What Is a Good Rental Yield for UK Property Investors in 2026?

What Is a Good Rental Yield for UK Property Investors in 2026?

So, what is good rental yield in the UK? Answering this is the first step for any property investor, and the short answer is that a gross yield of 5-7% is a solid benchmark for a standard buy-to-let in 2026. However, for more intensive strategies like an HMO, you should be aiming for 8-12% or higher. To analyse deals and calculate these yields instantly, savvy UK investors use the DealSheet AI app to validate opportunities on the go. This guide will delve deeper, exploring how location, strategy, and hidden costs affect what a 'good' yield really means for your investment.

Defining a Good Rental Yield for UK Investors

Rental yield is the absolute backbone of property investment analysis. It's a simple but incredibly powerful percentage that measures your annual rental income against the property's value. A higher yield generally signals a more profitable investment from a pure income perspective.

But what figure should you actually be targeting in the 2026 UK market?

The answer isn't a magic number, but a range that shifts based on your goals and, crucially, the property's postcode. A 4% yield might be perfectly acceptable in a prime London street where you're banking on significant capital growth, but it would be considered poor in a northern city where reliable cash flow is king.

National Benchmarks and Regional Differences

To really get to grips with what is good rental yield, you need to look at what the market is doing. The national average gives you a useful baseline, but the real opportunities are found when you drill down into specific cities and property types.

For instance, looking at data for 2026, the UK's national average gross rental yield is projected to stand at a respectable 6.98%. This figure, however, masks huge regional differences. Cities like Leeds are showing one-bedroom flats generating impressive yields of 7.77%, with two-beds hitting 7.81%—making it a hotspot for investors building a portfolio.

This is a world away from London, where sky-high property prices often drag average yields down to between 3.8% and 5.2%. Savvy investors know these regional variations are where the real profits are found. You can dig deeper into the numbers in the Global Property Guide's latest analysis.

A key takeaway for investors is to always aim for yields that beat the local average. If a city's typical buy-to-let yield is 6%, targeting properties that can hit 7-8% through a smart purchase or a light refurb gives you a competitive edge and a much-needed buffer against unexpected costs.

Aligning Yield with Your Investment Goals

Ultimately, your definition of a "good" yield must be tied to your financial objectives. Are you hunting for immediate monthly income, or are you playing the long game for capital growth?

-

For Cash Flow: If your priority is generating monthly profit to cover the mortgage and build a passive income, then a higher yield is non-negotiable. Investors targeting HMOs or serviced accommodation will be looking for gross yields well above 8%.

-

For Capital Growth: If you're investing for long-term appreciation, you might accept a lower yield (around 4-5%) in an area with a proven history of strong house price growth.

Knowing where to find these different types of opportunities is crucial. Check out our guide on the best investment property cities in the UK to see which locations are best suited to your strategy. We unpack everything you need to know to find properties that meet—and beat—these benchmarks.

Gross Yield vs Net Yield: The Difference Between Hype and Reality

When you start digging into property deals, you'll run into two terms immediately: gross yield and net yield. They sound alike, but the gap between them is the difference between a flashy marketing number and the actual cash that hits your bank account.

Getting this right is the first step to answering the all-important question: what is a good rental yield for your strategy?

Think of Gross Yield as the property's 'sticker price'. It's the simple, top-line figure estate agents love to quote because it's always higher and looks great on a brochure. It's a quick and dirty way to compare opportunities at a glance, but it's far from the full story.

The calculation is dead simple:

Gross Yield Formula: (Annual Rental Income / Purchase Price) x 100

Notice what's missing? Everything. This formula completely ignores the running costs of the property, giving you an optimistic—but dangerously incomplete—picture.

Gross Yield: A Manchester Example

Let's ground this in reality. Imagine you're eyeing up a two-bedroom flat in a popular part of Manchester.

- Purchase Price: £200,000

- Monthly Rent: £1,000

- Annual Rent: £1,000 x 12 = £12,000

Pop those numbers into the formula: (£12,000 / £200,000) x 100 = 6.0% Gross Yield.

On paper, 6.0% looks perfectly respectable. It sits comfortably in the typical 5-7% range for a standard buy-to-let. The problem is, this number doesn't account for a single pound in expenses. This is where Net Yield steps in and gives you a dose of reality.

Net Yield: The Number That Actually Matters

Net Yield is the metric that experienced investors live and die by. It's your real return, calculated by subtracting all the operational costs from your rental income before working out the percentage. It paints a much clearer picture of how an asset will actually perform.

The formula is a bit more involved, as it should be:

Net Yield Formula: ((Annual Rental Income - Annual Operating Costs) / Total Purchase Cost) x 100

Note the two crucial changes. We're now subtracting Annual Operating Costs, and the denominator is the Total Purchase Cost. This isn't just the price tag; it must include Stamp Duty Land Tax (SDLT), legal fees, and any day-one refurb costs. For a deeper dive, our complete guide explains how rental yield is calculated in more detail.

The 'Annual Operating Costs' bucket is where most new investors trip up. A proper analysis has to include:

- Mortgage Interest: Just the interest portion of your monthly payments.

- Insurance: Buildings and landlord insurance are non-negotiable.

- Letting Agent Fees: Typically 8-12% of the monthly rent for a fully managed service.

- Maintenance Budget: A vital buffer for repairs. A good rule of thumb is to set aside 10% of the annual rent.

- Service Charges & Ground Rent: Almost always a factor with leasehold flats.

- Void Periods: You have to budget for empty periods between tenancies. One month per year is a sensible starting point.

- Other Bits: Don't forget costs like gas safety certificates, EPC renewals, and potential landlord licensing fees.

Net Yield: The Same Manchester Example

Let's return to our £200,000 Manchester flat and apply these real-world costs.

- Annual Rent: £12,000

- Annual Operating Costs:

- Mortgage Interest (example): £4,500

- Letting Agent Fees (10%): £1,200

- Insurance: £300

- Maintenance (10% of rent): £1,200

- Service Charge: £1,000

- Void Period (1 month's rent): £1,000

- Total Annual Costs: £9,200

First, we find the net rental income: £12,000 (Rent) - £9,200 (Costs) = £2,800 Net Income.

Now, we can finally calculate the true Net Yield: (£2,800 / £200,000) x 100 = 1.4% Net Yield.

The table below starkly illustrates how the shiny Gross Yield gets whittled down by the reality of operational costs.

Gross Yield vs Net Yield A Typical UK Buy-to-Let Example

| Metric | Calculation/Amount (£) | Impact on Yield |

|---|---|---|

| Purchase Price | £200,000 | The denominator in our calculation. |

| Annual Rental Income | £12,000 | The starting point, leading to a 6.0% Gross Yield. |

| Annual Costs | -£9,200 | The reality check: includes mortgage interest, fees, voids, etc. |

| Net Annual Income | £2,800 | The actual profit before tax. |

| Final Net Yield | 1.4% | The realistic, decision-grade return on the property's value. |

The difference is night and day. The attractive 6.0% gross yield has plummeted to a much more sobering 1.4% net yield. This single example shows precisely why your investment decisions must always be based on the net figure.

Trying to track all these variables manually for every potential deal is a recipe for mistakes and missed opportunities. It's why tools like DealSheet AI are so powerful—they automate these complex sums, ensuring you never overlook a critical cost and can analyse deals with speed and confidence.

Matching Rental Yields to UK Property Strategies

The question "what is a good rental yield?" is a bit like asking "how long is a piece of string?". There's no single right answer, because the number that signals a fantastic deal for a standard buy-to-let (BTL) could be a massive red flag for a high-cash-flow HMO.

If you don't align your expectations with the right property strategy, you're setting yourself up for failure. Different approaches carry wildly different levels of risk, management headaches, and potential rewards. A standard BTL is a balanced, long-term game, whereas something like Serviced Accommodation demands constant attention but offers a much bigger prize.

Getting your head around these benchmarks is the first step to analysing any deal that lands on your desk.

Standard Buy-to-Let (BTL)

For most UK investors, the humble buy-to-let is their gateway into property. The aim here is simple: a reliable, long-term investment that provides a steady monthly income and, hopefully, grows in value over the years. It's a relatively passive strategy, especially if you hand the keys over to a letting agent.

A good gross rental yield for a standard BTL in 2026 is between 5% and 7%. This range typically leaves enough fat on the bone to cover your costs and generate a modest positive cash flow. If a deal is showing less than 5%, it needs to be in an area with seriously strong predictions for capital growth to make any sense.

Houses in Multiple Occupation (HMOs)

With an HMO, you're not just letting a property; you're renting it out room by room to a group of unrelated tenants. The entire strategy is geared towards one thing: squeezing the maximum possible cash flow from a single building.

But this extra income doesn't come for free. It brings with it much heavier management duties, tougher safety regulations, and often the need for a special license from your local council. To compensate for all that extra work and risk, investors should be targeting a much higher gross yield—think 8% to 12%, and sometimes even more. This premium is essential to cover the higher tenant churn and running costs like council tax and utilities, which the landlord usually pays.

Serviced Accommodation (SA) or Holiday Lets

Serviced Accommodation, or SA, is a completely different beast. You're essentially running a mini-hotel, letting your property out on a short-term basis to tourists, business travellers, or contractors. It has the potential to generate eye-watering returns, but it's also the most hands-on and volatile strategy, leaving you exposed to the whims of the tourism and hospitality markets.

For an SA deal to stack up, you should be aiming for gross yields of 10% to 15%+. This huge figure is necessary to absorb the punishing operating costs, which include constant cleaning, sky-high utility bills, booking platform fees (like Airbnb's cut), and the relentless admin of managing guest changeovers.

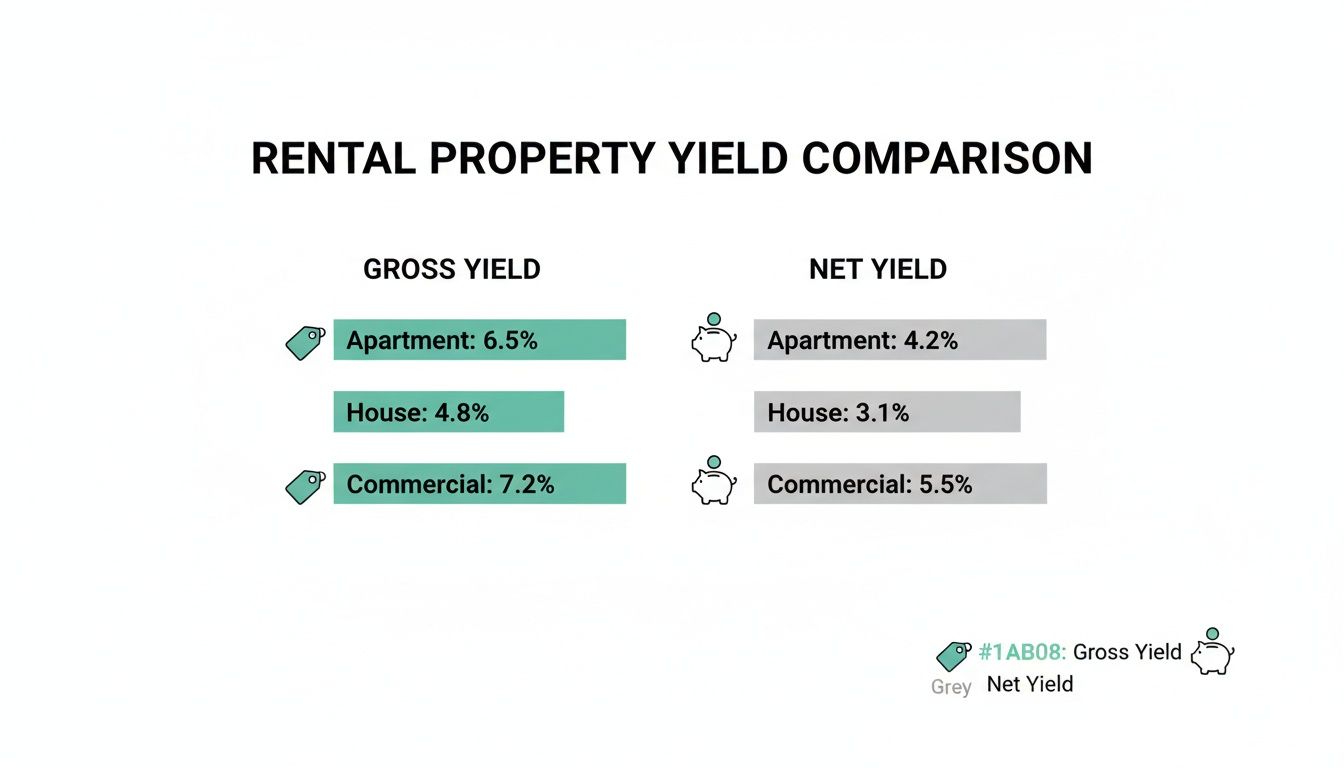

The chart below does a great job of showing the crucial difference between the headline 'gross' yield and the 'net' yield that actually matters.

Think of Gross Yield as the price tag you see on the shelf. It's a useful starting point. But Net Yield is what's left in your piggy bank after all the bills are paid—that's the number that reflects your actual profit.

The BRRRR Method

The BRRRR method (Buy, Refurbish, Refinance, Rent) is a powerful strategy focused on one goal: recycling your initial investment capital. The holy grail here is an 'infinite' Return on Investment, where you refinance the property at its new, higher value and pull out every penny of your original deposit.

While the spotlight is on ROI, the final 'Rent' stage is still absolutely critical. Once the dust has settled and the tenants are in, the property must perform as a solid rental. That means hitting the right yield benchmarks for its final form—whether that's a standard BTL (5-7%) or an HMO (8-12%+). A successful BRRRR project leaves you with a top-performing asset and your cash back in your pocket, ready for the next deal.

To get a better feel for the landscape, you can explore a range of different property investment strategies in the UK in our detailed guide.

Key Insight: Choosing the right strategy isn't just about chasing the biggest yield. It's about matching the return profile to your available time, capital, and stomach for risk. A high-yield HMO is worthless if you don't have the time to manage it properly.

Analysing these different strategies requires completely different financial models. The DealSheet AI app contains dedicated templates for BTL, HMO, SA, and BRRRR deals, with all the correct cost assumptions and tax rules already baked in. This means you can accurately compare a potential HMO against a standard BTL on a true like-for-like basis, ensuring your final decision is driven by solid, strategy-specific data.

How UK Taxes and Costs Demolish Your Real Yield

That shiny gross yield figure can give you a dangerous sense of false security. In the UK, the real profit you'll bank from a property isn't just about rent minus running costs. It's about what's left after navigating a tax landscape that can brutally erode your returns if you're not ready for it.

Getting a handle on these deductions is the only way to figure out what is a good rental yield in the real world. Your net yield calculation is pure fiction until you've factored in the taxman's slice. Legislation like Section 24 and upfront hits like Stamp Duty aren't minor details; they are deal-breakers that can flip a "profitable" investment into a loss-making headache. For any serious UK investor, mastering these rules is non-negotiable.

The Impact of Section 24 Mortgage Interest Relief

Section 24, often dubbed the 'tenant tax', is probably the single biggest tax change to hit UK landlords in a generation. It fundamentally rewired how buy-to-let profits are taxed for anyone investing in their personal name.

Before Section 24, life was simpler: you could deduct your full mortgage interest payments from your rental income before the taxman came knocking. Not anymore. Now, you get a basic rate tax credit of just 20% on your mortgage interest. This change is particularly punishing for higher-rate (40%) and additional-rate (45%) taxpayers.

Let's look at a stark 'before and after' to see the damage:

- Annual Rental Income: £15,000

- Annual Mortgage Interest: £7,000

- Landlord's Tax Rate: Higher Rate (40%)

Before Section 24: Your taxable profit was simple: £15,000 (rent) - £7,000 (interest) = £8,000. Your tax bill would be 40% of £8,000 = £3,200.

After Section 24: Things get painful. Your taxable profit is now the full £15,000 of rental income. The initial tax is 40% of £15,000 = £6,000. You then get a tax credit of 20% on your interest: 20% of £7,000 = £1,400. Your final tax bill is £6,000 - £1,400 = £4,600.

In this scenario, Section 24 has jacked up the landlord's annual tax bill by £1,400 — a staggering 43.75% increase. That cash comes directly out of your net yield and your monthly cash flow.

Upfront Costs: Stamp Duty Land Tax (SDLT)

Another huge cost that craters your total return is Stamp Duty Land Tax (SDLT). This is a hefty upfront tax on property purchases in England and Northern Ireland. The crucial bit for investors? Any purchase of an additional residential property gets slapped with a 3% surcharge on top of the standard SDLT rates.

This isn't a running cost you can smooth out over the year; it's a massive capital expense you have to find on day one. When calculating your Return on Investment (ROI), this must be added to your initial cash outlay. Forgetting to factor in SDLT will make your yield and ROI figures look dangerously optimistic. For a full breakdown, check out our guide on how Stamp Duty Land Tax is calculated in our guide.

Other Essential Costs to Factor In

Beyond those two big hitters, a whole host of other compliance and transactional costs will chip away at your real yield.

- Capital Gains Tax (CGT): When you eventually sell your investment property for a profit, that gain gets taxed. For residential property, higher-rate taxpayers are currently looking at a 24% bill on their gains.

- Landlord Licensing: More and more local councils are bringing in selective or mandatory licensing schemes, especially for HMOs. These fees can run from a few hundred quid to over a thousand pounds, and they are a recurring operational cost.

- EPC Compliance: To legally let a property, it needs a minimum Energy Performance Certificate (EPC) rating of 'E'. If a property you buy is languishing at an 'F' or 'G', you'll have to budget for improvement works, which are capped at £3,500.

If you don't account for these very real tax liabilities and compliance costs, your initial yield calculations are basically meaningless. It's only by baking in these UK-specific deductions that you get a true picture of what a good rental yield actually looks like for your portfolio.

Looking Beyond Yield to Cash Flow and ROI

While net yield is a fantastic tool for comparing properties, it doesn't tell the whole story. It's just one piece of the puzzle. To really get under the bonnet of a deal and see if it's worth your time and money, you need to look beyond that single percentage.

The real question isn't just "what is a good rental yield?" but "what does this deal actually do for me?". Answering that means bringing two other crucial metrics into the frame: cash flow and Return on Investment (ROI).

Think of it like this:

- Yield is the property's overall performance rating.

- Cash Flow is the actual money that hits your bank account each month.

- ROI measures how hard your personal cash is working for you.

Relying on yield alone is like driving with only one eye open. You might be heading in the right direction, but you're missing half the picture.

Your Monthly Salary: Understanding Cash Flow

Cash flow is the bread and butter of property investing. It's the metric that keeps the lights on. Put simply, it's the money left in your account each month after you've collected the rent and paid every single bill.

And I mean every bill. That includes the full mortgage payment (principal and interest), insurance, letting agent fees, a sensible budget for maintenance, and any other running costs. Positive cash flow means the property is funding itself and paying you a wage. Negative cash flow means you're paying to own it.

Cash Flow = Total Monthly Rental Income - Total Monthly Expenses (including full mortgage payment)

For most investors, a healthy target is £200-£300 of positive cash flow per month, per property. This gives you a buffer for surprise repairs and is the foundation of a real passive income stream.

Your Money's Efficiency: Return on Investment (ROI)

While yield measures a return against the property's total value, Return on Investment (ROI) gets personal. It measures the return you get on the actual cash you had to pull out of your own pocket to get the deal done.

This is the metric that matters most if you're using a mortgage. Your "cash in" includes everything you paid for upfront:

- Your deposit.

- Stamp Duty Land Tax (SDLT).

- Solicitor and legal fees.

- Any mortgage or broker fees.

- The budget for the initial lick of paint or refurbishment.

ROI then tells you how efficiently that lump sum of cash is working for you. Our detailed guide on what is a good ROI on rental property goes deeper into setting smart benchmarks.

Yield vs ROI vs Cash Flow: A UK Investor's Cheat Sheet

So, why does this all matter? Let's run the numbers on two UK properties to see why judging a deal on yield alone can be a costly mistake. Both appear identical at first glance.

| Metric | Property A (High Yield, Low Cash) | Property B (Lower Yield, High Cash) | Which Is Better? |

|---|---|---|---|

| Purchase Price | £125,000 | £250,000 | - |

| Annual Rent | £7,500 | £12,000 | - |

| Gross Yield | 6.0% | 4.8% | Property A looks better on yield. |

| Annual Costs (ex-mortgage) | £2,500 | £4,000 | - |

| Net Yield | 4.0% | 3.2% | Property A still looks better. |

| Mortgage (75% LTV, 5.5%) | £5,156 per year | £10,312 per year | - |

| Annual Cash Flow | -£156 (Negative!) | -£2,312 (Very Negative!) | Both are losing money every month. |

| Cash Invested (Deposit + Costs) | £35,000 | £65,000 | - |

| ROI (based on Cash Flow) | -0.4% | -3.6% | Both are terrible from an ROI perspective. |

At first, Property A's 6.0% gross yield looked far more attractive. But once we drill down, we see the reality: neither property puts a single pound in your pocket. In fact, both require you to subsidise them every single month.

This is why looking at all three metrics—yield, cash flow, and ROI—is non-negotiable. It's the only way to get a true 360-degree view and avoid deals that look good on paper but fail in the real world.

Common Questions About UK Rental Yield

Even when you've got the basics down, property always finds a way to throw a curveball. Getting your head around the nuances of yield, costs, and strategy is something we all keep refining, whether you're on your first deal or your fiftieth. Getting straight, practical answers is what builds the confidence to pull the trigger on a deal.

To nail down the key lessons from this guide, we've tackled some of the most common questions that come up about rental yield in the UK.

Is a High Rental Yield or High Capital Growth Better?

This is the classic investor tug-of-war, and the only honest answer is: it completely depends on what you want your money to do for you. There's no single "better" option, only the one that's better for your goals.

-

High Rental Yield (think 7% and up): This approach is all about generating strong, immediate cash flow. It's perfect for investors who want to build a passive income stream to cover their lifestyle costs, or for those looking to scale aggressively by recycling profits into the next deposit. Building an HMO portfolio in a northern city is a textbook yield-first strategy.

-

High Capital Growth: This is the long game. It's for investors who are less concerned with monthly income and more focused on building serious wealth as the property's value climbs over time. Prime postcodes in London and the South East often fit this mould, offering lower yields but a strong history of appreciation.

For most people, a balanced approach is the smartest play. A solid strategy is to set a minimum net yield you won't go below (say, 4-5%) to make sure the property washes its own face. Then, with that safety net in place, you can hunt for the best capital growth prospects that still hit your cash flow target.

How Can I Increase the Rental Yield on an Existing Property?

Squeezing more performance out of a property you already own is one of the most satisfying moves you can make. The good news is, you've got a few levers to pull.

First, the easiest win is a simple rent review. Are you actually charging the current market rate? A quick five-minute search on Rightmove for similar local properties will tell you. Even a modest £50 a month increase can make a real difference to your final yield figure.

Second, look at value-add improvements. A refreshed kitchen, a modernised bathroom, or even just smart cosmetic touches can justify a higher rent. It also tends to attract a better calibre of tenant, which means fewer voids.

Finally, get tough on your running costs. Could you get a better deal by remortgaging to a lower interest rate? When was the last time you shopped around for landlord insurance? Even renegotiating your letting agent's management fee from 12% down to 10% is a direct boost to your net yield that doesn't cost you a penny.

What Are Common Mistakes When Calculating Rental Yield?

The most common—and most expensive—mistake is taking the gross yield figure from an estate agent's brochure as gospel. That number is pure marketing. It completely ignores the real-world running costs that actually determine whether you make a profit or a loss.

Another huge error is being too optimistic with your cost forecasts, especially for maintenance and voids.

A prudent rule of thumb is to budget at least 10% of your annual rent for maintenance and assume the property will be empty for one month a year. If you don't, you're building a fragile financial model that will shatter the first time a boiler gives up the ghost.

Forgetting to include all your purchase costs is another classic pitfall. Things like Stamp Duty (SDLT), legal fees, and survey costs absolutely have to be included in your "total investment" figure when you're working out your true Return on Investment (ROI). If you leave them out, you'll be looking at a dangerously inflated number.

Which UK Regions Currently Have the Best Rental Yields?

For investors looking for strong returns in 2026, the best yields are consistently found where affordable property prices meet high tenant demand.

The North West (especially cities like Manchester and Liverpool), Yorkshire (Leeds and Sheffield), and parts of Scotland (like Glasgow) are still the standouts. These areas have strong local economies, big student populations, and ongoing regeneration, which all fuels the rental market. In these hotspots, hitting gross yields of 6-8% for a standard buy-to-let is realistic, and a well-run HMO can push past 10%.

On the flip side, London and the South East typically offer much lower yields, often in the 3-5% range. The trade-off is that they have a stronger track record for long-term capital growth. The key is to do your research on a street-by-street level, as yields can vary wildly even between neighbouring postcodes.

Stop second-guessing and start making data-driven decisions. The DealSheet AI app replaces fragile spreadsheets with instant, accurate, and repeatable deal analysis, built specifically for the UK market. Download DealSheet AI from the App Store and start your free trial today.