A UK Developer's Guide to Property Development Finance Options in 2026

A UK Developer's Guide to Property Development Finance Options in 2026

Navigating the world of UK property development finance options is make-or-break for any project in 2026. The key is to understand that your funding structure—from traditional senior debt to more complex solutions like mezzanine finance—directly dictates your project's viability and profitability. This guide breaks down the main funding routes, including senior debt, mezzanine finance, and government-backed schemes, to help you build the optimal capital stack for your next UK development. To get your numbers straight from the start, you need a robust financial model; use the DealSheet AI app to instantly analyse finance costs and project feasibility—download it now and start your free trial.

A High Level Overview of Funding Types

The first step in building a successful capital stack is understanding the core property development finance options available in the UK. Each funding route exists for a different reason, carries its own risk profile, and is designed for specific project scales and developer experience levels.

You've got the most common and lowest-cost senior debt at one end, and more complex equity partnerships at the other. The path you choose will directly hit your leverage, costs, and, most importantly, your project's profit. Getting a clear grasp of these differences is essential.

The Shifting Lender Landscape in 2026

The UK's lending environment has changed a lot, and that affects how developers get funding. Fresh data from Bayes Business School shows new commercial real estate lending hit £22.3 billion in the first half of 2025, with development finance making up a healthy 22% of that.

Here's the crucial part: debt funds now provide around 57% of commercial development finance. They've overtaken traditional banks, marking a major shift in the market. You can discover more insights from the Bayes commercial real estate lending report to see the full picture. This shift means developers have more choice, but it also means you have to understand the very different terms and risk appetites of these newer players.

Remember, the funding you pick touches every financial metric of your project. For a deeper dive into the numbers that matter, check out our guide on how to calculate property yield.

Comparing Your Main Finance Options

To make the initial decision-making a bit easier, the table below gives a quick, high-level comparison of the most common funding routes. Think of it as a cheat sheet to summarise their key features, helping you see which options are most relevant for your project before we get into the nitty-gritty of each one.

High-Level Comparison of UK Development Finance Options

| Finance Type | Typical LTC | Risk and Cost Profile | Ideal Use Case |

|---|---|---|---|

| Senior Debt | 50% - 65% | Lowest cost, lowest risk. | Standard, lower-risk projects with experienced developers. |

| Mezzanine Finance | 65% - 85% | Higher cost, medium risk. | Bridging the gap between senior debt and developer equity. |

| Equity Finance | 90% - 100% | Highest cost (profit share), highest risk. | Projects where the developer has limited capital to contribute. |

| Stretched Senior | 70% - 75% | Medium cost, medium risk. | Simplifying the capital stack by blending senior and mezzanine. |

This table gives you a starting point. Now, let's break down what each of these actually means for your bottom line.

Securing Senior Debt for Your Project

When it comes to property development finance options in the UK, senior debt is the bedrock. Think of it as the main, largest, and most secure loan in your project's funding structure. It always takes 'first charge' over the asset, which is just legal speak for saying the senior lender gets paid back first if things go wrong and the property has to be sold.

While high street banks used to be the go-to, the market is now a mix of challenger banks and specialist debt funds, each with a different view on risk. Getting to grips with how senior debt is structured isn't optional for a serious developer; it's the foundation of your entire financial model.

Understanding Typical Terms and Costs

When you pitch your project to a lender, they'll scrutinise it against a few key metrics. The big one is the Loan-to-Cost (LTC) ratio, which usually lands somewhere between 50% and 65%. This is the percentage of the total project cost the lender will cover, leaving you to find the rest from your own equity.

Interest rates are nearly always variable, quoted as a margin over a benchmark rate. In the UK, that benchmark is now the Sterling Overnight Index Average (SONIA). So, you might see a rate like 'SONIA + 6%', meaning your actual interest cost moves up and down with the market.

But interest is only part of the story. You absolutely have to factor in the fees:

- Arrangement Fee: This is for setting up the loan and is usually 1-2% of the total facility, paid upfront.

- Exit Fee: A fee charged when you repay the loan, often 1-2% of the loan amount itself or sometimes a slice of the Gross Development Value (GDV).

- Monitoring Fees: Lenders will appoint an independent monitoring surveyor to keep an eye on progress, and their costs are passed on to you.

Key Insight: Don't get fixated on the headline interest rate. The real cost of senior debt is a combination of interest plus arrangement, exit, and monitoring fees. You must model all of these to know what you're really paying.

Worked Example: A Small Residential Scheme

Let's put this into practice. Imagine a small residential project with a total cost (land and build) of £1,000,000.

A senior debt lender agrees to fund the scheme at 60% LTC over an 18-month term.

- Total Project Costs: £1,000,000

- Senior Debt Loan (60% LTC): £600,000

- Developer Equity Required: £400,000

Now for the finance costs, using typical terms:

- Arrangement Fee: 2% of the £600,000 loan = £12,000

- Interest: Let's assume an average drawn balance of £300,000 over the 18 months at 8% (e.g., SONIA + 6%). The interest would be roughly £36,000.

- Exit Fee: 1% of the £600,000 loan = £6,000

In this scenario, your direct finance costs come to £54,000 (£12,000 + £36,000 + £6,000), and that's before you've even paid the monitoring surveyor. This quick calculation shows that nearly 10% of your loan can be eaten up by finance charges alone, which hammers home why accurate financial modelling is so important.

For short-term or phased funding needs, a specialised bridging loan calculator can help you model these costs with more precision.

The Importance of Covenants and Monitoring

Getting the money is just the start. Your loan agreement will be packed with covenants – conditions you have to stick to throughout the build. These might include keeping a certain amount of cash as a contingency, submitting regular progress reports, or hitting specific construction milestones on time.

The lender's monitoring surveyor isn't just a box-ticker; they are the lender's eyes and ears on your site. They'll visit regularly (usually monthly) to verify progress and sign off on your next drawdown of funds. A good, transparent relationship with the surveyor is vital for keeping cash flowing.

Fall foul of your covenants, and you could find yourself in default, which gives the lender the right to step in and take control of the project. It's serious stuff.

Using Mezzanine Finance to Increase Leverage

So, your senior debt lender has offered a facility covering 65% of your project's costs, but that still leaves a hefty funding gap. This is the exact scenario where mezzanine finance enters the conversation. Think of it as a second, smaller loan that slots in right above your own equity but sits behind the senior lender in the repayment queue.

This type of funding is technically a form of subordinated debt, which is a fancy way of saying it's riskier for the lender. To protect themselves, they'll take a second legal charge over the property. Because they're second in line to get paid back if things go south, they charge a much higher price for their money.

The Cost Versus the Benefit

The main reason to even consider mezzanine finance is simple: higher leverage. By layering in a mezzanine piece, you can often push your total borrowing up to 85% LTC, and sometimes even a little higher. This drastically cuts down the amount of your own cash you need to commit to a deal, freeing up your capital to get other projects moving.

But this leverage doesn't come cheap. Not by a long shot. Interest rates for mezzanine finance in the UK typically fall in the 12% to 20% per annum range. This is not a loan you want hanging around for any longer than absolutely necessary, as the interest costs can quickly eat into your project's profit margin.

Key Takeaway: Mezzanine finance is a strategic scalpel, not a sledgehammer. It's best suited for projects with a healthy profit margin that can comfortably absorb the high finance costs, or for experienced developers looking to scale their operations by running multiple projects at once.

Worked Example: How Mezzanine Finance Works

Let's go back to our £1,000,000 total cost project. Without mezzanine, you were on the hook for £400,000 of your own equity. Now, let's see what happens when we add a mezzanine loan into the capital stack.

- Total Project Costs: £1,000,000

- Senior Debt (60% LTC): £600,000

- Mezzanine Loan (25% of Costs): £250,000

- Total Debt: £850,000 (which is 85% LTC)

- Developer Equity Required: £150,000

Just like that, your required equity has plummeted from £400,000 to just £150,000. That's the real power of mezzanine finance. But what does that £250,000 loan actually cost over the same 18-month term?

- Arrangement Fee (2%): £5,000

- Interest (at 15%): Assuming an average drawn balance, the interest would be roughly £28,125.

- Exit Fee (1%): £2,500

The extra finance cost for just this layer is £35,625. Add that to the senior debt cost of £54,000, and your total finance bill climbs to nearly £90,000. The crucial question you have to answer is whether freeing up £250,000 of your capital is worth paying an extra £35,625 in fees and interest. For fast-moving projects like flips, where speed and leverage are everything, this trade-off often makes perfect sense. Our detailed guide to property flipping in the UK digs into strategies where this kind of funding can be a game-changer.

Navigating the Intercreditor Agreement

A critical—and often tricky—part of using mezzanine finance is the intercreditor agreement. This is the legal document that sets out the rules of engagement between the senior and mezzanine lenders. It dictates the precise order of repayment and spells out exactly what happens in a default scenario.

The senior lender will always want to make sure their position is rock-solid, which can lead to some drawn-out negotiations. This agreement is non-negotiable, and its terms can have a real impact on how you manage the project day-to-day. It is absolutely vital to get experienced legal advice when navigating this process to ensure the terms are workable and don't tie your hands with unreasonable constraints.

Evaluating Alternative and Hybrid Funding Models

While the classic senior debt and mezzanine stack is a well-trodden path, it's far from the only way to fund a development project in the UK. Many developers, particularly those who value simpler legal setups and higher leverage from a single lender, are now looking at a range of alternative and hybrid models. These products effectively blend different finance types into one, more streamlined solution.

One of the most popular alternatives is the 'stretched senior' loan. Offered by specialist lenders and nimble debt funds, these loans roll the function of senior and mezzanine finance into a single facility. The beauty of this is its simplicity: one set of legal fees, one monitoring surveyor, and one point of contact. It cuts out a huge amount of administrative headache. A stretched senior loan can often reach up to 75% of the total project cost, covering a major chunk of your funding needs with just one agreement.

Stretched Senior vs Senior Plus Mezzanine

The all-in-one structure of a stretched senior loan is its main draw, but how does it stack up on cost against a traditional senior and mezzanine package?

Although the blended interest rate on a stretched product will naturally be higher than a standalone senior loan, it's often cheaper than the total cost of managing two separate facilities. Once you factor in two sets of legal and professional fees, the numbers can swing in favour of the simpler option. The reduced complexity alone is a massive win, especially for small to medium-sized developers. Trying to manage an intercreditor agreement between two different lenders can become a complex and drawn-out affair; a stretched senior loan sidesteps that problem entirely.

For more on navigating these kinds of multi-layered funding structures, our guide on structuring complex deals is a great place to start.

To really see the difference, let's run the numbers on a project with a total cost of £1,000,000. The table below compares the two main structures.

Worked Example Comparing Stretched Senior vs Senior Plus Mezzanine

| Metric | Structure 1: Senior + Mezzanine | Structure 2: Stretched Senior |

|---|---|---|

| Total Project Cost | £1,000,000 | £1,000,000 |

| Total Loan Facility | £850,000 (85% LTC) | £750,000 (75% LTC) |

| Developer Equity | £150,000 | £250,000 |

| Combined Finance Cost | ~£90,000 | ~£75,000 |

| Complexity | High (Two lenders, intercreditor) | Low (One lender, one agreement) |

The example really brings the trade-off into focus. A senior plus mezzanine stack gives you maximum leverage, which means you need less of your own cash in the deal. However, the stretched senior loan, while requiring more equity upfront, can be significantly cheaper and far, far simpler to manage. Your choice really boils down to what you value more: preserving your capital or saving on costs and complexity.

Exploring Other Innovative Funding Routes

Beyond stretched senior, a few other innovative property development finance options have emerged to suit different project scales and developer appetites.

-

Peer-to-Peer (P2P) Lending: This model cuts out the traditional bank, connecting developers directly with a crowd of individual investors through an online platform. P2P tends to be a great fit for smaller residential projects, usually those with a Gross Development Value (GDV) under £2 million. While it can offer competitive rates and flexible terms, don't assume it's a soft touch—the due diligence process is often just as rigorous as any traditional lender's.

-

Joint Venture (JV) Equity Finance: With a JV, you're not taking on debt; you're bringing in a partner. An equity investor provides a huge chunk, or sometimes all, of the cash you need. Instead of charging interest, they take a share of the project's profit—often around 50%. This can be a fantastic route for highly experienced developers who have a solid track record but are short on personal capital. The whole game is about finding a partner whose ambitions and risk appetite match your own.

Expert Tip: When you're considering a JV, remember you're shifting from managing debt to managing a partnership. Your proposal has to sell the project's profit potential, not just its viability. The legal agreement needs to be absolutely watertight, clearly setting out roles, responsibilities, and exactly how the profit will be split. A poorly structured JV is a recipe for disputes that can sink the entire project.

Tapping into Government-Backed Finance Schemes

For residential developers in the UK, particularly small and medium-sized outfits, government-backed finance is a powerful—and often overlooked—funding route. These schemes aren't just about handing out cash; they're strategic tools designed to kickstart housing delivery, unlock stubborn sites, and give a leg-up to developers who find it tough to get 100% of their funding from the private market.

Knowing how to weave this kind of support into your capital stack is a crucial skill. It can seriously de-risk a project, smooth out your cash flow, and ultimately make a scheme viable that might have otherwise been stuck on the drawing board. Before you even think about shaking hands on a deal, modelling these scenarios is non-negotiable. The DealSheet AI app can help you stress-test various funding structures, including government-backed loans, to get your financial projections watertight—download it today and start your free trial.

The Role of Homes England

In England, the main player you need to know is Homes England, the government's housing and regeneration agency. Its core mission is to step into the market where needed, making sure more homes get built in high-demand areas and breaking the reliance on a handful of major housebuilders.

Homes England runs several funding programmes, but the Home Building Fund is the big one for most developers. It's important to be clear: this isn't a grant. It's a commercial loan fund, but one designed to be more flexible and supportive than you might find elsewhere.

Here's a look at the official Homes England portal, which should be the first stop for any developer hunting for information on available funding.

This portal is your direct line to their funding programmes, latest news, and strategic plans. It's an essential bookmark for any serious UK developer.

How Government Finance Works on the Ground

Think of government finance as a partner to private lending, not a replacement for it. A common scenario sees a developer securing a senior debt facility from a bank to cover, say, 60% of the project costs. They might then approach Homes England for a mezzanine-style loan to plug a further gap in the funding. This can dramatically cut the amount of equity the developer has to find themselves.

Key features you'll often find include:

- Flexible Terms: Repayment schedules can sometimes be structured more creatively than those from traditional commercial lenders.

- Patient Capital: The government's priority is getting houses built, not necessarily chasing a rapid return, so they can often take a longer-term view.

- A Stamp of Approval: Securing government backing sends a powerful signal to private lenders, giving them more confidence to get involved in your project.

Crucial Insight: Getting these funds isn't just about having a viable project; it has to align with government priorities. You'll often need to demonstrate 'additionality'—proving your scheme simply wouldn't get off the ground without their support. This could also mean contributing to specific policy goals, like building on brownfield land or embracing modern methods of construction.

The impact of these programmes is huge. For SME developers, government-backed finance remains a vital option alongside commercial loans. To give you a sense of scale, statistics for 2025 show that Homes England's programmes supported 15,581 housing starts and 13,500 completions in just a six-month period. For developers focused on sub-250-unit schemes, combining senior debt with Homes England support can be the difference-maker, materially reducing equity requirements and de-risking the entire venture. You can explore the full housing statistics from the UK government to see the scale for yourself. Properly factoring these specific loan tranches into your appraisal tool is essential for an accurate forecast of your final return.

Choosing the Right Finance for Your Development

Now that we've unpacked the main property development finance options, we get to the sharp end of the process: picking the right one for your deal. This isn't about finding a single 'best' product; it's about matching the funding structure to your experience, the project's scale, your appetite for risk, and how much speed and flexibility you truly need.

Think of it this way. A first-time developer tackling a clean, four-unit new build would be wise to stick with a simple senior debt facility. It offers the cheapest capital and a straightforward relationship with one lender. The lower leverage, maybe 60% LTC, means putting more of your own skin in the game, but it keeps things simple and makes finance costs predictable—exactly what you need when you're building a track record.

On the other hand, a seasoned developer managing a complex, multi-phase scheme with a hefty Gross Development Value (GDV) might find a bespoke Joint Venture (JV) a much better fit. By bringing in an equity partner, they can fund 100% of the project costs, letting them punch well above their weight and take on deals their own capital could never touch.

Matching the Finance to the Developer

Let's be honest: your experience level is probably the first thing any lender will look at. If you're new to the game, you represent a higher perceived risk, which naturally pushes you towards simpler, lower-geared funding. Lenders will expect to see a meticulously planned project with rock-solid costings and a healthy contingency baked in.

Once you've got a few successful projects under your belt, the world opens up. A proven track record is the best risk mitigator there is, and lenders will start offering you more sophisticated and higher-leverage products. Suddenly, stretched senior debt, mezzanine finance, and genuinely attractive JV partnerships are on the table.

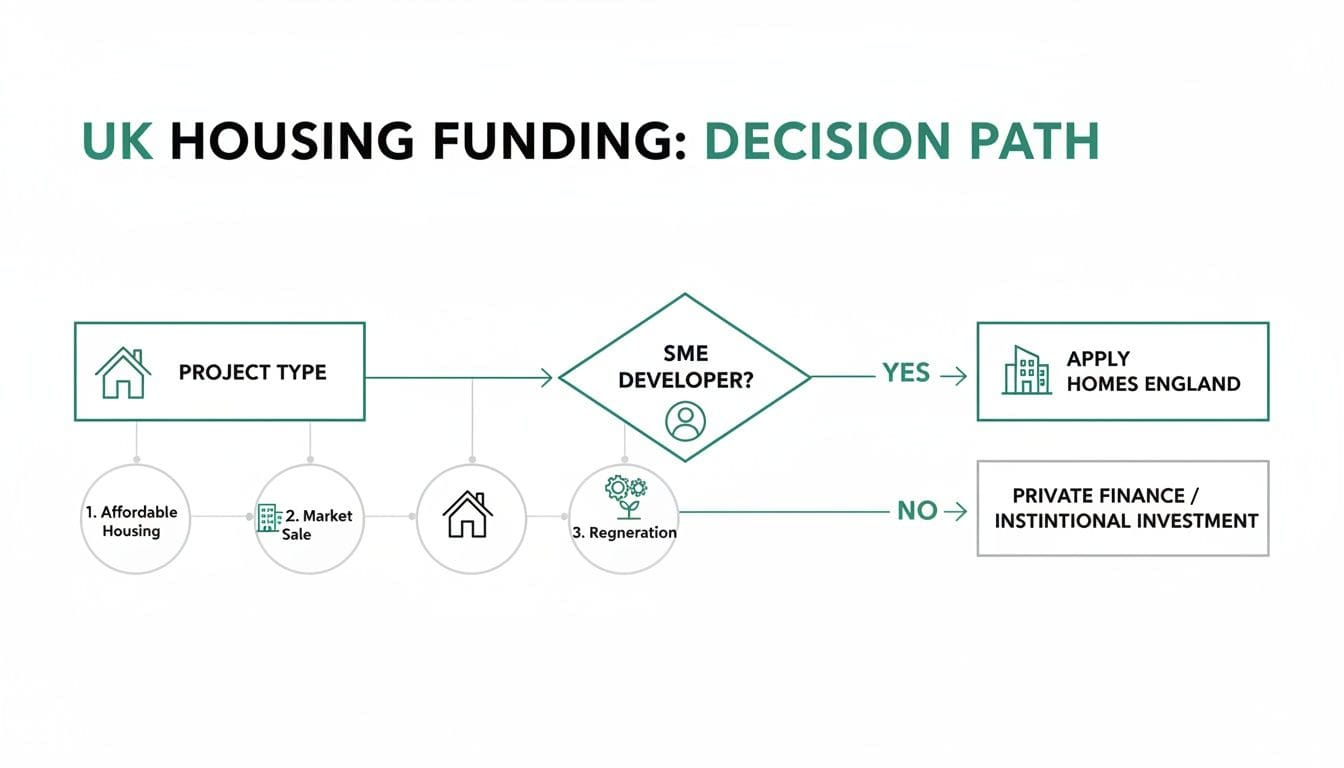

This flowchart gives you a simple decision-making map for figuring out which funding routes make the most sense for UK housing developers.

As you can see, project type and your scale as a developer are the primary filters. It also highlights how SME developers can often supplement private finance with government-backed schemes from funders like Homes England to get deals over the line.

Presenting a Professional Proposal

No matter which funding route you take, your success hangs on the quality of your proposal. A professional, well-underwritten submission that shows you've stress-tested the deal from every angle is non-negotiable.

Key Insight: Lenders aren't just funding a project; they are backing a developer. Your financial model is your primary tool for building that credibility. It must be robust, transparent, and account for everything from interest rate hikes to build cost inflation.

Your proposal has to clearly spell out the project's viability, backed by solid data on comparable sales, realistic build timelines, and a detailed cost breakdown. To really nail this, check out our guide on estimating building costs per square metre for the essential data your financial models need. A strong proposal anticipates the lender's questions and proves you're a capable operator, massively improving your odds of securing the best possible terms.

Common Questions Answered

When you're wading through the different property development finance options in the UK, a lot of questions come up. The market's complex, so let's clear up some of the most common queries.

How Much Equity Do I Need for a Development Project?

The amount of your own cash you need to put in—what lenders call 'skin in the game'—really depends on the finance structure you choose.

If you go for a straightforward senior debt loan, most lenders will only fund up to 60-65% of the total project costs. That means you're on the hook for the remaining 35-40% yourself.

But you can get clever. By layering mezzanine finance on top or using a stretched senior loan, it's possible to push the total borrowing up to 75-85% of costs. This move dramatically cuts your personal equity down to as little as 15%. And if you bring in a Joint Venture (JV) equity partner, you could even fund a deal with almost none of your own capital, though you'll be sharing a hefty slice of the profits.

Key Insight: Your required equity is a direct trade-off. A lower personal contribution almost always means paying higher interest rates or giving away a share of your profit. There's no free lunch.

Can I Get Development Finance with No Experience?

Securing funding as a first-time developer is tough, but it's definitely not a non-starter. Lenders will see you as a higher risk, so expect them to put your proposal under a microscope. You can't afford to present anything less than a professional, meticulously detailed plan.

To boost your chances, think strategically:

- Start Small: Forget the 20-unit scheme for now. Propose something simple and low-risk, like a single new-build or a straightforward conversion project.

- Build a Strong Team: Lenders aren't just backing you; they're backing your team. Surround yourself with experienced professionals, including a reputable main contractor, architect, and project manager. Their track record becomes part of your credibility.

- Opt for Lower Gearing: Go for a simple senior debt facility with a lower Loan-to-Cost ratio. This shows the lender you aren't overstretching and are willing to commit more of your own capital, which is a massive confidence booster.

What Is the Difference Between LTC and LTGDV?

Getting your head around these two acronyms is absolutely fundamental to comparing any of the property development finance options out there.

-

LTC (Loan to Cost): This is the loan amount measured as a percentage of the total project costs—that's the land purchase plus all your build costs. Lenders use LTC to decide how much they'll lend you to actually get the project built.

-

LTGDV (Loan to Gross Development Value): This metric looks at the loan amount as a percentage of the project's estimated final value once it's finished and ready to sell. Lenders use LTGDV as a crucial safety check to make sure there's a healthy profit margin in the deal and that the total debt makes sense against the asset's end value. Most lenders will cap their total facility at 70-75% LTGDV.

Ready to analyse your next deal with confidence? The DealSheet AI app helps you model various finance structures, calculate costs, and instantly see your projected returns. Download DealSheet AI from the App Store and start your free trial today.