

On your existing properties, you should be re-running the numbers at least once a year. It's also a must-do whenever a major variable changes, like:

- A significant rent increase or decrease.

- A major, unexpected repair bill lands on your desk.

- You remortgage and your interest payments change.

And for new deals you're looking at? The answer is simple: every single time. This regular review makes sure your portfolio is actually performing as you think it is and helps you spot the underperformers that might need a decision.

Should I Trust the Yield Quoted on a Property Listing?

Treat any yield figure advertised by an estate agent with a huge dose of scepticism. These are almost always an optimistic gross yield, designed purely to grab your attention.

They often use a pumped-up rental estimate and, crucially, ignore all the extra purchase costs like Stamp Duty and legal fees. Think of it as a marketing number, not a serious piece of investment analysis. Always do your own research on local rents and calculate both the gross and, more importantly, the net yield yourself using a complete list of costs.

Stop second-guessing and start making data-driven decisions. The DealSheet AI app helps you calculate rental yield, ROI, and cash flow in seconds, straight from a property listing.

Analyse your next UK property deal with a free trial of DealSheet AI.