How to Flip Houses UK: A Step-by-Step Guide for Profit in 2026

How to Flip Houses UK: A Step-by-Step Guide for Profit in 2026

Learning how to flip houses UK for profit in 2026 requires mastering a simple but critical formula: buying the right property at a deep discount, executing a cost-effective renovation, and securing a swift, profitable sale. This guide provides the actionable blueprint for achieving exactly that. The key is to remove guesswork and make every decision based on solid data, which is why savvy investors now use tools like the DealSheet AI app to analyse a property's potential profit in seconds.

Your Blueprint For Profitable House Flipping In The UK

Let's be blunt: successfully flipping houses in the UK is tougher than ever. The market, squeezed by higher taxes and unpredictable material costs, demands a rock-solid strategy and precision from day one. The days of easy profits are long gone. Today's flipper has to be an analyst first and a renovator second.

The real core of a profitable flip isn't the grand design or the fancy kitchen finishes. It's locked in the moment you buy the property. Pay too much, or underestimate your costs, and you can wipe out your entire profit margin before you've even started. This is exactly why meticulous financial planning is completely non-negotiable.

Understanding The Modern Flipping Process

The journey of flipping a house can be broken down into three fundamental stages: Buy, Renovate, and Sell. Each phase comes with its own unique challenges and opportunities that you have to manage carefully to protect your bottom line.

True success requires a deep understanding of not just renovation, but also deal sourcing, financing, and the all-important tax implications. If you're just starting out, it's vital to get your head around what property sourcers need to deliver and how to stand out—this is how you find those undervalued gems in the first place.

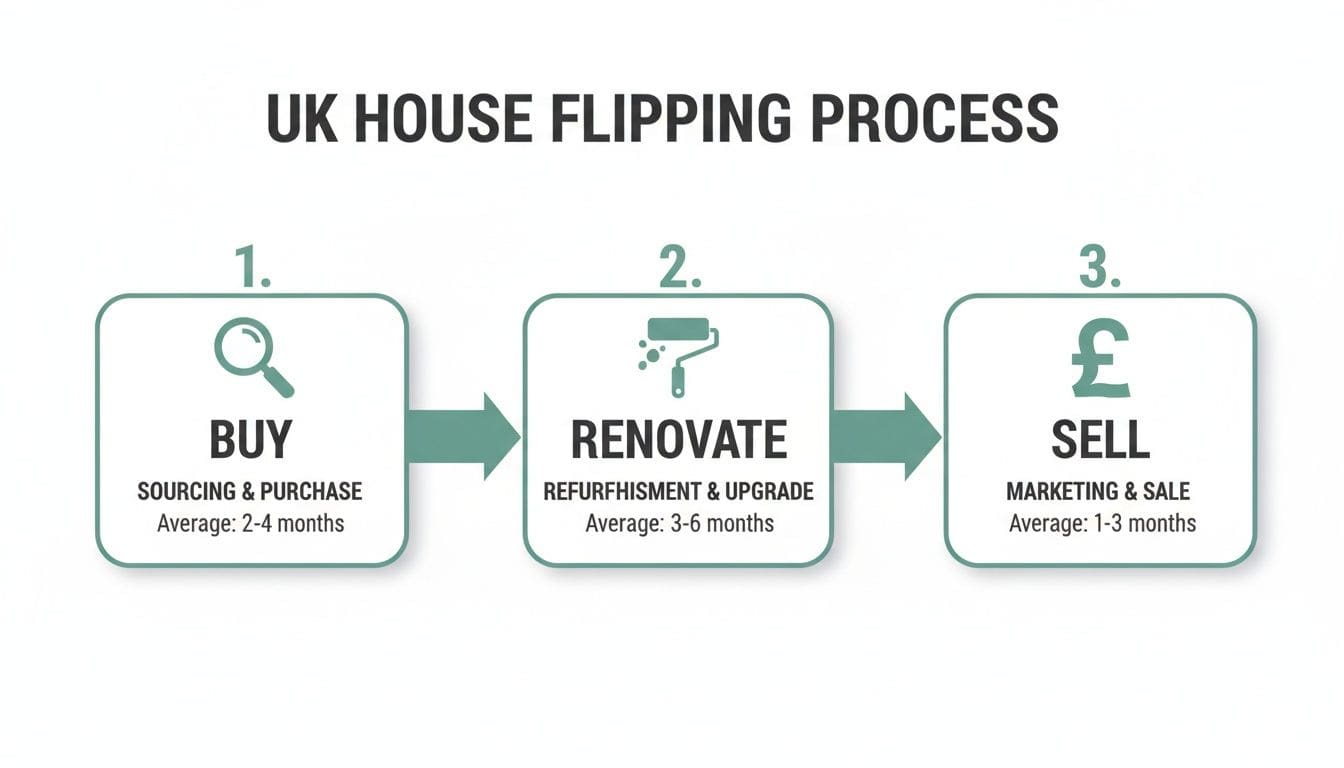

This visual below lays out the simple, yet critical, flow of a typical UK house flip.

The graphic above summarises the core journey, but it's the detail behind the stages that makes or breaks a project.

The UK House Flipping Process at a Glance

This table provides a high-level overview of the key stages and what you need to focus on to get them right.

| Stage | Key Objective | Critical Success Factor |

|---|---|---|

| Buy | Acquire an undervalued property with clear potential for value-add. | Accurate underwriting and securing the property at the right price. |

| Renovate | Execute a targeted renovation on time and within budget to maximise the property's market value. | Strict budget control and efficient project management. |

| Sell | Achieve a quick, profitable sale at the target price through effective marketing and negotiation. | Understanding the local market and pricing the property correctly for a fast exit. |

As the table shows, each step is sequential and completely dependent on the last; a mistake in the buying phase will inevitably cascade into the renovation budget and demolish your final sale price. Mastering this workflow is the first step towards consistent profitability in today's market.

Finding and Funding Your Next Flip

Here's the first and most important rule in property flipping: you make your money when you buy, not when you sell. Get this wrong, and the whole project is compromised. Overpaying by even a few thousand quid can vaporise your profit margin before you've even picked up a hammer.

Finding the right deal is a game of strategy, speed, and frankly, a bit of old-fashioned networking. Your search has to go way beyond the standard Rightmove alerts that every other wannabe flipper is watching. The real opportunities are often lurking where others aren't looking. This means building genuine relationships with local, independent estate agents—the ones who hear about a probate sale or a motivated seller before the property ever hits the open market.

Sourcing Deals Beyond The Obvious

To find properties with genuine, profitable potential, you absolutely have to diversify your sourcing channels. Relying on one method is just a recipe for frustration and paying too much in a competitive market.

Here are a few proven strategies that consistently unearth undervalued properties:

- Property Auctions: The classic hunting ground for fixer-uppers, repossessions, and probate sales. Auctions demand quick, decisive action and having your finance sorted beforehand, but they can be a goldmine for discounted properties if you know what you're doing.

- Direct-to-Vendor Marketing: This means reaching out to homeowners directly, maybe through targeted leaflets or focused online ads. It's a longer game, for sure, but it lets you negotiate without agents in the middle, which can often lead to a better price.

- Networking with Sourcers: A good property sourcer can be worth their weight in gold, bringing you deals that perfectly match your criteria and saving you a huge amount of time. Just remember to always, always do your own due diligence on any deal they bring to the table.

The secret to successful sourcing is relentless consistency. You have to dedicate time every single week to calling agents, scanning auction catalogues, and chasing down potential off-market leads. It's a numbers game—the more stones you turn over, the more likely you are to find that hidden gem.

The geography of flipping has also changed dramatically. Smart investors are increasingly looking north for better value and healthier returns. Recent data shows a massive northward shift in flipping activity across England and Wales, with 61% of flipped properties now located in the Midlands, the North of England, or Wales. The North East has become a real hotspot, with flipping activity more than double the national average. You can read more about these property market trends on Hamptons.co.uk. This trend really hammers home the importance of analysing regional markets to find the best pockets of opportunity.

Securing The Right Finance For Your Flip

Once you've found that promising deal, you need to fund it—and quickly. Your standard residential mortgage just won't work for a run-down, unmortgageable property or a deal that needs to complete in 28 days. This is where specialist finance becomes your best friend.

Bridging loans are the go-to tool for most property flippers. They are short-term loans designed to 'bridge' the financial gap between buying a property and then either selling it on or refinancing it onto a long-term mortgage.

Their main advantages are pretty compelling:

- Speed: A bridging loan can often be arranged in a matter of days. This is absolutely critical for securing auction properties or snapping up off-market deals where the seller wants a fast, no-fuss sale.

- Flexibility: Lenders are more interested in the property's future value (the 'exit') than your personal income statements. They're comfortable lending on properties in a poor state of repair that high street banks wouldn't touch.

Of course, this speed and flexibility comes at a cost. Bridging finance has higher interest rates and fees than traditional mortgages, so you have to model these costs with pinpoint accuracy to make sure your project stays profitable. To get a handle on these numbers, you can use our bridging loan calculator to run different scenarios on your next potential deal.

Joint Ventures (JVs) are another fantastic way to fund a flip, especially if you're just starting out and are a bit light on cash. This involves partnering with someone who has the capital, while you bring the deal-sourcing skills, the vision, and the time to manage the project. A typical JV might split the profits 50/50 after the funding partner gets their initial investment back.

This approach massively reduces your personal financial risk, but it absolutely requires a rock-solid legal agreement and complete trust between you and your partner. The success of any JV boils down to crystal-clear communication and a shared vision from day one.

Mastering the Numbers: From Budget to Renovation

Let's be brutally honest. A property flip is won or lost on a spreadsheet long before the first wall comes down. Getting the numbers wrong is the fastest way to turn a promising project into a financial nightmare. Your budget is the blueprint for your profit, and it needs to be ruthlessly detailed.

This means you have to look far beyond the headline purchase price. You need to account for every single cost that will eat into your margin, from the taxman's share to the final lick of paint. This meticulous approach is what separates the seasoned pros from the hopeful amateurs left wondering where their profit vanished.

Dissecting The True Purchase Costs

The price you agree with the seller? That's just the starting line. A host of other substantial costs kick in immediately, and underestimating them can cripple your project from the get-go.

First up is the big one: Stamp Duty Land Tax (SDLT). For anyone learning how to flip houses in the UK, this is a critical and often painful expense. Since you're buying an additional property, you'll be hit with the higher rate of SDLT, which slaps a significant surcharge on top of the standard rates.

This tax burden has become a massive hurdle for flippers. In fact, flipping activity in England and Wales has slumped to its lowest point in over a decade, driven largely by rising stamp duty and stagnant house prices. The average SDLT bill for a flipper has climbed to a hefty £11,920, which now consumes a staggering 30% of gross profit before a single hammer is swung. It's a stark reminder of just how crucial it is to factor this in accurately.

Beyond SDLT, your initial outlay must cover:

- Legal Fees: Budget for conveyancing solicitors for both the purchase and the eventual sale.

- Financing Costs: If you're using a bridging loan, this includes arrangement fees, valuation fees, lender's legal fees, and the monthly interest payments.

- Survey and Insurance Costs: A structural survey is non-negotiable for older properties, and you'll need unoccupied property insurance from day one.

Building An Iron-Clad Renovation Budget

Once you've nailed down the purchase costs, the focus shifts to the renovation. This is where budgets can spiral out of control without a disciplined approach. Vague estimates won't cut it; you need a detailed scope of works.

This document should list every single job, from ripping out the old kitchen to the final decorating touches. Go room by room, trade by trade. This level of detail is essential for getting accurate quotes from contractors and for tracking your spending as the project moves forward.

A good scope of works acts as your project's constitution. It ensures you and your builder are on the same page, preventing misunderstandings and the dreaded "scope creep" where extra jobs get added, blowing your budget and timeline out of the water.

Your contingency fund isn't an optional extra; it's a non-negotiable part of your budget. Aim for at least 15-20% of your total renovation cost. This is your safety net for the inevitable surprises an old property will throw at you, like hidden damp or faulty wiring.

When estimating build costs, you have to be realistic. For a much more detailed breakdown to help you form an accurate picture of what your renovation is likely to cost, you can check out our guide on building costs per square metre.

To give you a clearer idea of where the money goes, here's a sample budget breakdown for a typical UK flip.

Typical Flip Budget Breakdown (Sample Project)

| Cost Category | Example Cost (£) | Percentage of Total Budget | Notes |

|---|---|---|---|

| Purchase Costs | £15,000 | 25% | Includes SDLT (higher rate), legal fees for purchase, survey, and initial insurance. |

| Financing Costs | £9,000 | 15% | Arrangement fees for a bridging loan, valuation, and 6 months of interest payments. |

| Renovation - Labour | £15,000 | 25% | Covers all trades: builder, plumber, electrician, plasterer, decorator. |

| Renovation - Materials | £9,000 | 15% | Kitchen, bathroom suite, flooring, tiles, paint, windows, doors. |

| Contingency Fund | £6,000 | 10% | 15% of the total renovation budget (£40k). Crucial for unexpected issues. |

| Holding & Selling Costs | £6,000 | 10% | Council tax, utilities during the project, estate agent fees, and sale conveyancing. |

| Total Project Budget | £60,000 | 100% | This is the total capital required on top of the property purchase price. |

Remember, these percentages are just a guide. A project needing heavy structural work will see the labour and materials share increase, while a simple cosmetic refresh will have lower renovation costs. The key is to map out your specific project with this level of detail.

Vetting Contractors And Managing The Build

Finding a reliable contractor is one of the most stressful parts of a flip, but it's absolutely essential for success. Never, ever go with the cheapest quote without doing thorough due diligence.

Here's a simple vetting process I stick to:

- Get Multiple Quotes: Aim for at least three detailed quotes based on your specific scope of works.

- Check References: Don't just ask for them—actually call previous clients. Ask about their communication, quality of work, and whether they stuck to the budget and timeline.

- Visit a Previous Project: If you can, ask to see a completed job. It's the best way to assess their standard of finish.

- Verify Insurance: Make sure they have adequate public liability insurance. No excuses.

Once you've chosen your team, agree on a payment schedule tied to specific project milestones. Never pay for large amounts of work upfront. This structure incentivises progress and protects your cash flow. Regular site visits and clear communication are key to keeping the project on track and ensuring the quality meets your standards.

Navigating Permissions and Regulations

Finally, don't get caught out by red tape. Understanding planning permission and building regulations is crucial if you want to avoid costly delays and legal headaches down the line.

-

Planning Permission: This is all about the external appearance and use of a building. Most internal cosmetic changes won't need it. But major work like a significant extension, changing the building's use, or altering the exterior in a conservation area almost certainly will.

-

Building Regulations: These cover the health and safety side of construction—things like structural stability, fire safety, and energy efficiency. Most renovation work, including new windows, a full electrical rewire, or moving a bathroom, will need to be signed off by building control.

Always check with your local council's planning department before starting any major work. Getting this wrong can result in being forced to undo completed work at your own expense—a total disaster for any flip's budget and timeline.

Executing a Flawless Exit Strategy

After months of dust, tough decisions, and disciplined spending, the exit is where all your hard work finally pays off. But don't get complacent. A clumsy exit can shave thousands off your profit margin, undoing all the value you've painstakingly created.

Getting a fast, profitable sale isn't about luck. It's a methodical process designed to attract the right buyers and achieve the best possible price. The final sale is the culmination of every decision you've made on your journey of learning how to flip houses uk. This is the moment to execute with absolute precision.

Staging For A Swift Sale

An empty, freshly renovated house can feel surprisingly small and sterile. Your job is to help potential buyers emotionally connect with the property, to see it as their future home. This is where professional home staging becomes one of the smartest investments you can make in the final stretch.

Staging isn't just about plonking some furniture down. It's about creating a lifestyle narrative that speaks directly to your target buyer. It demonstrates the scale of each room and shows exactly how the space can be used, removing guesswork and making the home feel instantly liveable.

Alongside staging, high-quality professional photography is completely non-negotiable. These images are your property's first impression online, and they need to be good enough to stop someone mid-scroll. Poorly lit smartphone snaps will get you ignored; professional shots will drive viewing requests through the roof.

Selecting Your Sales Team and Setting The Price

Choosing the right estate agent is a critical business decision, not an afterthought. Don't just go with the one who gives you the highest valuation. Look for an agent who is genuinely motivated, has a strong track record selling similar properties in the area, and presents a clear, proactive marketing strategy.

A good agent will:

- Have a database of active, qualified buyers ready to view your property immediately.

- Provide realistic, data-backed pricing advice designed to attract immediate interest.

- Offer concrete plans for marketing that go beyond a simple listing on Rightmove and Zoopla.

Pricing is a delicate balance. Go in too high, and the property will sit on the market, gathering dust and looking stale. Go in too low, and you're just leaving money on the table. The sweet spot is a price competitive enough to generate a flurry of early viewings. This creates urgency and competition among buyers, often leading to offers at or even above the asking price.

Building Resilience With A Plan B

So, what happens if the market takes an unexpected nosedive just as you're ready to sell? A savvy investor always has a contingency plan. Relying solely on a quick sale exposes you to massive market risk. Your Plan B is your safety net.

The most common and effective alternative is to rent the property out. This strategy, often part of a BRRR (Buy, Refurbish, Refinance, Rent) model, turns your flip into a cash-flowing asset. The key is that you must have analysed the deal from both a flip and a rental perspective right from the very beginning.

Having a solid Plan B isn't admitting defeat; it's a sign of a professional, resilient property business. It allows you to wait out a slow sales market while the property generates income, giving you the flexibility to sell when conditions improve.

Pivoting to a rental does come with its own financial and legal hurdles. You'll need to refinance from your expensive bridging loan onto a standard buy-to-let mortgage. Lenders will assess the property's rental income to ensure it meets their stress-testing criteria, which typically requires the rent to cover 125-145% of the mortgage payment.

You'll also need to consider the tax implications, like income tax on rental profits and potential changes to your Stamp Duty position. To get your head around these obligations, you can explore our guide on what is Stamp Duty Land Tax. A well-executed rental exit can turn a potential loss into a profitable long-term investment.

Managing Risk in a Volatile Market

Flipping property in the UK can be hugely rewarding, but ignoring the risks is a fast track to financial disaster, especially when the market's this choppy. The days of easy profits are long gone. We're now in a climate where sharp risk management isn't just a good idea—it's essential for survival.

Learning how to flip houses successfully in the UK today means becoming an expert in spotting trouble before it starts. It's about identifying threats to your budget, timeline, and profit before they materialise and having a solid Plan B ready to go. A single unforeseen problem can, and often does, wipe out an entire profit margin.

The Reality of Squeezed Profit Margins

First things first: you have to be brutally realistic about the numbers from day one. The profitability of house flipping has tightened significantly. Average gross profits have plummeted by 42%, falling from around £38,000 in early 2022 to just £22,000 in the first quarter of 2025.

This isn't a blip; it's a trend. The average gross profit margin for flippers dropped from 17% back in Q1 2015 to a mere 10% in Q1 2025, a shift driven by everything from policy changes to soaring costs. You can dig into the data behind these property flipping profitability trends on Property Portfolio Investor. I'm not showing you these figures to put you off, but to hammer home just how precise your deal analysis needs to be. There's no room for guesswork.

Identifying and Mitigating Key Threats

Your success hinges on your ability to see the common threats coming and neutralise them before they hit your bottom line. Let's break down the big three and the practical tactics you can use to protect your project.

Renovation Cost Overruns

This is the big one. It catches out new and experienced flippers alike. An old property is a treasure chest of expensive surprises, from hidden damp and rotten joists to ancient wiring that needs a complete overhaul.

-

The Fix: Your 15-20% contingency fund is completely non-negotiable. This should be calculated as a percentage of your total renovation budget and ring-fenced from the start. Don't even think about touching it for anything other than genuine, unforeseen project costs.

-

The Fix: Get multiple, highly detailed quotes based on an exhaustive scope of works. A vague, one-line quote is a massive red flag. You want a breakdown that itemises labour and materials, giving you a clear baseline to hold your contractor accountable to.

Project Delays and Timeline Blowouts

Time really is money, especially when you're paying eye-watering interest on a bridging loan. Delays caused by unreliable trades or supply chain issues will chew through your profits faster than anything else.

-

The Fix: Pre-vet your backup trades. Before the project even begins, have the contact details of a second-choice electrician, plumber, and plasterer who you know are reliable. If your main guy lets you down, you can pivot fast without losing weeks scrambling for a replacement.

-

The Fix: Order materials with long lead times—think windows, specialist kitchen fittings, or bespoke doors—the moment the purchase completes. Don't wait until the builder is standing there asking for them.

A project timeline is a management tool, not a hopeful guess. Build in buffer periods between the key stages. For example, always allow a full week after plastering for it to dry out completely before the decorators are even booked to start. Rushing the sequence will only force you into costly rework down the line.

A Cooling Sales Market

You can control your budget and your build, but you have no control over the wider property market. A sudden dip in buyer confidence or another interest rate hike can leave you struggling to sell at your target price.

-

The Fix: Do your homework on local sales data before you even think about buying. Look at the average time properties are on the market and, crucially, the gap between asking prices and actual sold prices. This paints a real-world picture of local demand.

-

The Fix: Always have a Plan B. As we've discussed, your best alternative exit is often to rent the property out. This means you absolutely must analyse the deal as both a flip and a potential rental right from the outset. For a deeper dive into this kind of financial modelling, check out our complete guide to analysing UK buy-to-let deals. This dual-analysis approach is what builds real resilience into your investment.

Got Questions About Flipping Houses in the UK?

Even with the best guide in hand, you're bound to have questions. Flipping property isn't a paint-by-numbers game. This is where we tackle the most common queries I hear from both new and seasoned flippers, giving you straight answers for the market we're in right now.

How Much Money Do You Really Need to Flip a House in the UK?

There's no magic number here. The cash you need is tied directly to where you're buying and how big the project is. But we can break down the essential pots of money you'll need to have lined up.

First, you've got the deposit. For specialist finance like bridging loans, you'll typically need 25% of the purchase price. Then, you absolutely must have the cash ready for Stamp Duty Land Tax (SDLT), all your legal fees, and the entire renovation budget.

So, what's a realistic starting figure? For a lower-value property up in the North East, you might get started with around £40,000 to £60,000. Try to do a similar project down in the South East, and that number could easily rocket past £150,000. The one non-negotiable, wherever you are, is your contingency fund. You need at least 15-20% of your total refurb budget set aside. Trust me, old properties always have a few expensive surprises hiding in the walls.

Is House Flipping Still Worth It in the UK for 2026?

Yes, you can absolutely still make good money flipping property, but the game has completely changed. The days of making easy profits just by riding a rising market are long gone. Success in 2026 is all about a much sharper, more analytical approach.

Your profitability now boils down to three core skills:

- Buying at a serious discount: The old saying is true – you make your money when you buy. You have to find properties that are genuinely undervalued.

- Controlling every pound: You need to manage your renovation budget with military precision. Every penny you save on the refurb goes straight to your bottom line.

- Picking the right location: The most viable flips are now found in areas with lower purchase prices, like the North East, where the sting of SDLT is a little less painful.

Higher borrowing costs and hefty taxes mean your initial deal analysis has to be watertight. Using data to make decisions isn't just a "nice-to-have" anymore; it's an essential part of the modern flipper's toolkit.

Does the 70% Rule Work for the UK Market?

The 70% rule is a popular American guideline that says you should pay no more than 70% of the property's After Repair Value (ARV), minus the repair costs. While it can be a quick, back-of-a-fag-packet check, it's far too simplistic and downright dangerous to rely on in the UK.

Relying on the 70% rule in the UK is a recipe for a costly mistake. It creates a false sense of security by completely ignoring the unique and substantial costs that define our market.

The rule's biggest weakness? It fails to account for our specific transaction costs, which can completely wipe out a profit margin. It totally ignores:

- Stamp Duty Land Tax (SDLT): This is a massive upfront cost, especially with the second-property surcharge.

- Legal & Financing Fees: Conveyancing, bridging loan arrangement fees, and monthly interest payments are significant chunks of cash.

- Holding & Selling Costs: Don't forget council tax, utilities, and estate agent fees. They all add up.

Instead of a blunt instrument like the 70% rule, UK flippers must run a detailed deal analysis. You have to subtract all your purchase, holding, renovation, and selling costs from your projected ARV. It's the only way to figure out a true Maximum Allowable Offer (MAO) that actually protects your profit.

What Taxes Do I Pay When Flipping a House?

You'll get hit with tax at both the start and the end of a flip. When you buy, you're liable for Stamp Duty Land Tax (SDLT), and since it's an additional property, you'll be paying the higher surcharge rate.

When you sell, the profit you make is taxable. The crucial thing to grasp is that HMRC sees flipping as trading activity, not property investing. This has huge implications.

Your profit is treated as income. If you're operating as a sole trader, it's subject to your personal Income Tax rate (currently 20%, 40%, or 45%). If you flip through a limited company, the profit gets hit with Corporation Tax. And here's the kicker: because it's trading income, you cannot use your annual Capital Gains Tax allowance to reduce the bill. My best advice? Always talk to a specialist property accountant to make sure your deals are structured as tax-efficiently as possible from day one.

Ready to analyse your next deal with speed and accuracy? The DealSheet AI app replaces guesswork with data, allowing you to analyse a potential flip in under 60 seconds, complete with UK-specific costs like SDLT. Stop building fragile spreadsheets and start making smarter, faster investment decisions. Download the app and start your free trial today at https://apps.apple.com/gb/app/dealsheet-ai/id6756220992.