A Modern Guide to Flipping Property UK for Profit in 2026

A Modern Guide to Flipping Property UK for Profit in 2026

Flipping property in the UK can still build serious wealth, but the game has changed. The key to successful flipping property uk ventures in 2026 is no longer just buying a property and hoping for market growth; it's about meticulous, data-driven analysis from the very beginning. Profit is now made or lost in the numbers before you even commit to a deal. To gain a professional edge, modern investors are using tools like the DealSheet AI app to analyse opportunities instantly, ensuring every UK-specific cost and tax is calculated with precision.

The New Reality of Flipping Property in the UK

The old strategy of "buy, hope, and sell" is officially dead. As we look towards 2026, anyone serious about flipping property in the UK needs to understand the economic pressures that have reshaped the landscape. Success is still very much possible, but it's earned through precision and a solid strategy, not blind optimism.

Profit margins are tighter than ever. It's a squeeze caused by a perfect storm of factors:

- Hefty Purchase Costs: Higher Stamp Duty Land Tax (SDLT) rates for second homes add a significant chunk to your upfront costs, and you absolutely must bake this into every calculation.

- Soaring Renovation Expenses: The price of building materials and decent labour has shot up. Getting your refurb budget wrong is one of the fastest ways to wipe out your profit.

- Pricey Financing: Interest rates have been all over the place, directly impacting the cost of short-term finance like bridging loans—the bread and butter of most property flips.

Shifting from Speculation to Strategy

This new environment forces a complete change in approach. Successful flippers today are meticulous planners, not speculators. Your profit isn't a happy accident; it's engineered from day one through smart, calculated decisions. This means ditching the gut feelings and adopting a data-driven mindset.

The golden rule for a successful flip in 2026 is simple: you make your money when you buy, not when you sell. This means finding genuinely undervalued properties and having a crystal-clear grip on every single cost before you even think about making an offer.

Why Speed and Accuracy Are Your Secret Weapons

In a competitive market, the best deals don't hang around for long. Speed is your advantage. But moving fast without being accurate is a recipe for losing a lot of money, very quickly.

The ability to instantly analyse a potential flip—nailing the After Repair Value (ARV), the refurb budget, all the taxes, and the finance costs—is what separates the profitable investors from the cautionary tales. This guide is your modern playbook for doing just that, ensuring your next flipping property UK venture is built on a rock-solid financial foundation.

How to Find and Analyse Profitable Flip Deals

In property flipping, there's a golden rule every seasoned pro lives by: you make your money when you buy, not when you sell. Forget mindlessly scrolling through property portals for hours on end; the best opportunities are almost always found where nobody else is looking. To succeed in today's market, you need a smarter way to source deals and ruthless efficiency when you analyse them.

Let's be blunt: the market has got a lot tougher. Flipping in the UK has actually hit its lowest point in over a decade, with flips making up just 1.7% of sales in the first three quarters of 2023.

Why? Costs have shot up and tax policies have squeezed margins. As a result, average gross profits have plummeted from around £38,000 in early 2022 to a projected £22,000 in Q1 2025. That's a staggering 42% drop. You can read the full, sobering analysis from Hamptons here.

I'm not telling you this to put you off. I'm telling you this to focus you. With margins this tight, you simply cannot afford to get your numbers wrong.

Uncovering Hidden Property Gems

The most profitable flips are never just handed to you on a plate. They're the result of a proactive sourcing strategy that goes way beyond the obvious.

Your first move should be building real, genuine relationships with local estate agents. Let them know you're a serious, finance-ready buyer looking for specific types of properties—think probate sales, homes screaming for modernisation, or anything with a genuinely motivated seller. A good agent who trusts you will call you before a property even hits Rightmove.

Auctions are another fantastic hunting ground for bagging properties below market value. You'll often find unmortgageable homes, probate sales, or repossessions that terrify typical homebuyers but represent pure gold for a flipper. The key here is to do your homework meticulously, understand every word of the legal pack, and never, ever get carried away in the heat of bidding. Check out our in-depth guide to the best property auction sites in the UK to learn how to navigate them like a pro.

Finally, don't write off direct-to-vendor marketing. It's more effort, absolutely, but identifying and contacting owners of tired, empty, or unloved properties can lead to truly off-market deals with zero competition.

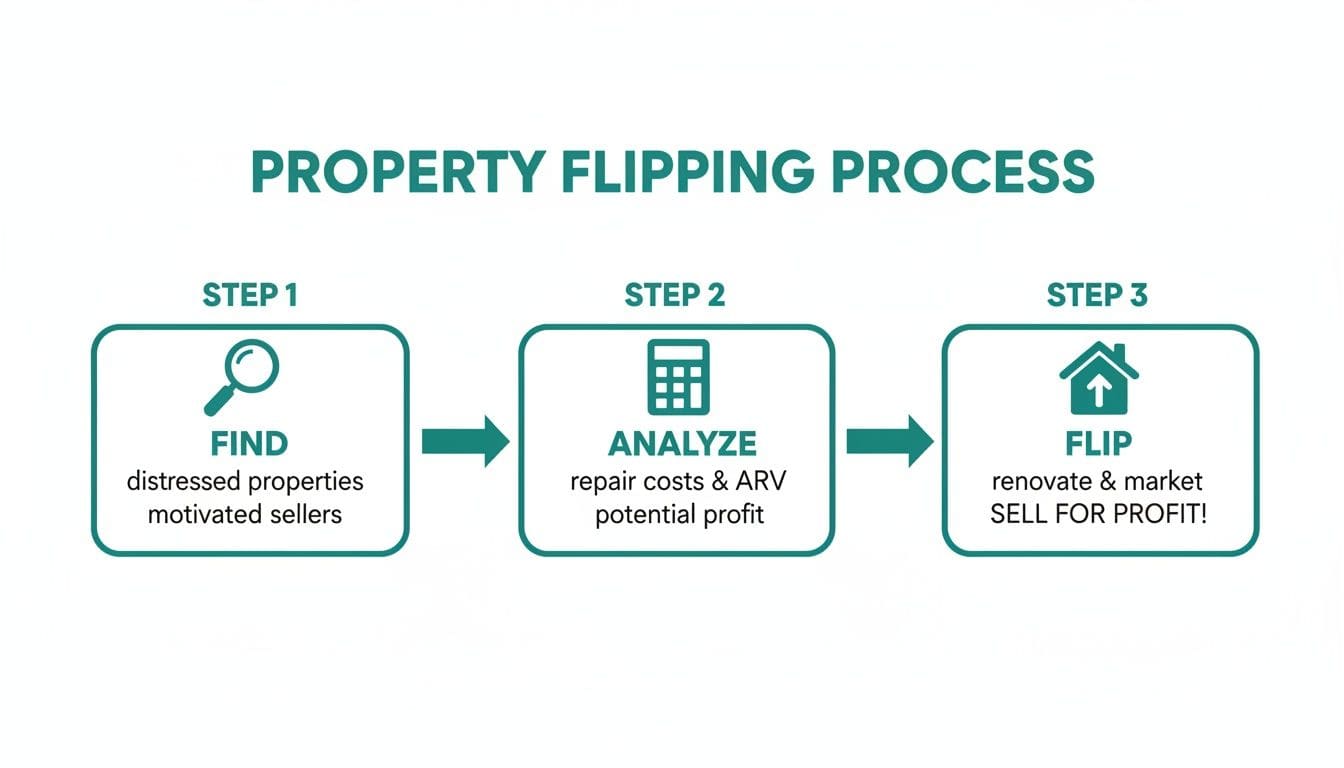

At its core, the process is simple, but each stage is critical.

Finding and analysing are distinct, vital stages that have to be nailed down long before you even think about picking up a paintbrush.

Mastering Rapid and Accurate Deal Analysis

Once you've found a potential deal, speed is your biggest advantage. The best opportunities get snapped up fast, so you need a system to run the numbers in minutes, not days. This is where you have to become an expert at underwriting.

Underwriting is simply the process of working backwards from the final sale price (the ARV, or After Repair Value) to figure out the absolute maximum you can pay for the property while still hitting your target profit. This means forecasting every single cost without fail.

The single biggest mistake new flippers make is underestimating costs. Your analysis must include everything: the purchase price, Stamp Duty, legal fees, broker fees, bridging loan interest, renovation costs, utility bills, council tax, estate agent selling fees, and your final Capital Gains Tax liability.

A decent rule of thumb to start with is the 70% Rule. It suggests you should pay no more than 70% of the property's ARV, minus the estimated repair costs. But this is just a guideline. For accurate UK calculations, a detailed breakdown is non-negotiable.

Here's a quick look at the kind of numbers you need to pull together instantly.

Example Flip Underwriting Template (Based on a £150,000 Purchase)

This table breaks down the essential figures needed to assess a potential flip quickly. It's a simplified version, but it covers the core components you must account for.

| Metric | Example Value (£) | Description |

|---|---|---|

| Purchase Price | £150,000 | The price you pay for the property. |

| Stamp Duty (SDLT) | £7,000 | Assumes additional property rate. Varies by price. |

| Legal & Broker Fees | £3,500 | Solicitor, survey, and finance broker costs. |

| Renovation Budget | £25,000 | Includes materials, labour, and a contingency. |

| Holding Costs | £9,000 | Bridging interest, utilities, council tax for 6 months. |

| Total Costs In | £194,500 | The total cash required to buy and refurbish. |

| After Repair Value (ARV) | £240,000 | The realistic price it will sell for once renovated. |

| Selling Costs | £4,800 | Estate agent fees (e.g., 1.5% + VAT) and legal fees. |

| Gross Profit | £40,700 | ARV minus all costs before tax. |

| Capital Gains Tax (CGT) | £6,916 | Assumes higher-rate taxpayer after allowances. |

| Net Profit | £33,784 | The final profit in your pocket. |

This process shows that even a seemingly profitable deal has many layers of cost that can quickly erode your margin if not tracked meticulously.

This is where modern tools have completely changed the game. Instead of fighting with complex spreadsheets and risking a misplaced formula, you can use apps like DealSheet AI to automate the entire financial breakdown. Just paste in a property listing URL, and it instantly calculates every UK-specific cost and tax for you.

This gives you the clarity to make a fast, confident offer, eliminating the guesswork and costly human errors that could wipe out your entire profit. It's how the pros operate in today's fast-moving market.

Securing the Right Finance for Your Flip

Speed is everything when it comes to flipping property in the UK, and that urgency starts with your finance. Get it right, and you can pounce on a great deal, especially at auction. Get it wrong, and you can watch your profits get eaten alive before you've even picked up a paintbrush. Understanding your options here isn't just important—it's non-negotiable.

For most flippers, especially when buying a property that's in no state to get a standard mortgage, bridging loans are the default tool. They are short-term, asset-backed loans designed to "bridge" the gap between buying a property and either selling it on or securing long-term finance.

Understanding Bridging Loans

The killer feature of a bridging loan is speed. A good lender can get funds out the door in a matter of days. This is absolutely critical for hitting the tight 28-day completion deadlines you'll face at most UK property auctions. Unlike a traditional mortgage, the lending decision hinges more on the property's value (and its potential future value) than on your personal income slips.

Of course, that speed and flexibility come at a price. Interest rates are punchy, much higher than a standard mortgage, and they're typically charged monthly. On top of that, you have to account for arrangement fees, valuation fees, and legal costs. These numbers add up fast and have to be built into your deal analysis from the very first minute.

The real cost of a bridging loan is never the headline interest rate. It's the grand total of all fees and the rolled-up interest over the entire term. Getting this calculation wrong is one of the fastest ways to turn a profitable flip into a painful loss.

To dodge any nasty surprises, you have to model the total cost of borrowing with complete accuracy. For a detailed guide on how these costs stack up, check out our bridging loan calculator — it will help you see the real numbers before you commit.

Comparing Your Finance Options

While bridging is the go-to for many, it's not the only game in town. Depending on the state of the property and your own circumstances, other routes might be a much better fit.

- Cash Purchase: This is the dream scenario. Using cash is the fastest, simplest option. It makes you a hugely attractive buyer, gives you immense negotiating power, and completely removes finance costs, pushing your potential profit margin way up. The downside? It ties up a massive chunk of capital you can't deploy on other projects.

- Light Refurbishment Mortgages: If the property is habitable and just needs cosmetic work—think a new kitchen, bathroom, or a full redecoration—then a light refurb mortgage could be perfect. These products let you borrow against the property's current value and sometimes release funds in stages as you complete the work. They're slower to arrange than a bridging loan, but the interest rates are far, far lower.

- Auction Finance: Think of this as a specialised bridging loan, pre-packaged for auction buys. Some lenders will even offer a pre-approval, which gives you the confidence to bid knowing your funding is locked in, as long as the property and its legal pack tick their boxes.

Here's a quick way to think about the main funding routes:

| Finance Type | Best For | Speed | Cost |

|---|---|---|---|

| Bridging Loan | Unmortgageable properties, auction buys | Very Fast (days) | High |

| Cash Purchase | Maximum negotiating power | Instant | None (opportunity cost) |

| Refurbishment Mortgage | Habitable homes needing cosmetic work | Slow (weeks/months) | Low |

The right path depends entirely on the deal itself. For a complete wreck you've snagged at auction, a bridging loan is often your only realistic choice. For a tired but liveable probate sale, a refurbishment mortgage could save you thousands in interest payments.

Bidding at Auction with Confidence

Property auctions are a fantastic place to find deals, but they are absolutely unforgiving. When that hammer falls, you are legally bound to complete the purchase. This means you must have your finance lined up and your numbers nailed down before you even think about raising your hand.

Your first move is to get the legal pack from the auctioneer and send it straight to your solicitor for a thorough review. It contains everything you need to know about title deeds, searches, and any lurking legal issues. Never, ever bid on a property without your solicitor giving the legal pack the all-clear.

Next, you need to set a hard, non-negotiable maximum bid. This number isn't a guess; it's the result of the same detailed underwriting process we've been talking about. You need to work backwards from the property's After Repair Value (ARV), subtracting every single cost imaginable:

- Your target net profit.

- All selling costs (agent and legal fees).

- Your full renovation budget (plus a 10-15% contingency).

- All finance costs (interest, arrangement fees, the lot).

- All purchase costs (Stamp Duty, legal fees).

The number you're left with is your walk-away price. It's incredibly easy to get swept up in the heat of a bidding war in the auction room. Sticking to your pre-calculated limit is the single most important discipline for any flipping property UK investor to master. Going just a few thousand pounds over can obliterate your entire profit margin.

Smart Renovation Budgeting and Project Management

The renovation is where you physically add value to your property, but it's also a minefield where profits can instantly disappear. Get this bit wrong, and you'll quickly turn a promising deal into a costly lesson. A successful flip hinges on a renovation that's finished on time and, crucially, on budget.

Your approach to budgeting has to be meticulous and grounded in reality, not optimism. When you're flipping property in the UK, a vague estimate simply won't cut it; you need a detailed, line-by-line breakdown of every single anticipated cost.

Building a Bulletproof Renovation Budget

A profitable refurb starts with a budget that accounts for everything. Walk through the property, room by room, and list every task required. Be brutally honest about the real scope of work.

Your list must include:

- Structural Work: Any layout changes, wall removals, or major repairs to the roof or foundations.

- First Fix: All the hidden stuff – new wiring, plumbing, and central heating installation.

- Plastering: Skimming walls and ceilings to get that smooth, modern finish.

- Second Fix: Fitting doors, skirting boards, architraves, sockets, and light fixtures.

- Kitchen & Bathroom: The cost of units, worktops, appliances, sanitaryware, and tiling. These are your big-ticket items.

- Finishing Touches: Painting, decorating, flooring, and landscaping.

Once you have your list, it's time to get accurate quotes. Never, ever rely on a single price. You should aim for at least three written quotes from reputable, vetted tradespeople for each major job. This doesn't just give you a price comparison; it also offers insight into different approaches and potential issues you hadn't even considered.

Crucial Tip: Always build a contingency fund into your budget. We recommend setting aside 10-15% of your total renovation cost to cover the unexpected. Whether it's discovering hidden damp or a sudden spike in material costs, this buffer is what will save your project from financial ruin.

The Art of Project Management

A budget is useless without a plan to execute it. Effective project management is all about creating a clear roadmap and keeping everyone on track. This starts with a schedule of works—a logical timeline detailing the order in which tasks must be completed.

For example, the plastering can't happen until the new wiring and plumbing (First Fix) are in place. You can't lay the flooring until the plaster is dry. A clear schedule prevents costly delays and ensures a smooth workflow between different trades.

One of the biggest threats to any renovation project is scope creep. This is when small, unplanned additions and changes start to sneak into the project, gradually inflating the budget and pushing back the timeline. A classic scenario is deciding to add extra plug sockets after the walls have been plastered. This forces the electrician to return and the plasterer to patch up the damage—a simple change that costs both time and money.

To avoid this, lock in your design and specification before any work begins. Make your decisions on everything from the kitchen layout to the tile choices upfront. Any changes made mid-project must be carefully evaluated for their impact on both the budget and the schedule. For a deeper look at how these numbers can stack up, you can learn more about typical UK building costs per square metre in our detailed guide.

Maintaining Quality Without Overspending

When flipping property, the goal is to create a finish that appeals to the broadest range of potential buyers, not to build your personal dream home. Focus your spending on the areas that have the biggest impact on value: kitchens and bathrooms.

Here are some practical tips for managing your project effectively:

- Regular Site Visits: Be on-site regularly to check progress, answer questions, and spot any issues early.

- Clear Communication: Maintain an open line of communication with your trades. A quick daily chat can prevent misunderstandings that lead to expensive mistakes.

- Track Your Spending: Use a simple spreadsheet or app to log every single expense against your budget. This gives you a real-time view of your financial position and helps you stay in control.

Ultimately, a smart renovation is a balancing act. It's about spending money in the right places to add maximum value while maintaining strict control over every pound to protect your profit margin.

Getting Right with UK Tax and Legal

If there's one area that can turn a profitable flip into a nightmare, it's the tax and legal side. Getting this wrong doesn't just chip away at your profit; it can wipe it out completely. This isn't about box-ticking; it's about protecting every pound you've worked to earn.

To succeed in this game, you need to get fluent in the language of HMRC. From the moment you buy to the day you sell, every financial move is under the microscope. You have to be ready for Stamp Duty Land Tax (SDLT), Capital Gains Tax (CGT), and potentially even Income Tax if you're flipping frequently.

The First Hurdle: Stamp Duty Land Tax

Stamp Duty Land Tax (SDLT) is the first big bill you'll face. It's a tiered tax you pay when buying property in England and Northern Ireland, and for flippers, it has a particularly sharp sting.

If this flip is an additional property—meaning you already own a home—you'll be hit with the higher rate SDLT surcharge. This adds a hefty upfront cost that absolutely must be in your initial deal analysis. Forget to factor it in, and your entire budget is skewed before you've even picked up a paintbrush.

The rules can get tricky, so for a deeper dive, check out our guide on what is Stamp Duty Land Tax.

Your Profit: Is It Capital Gains or Income?

Once you sell the renovated property, the taxman will want his share of the profit. For most people flipping a property here and there, this profit falls under Capital Gains Tax (CGT).

You're taxed on the 'gain' – that's the difference between what you sold it for and your total costs (the purchase price, SDLT, legal fees, and all your renovation expenses). Everyone gets an annual CGT allowance, which is a slice of profit you can make tax-free each year. Anything above that gets taxed, with residential property gains hitting higher-rate taxpayers harder.

But here's a crucial distinction. If HMRC decides you're 'trading' properties—flipping them systematically as your main business—your profits could be subject to Income Tax and National Insurance instead. With Income Tax rates typically higher than CGT, this reclassification can have a massive impact on your final take-home profit.

It's a common myth that doing just one or two flips a year keeps you safe from being classed as a trader. HMRC looks at your intention, frequency, and how organised your flipping activity is. Don't guess – get proper advice from an accountant who lives and breathes property tax.

The Real-World Impact of UK Taxes on Profit

The numbers paint a stark picture of how thin margins have become for UK property flippers. Recent analysis shows that average gross profits have plummeted from around £38,000 in early 2022 to just £22,000 by the first quarter of 2025.

A huge part of this squeeze is down to a staggering 236% increase in SDLT over the last decade, coupled with soaring renovation costs. The reality bites even harder after tax: only 66% of flips are actually profitable once SDLT is paid. You can read more on how flipping profits have been hit by rising costs here.

Staying on the Right Side of the Law

Beyond the taxman, there are legal obligations you simply can't ignore. Any structural changes or significant alterations will almost certainly need building regulations approval from your local council. This process ensures the work is safe, structurally sound, and meets current energy efficiency standards.

And if you're planning to extend, change the property's use, or significantly alter how it looks from the outside, you're almost guaranteed to need planning permission.

Trying to dodge these legal hoops is a classic false economy. It can lead to massive fines, being ordered to undo all your hard work, and leaving you with a property that's legally unsellable. Always, always check with your local planning authority before you start knocking down walls.

Creating Your Exit Strategy for a Successful Sale

A renovated property is just an expensive, static asset until it's sold. Your profit is only ever realised on completion day, which is why a well-planned exit strategy is a non-negotiable part of flipping property in the UK. This final stage is all about squeezing every drop of value out of your hard work through smart marketing, pricing, and crucially, having a solid backup plan.

The final presentation of your property can add thousands to the sale price and dramatically shorten the time it sits on the market. High-quality, professional photographs are essential; they're the first thing buyers see online and can make or break their interest in a split second.

Likewise, professional staging helps buyers connect with the space on an emotional level. It allows them to genuinely visualise themselves living there, which often translates to faster, higher offers.

Pricing and Selling Your Flipped Property

Choosing the right asking price is a delicate balance. Price it too high, and you'll scare off viewers, leaving the property to go stale on the market. Price it too low, and you're leaving thousands of pounds of hard-earned profit on the table. Your only guide here is data: analyse recent sold prices of comparable renovated properties in the immediate area to set a realistic, attractive price point.

Your choice of estate agent is just as important. Don't just go with the one offering the cheapest fee. You need an agent with a proven track record of selling similar properties in your target postcode. A great agent will actively market your property, skilfully manage viewings, and negotiate effectively on your behalf. Don't be afraid to push back on their fee; a 1% plus VAT commission is a common starting point, but it's often negotiable.

Having a Plan B If the Market Shifts

Even the most meticulous plans can hit headwinds. What happens if the market takes an unexpected downturn and the property just isn't selling as quickly as you anticipated? This is where having a Plan B becomes absolutely critical.

A savvy investor never backs themselves into a corner. Your Plan B is your safety net, allowing you to turn a slow-moving asset into a cash-flowing one, protecting your capital for the long term.

If a quick sale proves difficult, your pivot is usually to refinance. By switching from an expensive bridging loan to a standard buy-to-let mortgage, you can rent the property out. This transforms the flip into a long-term investment that generates monthly income and gives the market time to recover before you attempt to sell again.

This isn't a last-minute decision. Understanding the potential rental income and running the numbers for this "rental" scenario should be a key part of your initial due diligence, right at the start. For more on this, explore our comprehensive guide on how to use a property ROI calculator in the UK to properly assess both flip and rental strategies from day one.

Your Top Flipping Questions, Answered

Let's cut straight to it. When you're starting out, a few key questions always come up. Here are the straightforward answers I wish I'd had when I started, based on real-world projects.

How Much Money Do I Actually Need to Start Flipping Houses in the UK?

There's no single magic number, but anyone telling you it's "no money down" is selling a dream. In reality, you need a serious chunk of cash to do this properly and safely.

You'll need enough capital for:

- The deposit (usually 25% for specialist finance like bridging loans).

- All the purchase costs – think Stamp Duty, solicitor fees, and survey costs.

- The entire renovation budget, paid upfront. You can't rely on the loan for this.

- A contingency fund of at least 10-15% of the refurb budget. Trust me, you'll need it.

Let's make that real. For a £150,000 property needing a £25,000 renovation, you should have access to somewhere between £70,000 and £80,000 in liquid cash. This gives you the buffer to handle unexpected issues without sleepless nights.

Is Flipping Property Still Worth It in the UK for 2026?

Yes, absolutely. But the game has changed. The days of buying any old property, giving it a quick lick of paint, and making a fortune on a rising market are long gone. The margins are much tighter now.

Profitability in 2026 comes down to two things: finding genuinely exceptional deals and executing your renovation with military discipline on costs. You have to be better than the average investor. Success now means unearthing undervalued properties that others have missed, knowing exactly how to add significant value without overspending, and tracking every single penny from start to finish.

Can I Flip a Property with Zero Experience?

Honestly, while it's technically possible, I'd strongly advise against it. Jumping straight into a complex, back-to-brick renovation as your first project is a recipe for disaster. It's a surefire way to lose money and your sanity.

A much smarter approach is to start small. Find a simple cosmetic refurbishment—something that needs a new kitchen, bathroom, and decoration. This teaches you the process, helps you build a network of reliable tradespeople, and lets you build confidence without taking on massive risk.

Your first project is your education. Focus on learning the ropes, even if it means a smaller profit. The experience you'll gain is invaluable.

Stop guessing and start analysing. DealSheet AI gives you the power to analyse any UK property flip in seconds, directly from your iPhone. Get clarity on every cost and tax to make smarter, faster investment decisions. Download the app and start your free trial today.