How to Invest in Properties UK: A Practical 2026 Guide

How to Invest in Properties UK: A Practical 2026 Guide

Learning how to invest in properties in the UK boils down to one core idea: buying assets that generate rental income, grow in value, or ideally, do both. The key to success is to understand the market, pick a strategy that fits your goals, and analyse deals with speed and accuracy. This guide provides the actionable blueprint for achieving that in 2026, showing you how to move from theory to building a profitable portfolio. To make confident decisions fast, you need the right tools; the DealSheet AI app is built for UK investors to let you crunch the numbers on any property deal in seconds.

Your Blueprint for UK Property Investment

Think of this guide as a practical blueprint for anyone serious about investing in UK property. We'll walk through everything from choosing your investment model to analysing deals and managing the inevitable risks. We'll break down the proven UK strategies like Buy-to-Let (BTL), Houses in Multiple Occupation (HMO), and the Buy, Refurbish, Refinance, Rent (BRRRR) model, helping you figure out which path makes the most sense for you.

You have to know which way the wind is blowing to succeed. As we move into 2026, the UK market is showing robust signs of stability. Rental demand remains fierce in many regional hotspots—the very places investors should be looking. Experts are forecasting a 3% national house price increase across 2026, but that could jump to between 4.5-5.5% in the high-demand areas where investors are most active. In these spots, you can often find solid deals in the £120,000 to £160,000 range, offering a realistic way in. You can get a deeper market analysis from brennanbespoke.co.uk's UK property market forecast.

Setting Your Investment Foundation

Before you even think about looking at properties, you need to be brutally honest about what you want to achieve. Are you after a monthly income that trickles into your bank account, or are you chasing a big, one-off payout from a sale? Your answer to that single question will shape every decision you make from here on out.

A few key questions you need to ask yourself:

- What's my war chest? This isn't just your deposit. It's the total cash you have for Stamp Duty Land Tax (SDLT), solicitors, and any other costs.

- How much time can I realistically commit? A hands-on strategy like a property flip demands a huge amount of your time. A standard BTL managed by an agent? Far less.

- What's my appetite for risk? High-yield strategies usually come with higher headaches. Think about managing multiple tenants in an HMO versus a single family in a terraced house.

A well-defined strategy is the difference between speculating and investing. Knowing your goals, capital, and risk tolerance from the start prevents costly errors and keeps your portfolio aligned with your long-term vision.

For those right at the beginning of their journey, our guide on investing in property for beginners offers some extra groundwork. Getting this preparation right means you can move with confidence when the right opportunities in 2026 pop up.

Choosing Your UK Property Investment Strategy

Your journey into UK property investment kicks off with one critical decision: picking the right strategy. This isn't just about buying a building; it's about matching an asset to your financial goals, the time you can realistically commit, and your appetite for risk. A hands-off investor chasing a steady, long-term income will take a completely different path from someone with trade skills looking for a quick, high-value profit.

Getting to grips with the core models is the first practical step. Each one comes with its own distinct advantages and demands, from the slow-and-steady Buy-to-Let to the intense but potentially lucrative property flip. When you find the right one, it'll feel like a natural fit for your circumstances.

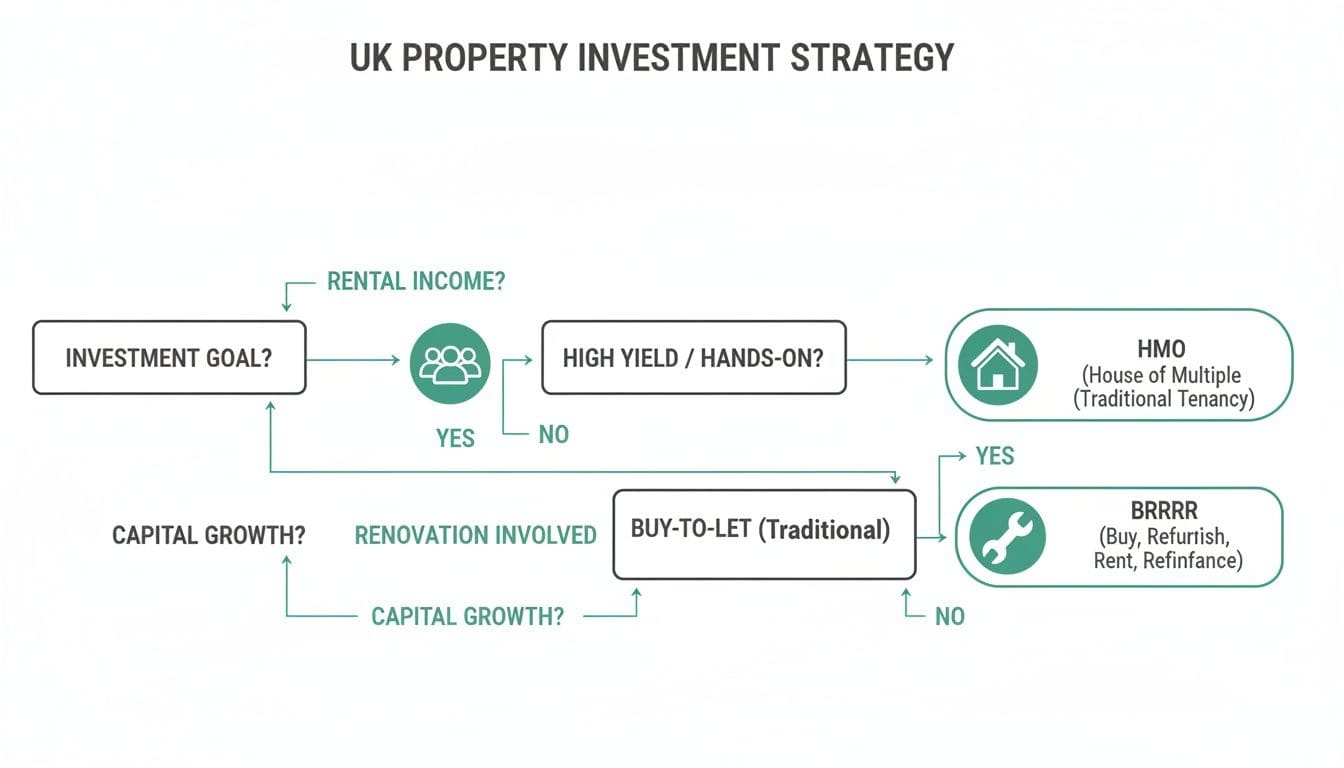

This flowchart can help you visualise which path might suit you best, depending on whether you're prioritising steady rental income, rapid capital growth, or a more hands-on approach.

As the diagram shows, your primary objective—whether that's cash flow, building equity, or capital gains—is the single most important factor. Each route demands a different level of your involvement and comes with its own unique risk profile.

The Classic Buy-to-Let (BTL) Model

The Buy-to-Let strategy is the bedrock of UK property investment. You simply buy a property and rent it out to a tenant, usually a single family or a professional couple, on an Assured Shorthold Tenancy (AST) agreement.

Its appeal is its relative simplicity and the potential for a double return: monthly rental income and long-term capital appreciation as the property's value hopefully grows over time.

This model is ideal for investors who prefer a more passive role, especially when you hire a letting agent to handle the day-to-day management. A typical BTL investor might buy a two-bedroom terrace house near a hospital in a regional city, ensuring consistent demand from key workers.

Houses in Multiple Occupation (HMOs) for High Cash Flow

An HMO involves renting out a property by the room to multiple, unrelated tenants. Think student housing or shared houses for young professionals. While the management is far more intensive and licensing from the local council is often required, the rewards can be substantial.

The combined rent from individual rooms typically generates a much higher gross yield than a standard BTL. For example, a five-bedroom house rented to students near a university could bring in £2,500 per month, whereas the same house rented to a single family might only achieve £1,400.

An HMO strategy effectively turns one property into multiple income streams. This diversification within a single asset can significantly boost monthly cash flow, but it comes with increased regulatory and management responsibilities.

The BRRRR Method: Building Equity and Recycling Capital

Buy, Refurbish, Refinance, Rent (BRRRR) is an active, value-add strategy. The process involves buying a property that needs work, renovating it to increase its value, refinancing onto a new mortgage based on the higher valuation, and then renting it out.

The ultimate goal is to pull out most, if not all, of your initial investment during the refinance. You can then use that cash for your next project. It's a powerful way to build a portfolio quickly without needing vast amounts of capital for each new purchase.

- Buy: Find a property below market value that has clear potential for improvement.

- Refurbish: Carry out renovations that add more value than they cost.

- Refinance: Secure a new mortgage based on the new, higher post-refurbishment value.

- Rent: Let the property out to generate rental income.

- Repeat: Use your pulled-out capital to start the next project.

Flipping Properties for Rapid Returns

Flipping, or Buy-to-Sell, is focused purely on capital gains. You buy a property, often at auction or one needing significant modernisation, renovate it quickly, and sell it on for a profit within a short timeframe, usually 6-12 months.

This strategy demands a deep understanding of local market values and renovation costs. Unlike rental strategies, there is no passive income; your entire return is realised upon sale. It's high-risk, high-reward, and best suited for those with project management skills and access to a reliable team of tradespeople.

To give you a clearer picture, this table compares the core strategies at a glance.

UK Property Investment Strategy Comparison

| Strategy | Primary Goal | Ideal For | Capital Growth vs. Cash Flow |

|---|---|---|---|

| Buy-to-Let (BTL) | Stable, long-term rental income and capital appreciation. | Hands-off investors seeking a balance of income and growth. | Balanced Focus |

| HMO | Maximising monthly rental income from a single asset. | Hands-on investors focused on achieving high cash flow. | Cash Flow Focus |

| BRRRR | Building a portfolio by recycling the same pot of capital. | Active investors who want to scale their holdings quickly. | Equity Building & Cash Flow |

| Property Flip | Generating a large, one-off profit in a short timeframe. | Experienced investors with renovation and market knowledge. | Capital Growth Focus |

Each path has its merits, but success depends on choosing the one that aligns with your resources and goals. For a more detailed breakdown of these approaches, you might be interested in our complete guide to UK property investment strategies. Choosing your path wisely is the most important decision you will make.

Sourcing and Analysing Deals Like a Professional

Right, you've picked your strategy. Now for the bit where the tyre meets the tarmac: finding and vetting actual investments. Knowing how to invest in properties is one thing, but this is where you learn to protect your capital by looking at deals with a cold, hard focus on the numbers. This is how you move from theory to practice, making sure a deal works on paper long before you commit a single pound.

This whole process is a mix of proactive searching and rapid-fire financial analysis. Your goal is to build a steady pipeline of potential deals and have a system that lets you chuck out the duds quickly. That way, you're only spending your time and money on genuine opportunities.

Proven Methods for Sourcing UK Property Deals

Great deals rarely just fall into your lap; they're the result of a systematic approach. Everyone starts on the big property portals, but the pros go deeper. They build networks and use specific tactics to find properties before they even hit the mass market.

Here are a few of the most effective ways to source deals in the UK:

- Mastering Online Portals: Don't just scroll. Use the advanced filters on sites like Rightmove and Zoopla. Hunt for properties that have been on the market for ages, have had price reductions, or are screaming "in need of modernisation." These are all tell-tale signs of a motivated seller.

- Building Agent Relationships: Don't just be another email address on a mailing list. Get down to the local estate agents in your target area, explain exactly what you're looking for, and prove you're a serious, ready-to-go buyer. A good relationship means you'll be the first person they call when a suitable property lands on their desk.

- Leveraging Property Auctions: Auctions can be a goldmine for below-market-value deals, from repossessions to probate sales. But they demand serious preparation. You have to get all your due diligence done before you bid, because when that hammer falls, you're in a legally binding contract.

The most successful investors don't wait for deals to come to them; they actively create opportunities. By combining digital tools with old-fashioned networking, you build a deal-finding engine that consistently uncovers potential investments.

Running the Numbers The Core of Deal Analysis

Finding a property is just the start. The analysis that follows is what separates a profitable asset from a financial sinkhole. Every single deal, no matter the strategy, has to be stress-tested against a few key financial metrics. This is where guesswork stops and data-driven decisions take over.

Your analysis should always calculate three non-negotiable figures:

- Gross Yield: This is the annual rent as a percentage of the purchase price. It's a quick, top-level indicator of a property's income potential, but it's just a starting point.

- Return on Investment (ROI): This is the one that really matters. It measures your annual profit (rent minus all costs) as a percentage of the actual cash you've put in (your deposit, fees, and refurb costs).

- Monthly Cash Flow: This is your profit after every single expense has been paid—mortgage, insurance, maintenance, voids, the lot. Positive cash flow is what makes an investment sustainable.

Our article on using a Rightmove deal analyser breaks down exactly how to pull these numbers from a simple property listing in minutes.

The Power of Fast, Automated Analysis

Trying to calculate these figures manually for every potential deal is a slow, painful process that's wide open to error. It gets even worse when you start trying to factor in UK-specific costs like Stamp Duty Land Tax (SDLT) or the brutal complexities of Section 24 for individual landlords. This is where technology becomes an essential part of learning how to invest in properties effectively.

The DealSheet AI app was built to get rid of this friction. It automates all these complex calculations, giving you a full, professional-grade analysis in seconds.

This speed is a massive advantage. While other investors are getting bogged down in spreadsheets, you can be analysing multiple deals, making informed offers faster, and snapping up opportunities before the competition even knows they exist.

The resilience of the UK market shows exactly why having a solid, numbers-first approach is so vital. In the 12 months to August 2025, total returns held firm at 8.7%, driven by strong rental income and a 2.7% growth in capital values across all sectors. This performance proves that even in a challenging climate, properly analysed deals deliver results.

Structuring Your Investment and Arranging Finance

How you decide to structure your property purchase is one of the most important decisions you'll make. It's a choice that has lasting consequences for your tax bill and your bottom line, so it's worth getting right from the very beginning.

Deciding whether to buy a property in your personal name or through a limited company is a fundamental fork in the road when you learn how to invest in properties in the UK. Nailing this can genuinely save you thousands over the life of your investment.

This isn't just about who owns the bricks and mortar; it directly affects how much tax you pay and which costs you can write off. Once you've settled on the best structure for your circumstances, you can then figure out how to finance the deal.

Individual Ownership vs A Limited Company

For years, the default option for most landlords was simply to buy property in their own name. But a major tax shake-up, known as Section 24, has completely changed the game, making the limited company route a far more attractive path for many UK investors.

If you own a property as an individual, Section 24 stops you from deducting your mortgage interest costs from your rental income before you calculate your tax. Instead, you only get a basic-rate tax credit of 20% on the interest. This is a huge problem for higher and additional-rate taxpayers, as it means they end up paying tax on their turnover, not their actual profit.

On the other hand, properties held inside a limited company (usually a Special Purpose Vehicle, or SPV) are completely unaffected by Section 24. The company can deduct 100% of the mortgage interest as a legitimate business expense. The remaining profit is then hit with Corporation Tax, which is often much lower than personal income tax rates.

The introduction of Section 24 was a game-changer. For anyone paying tax at 40% or 45%, operating through a limited company is now often the most tax-efficient way to build a rental portfolio, allowing for greater profit retention and reinvestment.

Let's put the two structures side-by-side to make it clear:

| Feature | Buying as an Individual | Buying via a Limited Company (SPV) |

|---|---|---|

| Mortgage Interest Relief | Restricted to a 20% tax credit (Section 24) | 100% of interest is a deductible expense |

| Taxation | Income Tax on profits (20%, 40%, 45%) | Corporation Tax on profits (currently 19-25%) |

| Mortgage Products | Wider range of products generally available | More specialist lenders; rates can be higher |

| Complexity & Costs | Simpler, with no annual company filings | Requires annual accounts and confirmation statements |

| Profit Extraction | Profits are personal income | Profits extracted via salary or dividends |

Ultimately, there's no single right answer. It all comes down to your personal tax position and your long-term ambitions. If you're a basic-rate taxpayer with just one or two properties, personal ownership might be simpler. But for anyone looking to scale a portfolio or who pays a higher rate of tax, the benefits of a limited company are pretty hard to ignore.

Arranging Your Property Finance

Once you've decided on your structure, the next job is to line up the money. Getting finance for an investment property is a different world to getting a mortgage on your own home. Lenders are far more interested in the property's rental income potential than they are in your personal salary.

The key concept you need to get your head around is leverage. This simply means using borrowed money—a mortgage—to amplify your potential return. For a standard buy-to-let mortgage, you'll usually need to put down a deposit of at least 25% of the property's value. The lender provides the other 75%, a ratio known as the Loan to Value (LTV). You can learn more about this crucial metric in our guide explaining what is the loan to value ratio.

Lenders will always run a "stress test" on the deal. They need to be confident that the rent will easily cover the mortgage payments, even if interest rates were to climb. As a rule of thumb, they'll want to see the monthly rent covering at least 125-145% of the mortgage payment.

If you're tackling something more complex, like an HMO conversion or a commercial development, you'll be looking at commercial finance. These loans are much more bespoke and are assessed case by case, looking at the project's viability and your track record as an investor. This is where a good mortgage broker really earns their fee.

Navigating Due Diligence and the UK Legal Process

Getting your offer accepted feels like the finish line, but it's really just the start of the race. This is where the real work begins: the due diligence phase. It's a period of intense scrutiny that'll tell you whether you've found a gem or a money pit waiting to drain your bank account.

Properly navigating the UK legal process is a non-negotiable skill. It's what protects your capital from nasty, expensive surprises that could have been spotted early on. This stage is all about verifying every last detail and uncovering potential problems before you're legally on the hook for the purchase. It's a joint effort between your solicitor, handling the legal minefield, and a surveyor, who gets hands-on with the building itself.

Assembling Your Professional Team

Your first move, before anything else, is to get a solicitor and a surveyor instructed. Don't just Google and go with the cheapest quote. You need professionals who live and breathe investment property; they understand the specific risks you need to be looking for, which a standard residential conveyancer might miss.

Your solicitor is your legal guide through this process. They're responsible for running searches, dissecting the contract, and making absolutely sure the seller actually has the legal right to sell. A good one is proactive, keeps you in the loop, and flags potential legal red flags the moment they see them.

The Property Survey: Uncovering Physical Risks

While your solicitor is buried in legal paperwork, your surveyor will visit the property to give it a thorough inspection. The type of survey you need will depend on the building's age and condition, but for an investment, this is absolutely not the place to skimp. A detailed report can uncover issues that could save you thousands down the line.

A good surveyor will be all over key areas, including:

- Structural Integrity: Looking for tell-tale signs of subsidence, heave, or significant cracks in the walls.

- Damp and Timber Issues: Identifying rising damp, penetrating damp, or evidence of woodworm or rot.

- The Roof: Assessing the state of the roof covering, gutters, and chimney stacks.

- Services: A high-level check of the electrics, plumbing, and heating systems.

A property survey isn't just a report; it's a powerful negotiation tool. If significant issues are found, you can use the surveyor's cost estimates to go back to the seller and renegotiate the price or ask them to fix the problems before completion.

Critical Legal Checks and Searches

Your solicitor will then carry out a series of searches with the local authority and other agencies. These are designed to uncover crucial information that you'd never spot just by walking around the property. These searches are vital for understanding any restrictions or future plans that could torpedo your investment's value.

This process typically includes:

- Local Authority Searches: These dig up information on planning permissions, building control history, any nearby road schemes, and whether the property sits in a conservation area.

- Title Deed Verification: Your solicitor pulls the title register from HM Land Registry to confirm who the legal owner is and check for any restrictions or "covenants" that could limit how you use the property.

- Environmental Searches: This check flags risks like contaminated land or flooding, which could cripple the property's value and make it difficult to insure.

Understanding the difference between freehold and leasehold is also absolutely critical at this stage. With a freehold, you own the building and the land it sits on, plain and simple. With a leasehold, you only own the right to occupy the property for a set number of years, and you'll likely be paying ground rent and service charges to a freeholder. Short leases are a massive red flag for mortgage lenders and can be incredibly expensive to extend.

This whole due diligence phase is underpinned by wider economic confidence. Recent ONS data shows UK business investment in property-related assets rose by 1.5% in Q3 2025, which you can read about in the latest business investment trends at ONS.gov.uk. This momentum suggests a healthy appetite for the kind of value-add projects that diligent investors uncover. While you conduct these checks, don't forget the financial side, particularly tax. For more detail, check out our guide on what Stamp Duty Land Tax is and how it will apply to your purchase.

Managing Risks and Planning Your Exit Strategy

Any seasoned investor will tell you that knowing how to invest in properties is as much about protecting your capital as it is about chasing big returns. A resilient portfolio isn't built on optimism; it's built by staring potential risks in the face and having a plan. We're talking about the dreaded void period where no rent comes in, or the boiler that inevitably gives up the ghost on the coldest night of the year.

Effective risk management isn't some dark art. It's just a proactive mindset that prepares you for the realities of being a landlord. This means creating financial buffers and having clear plans for the challenges that will, sooner or later, come your way.

Mitigating Common Landlord Risks

Three core things tend to keep landlords awake at night: empty properties, surprise repair bills, and tenants who cause problems. The good news is, you can put simple, practical strategies in place to soften the blow of each one.

A few essential tactics include:

- Building a Contingency Fund: You should aim to have 3-6 months' worth of the property's total running costs stashed away in a separate account. That includes the mortgage payments. This fund is what turns a potential financial crisis into a manageable inconvenience.

- Securing Proper Landlord Insurance: Your standard home insurance policy is useless for a rental property. You need specialised landlord insurance, which can cover you for loss of rent, property damage, and legal liabilities.

- Implementing Watertight Tenant Vetting: A robust referencing process is your absolute first line of defence. Always run credit checks, verify their employment, and get proper references from previous landlords. This is how you minimise the risk of late payments and property neglect from the outset.

Planning for the worst-case scenario is what allows you to operate with confidence. A solid contingency fund and the right insurance policy are not expenses; they are essential investments in the long-term stability of your portfolio.

Defining Your Exit Strategy From Day One

Just as important as managing the day-to-day risks is having a crystal-clear plan for how you'll eventually exit the investment. Your exit strategy isn't something to figure out later; it should influence the type of property you buy, how you structure the purchase, and countless decisions you'll make along the way.

Knowing your exit from the start gives you a clear destination. It focuses your efforts and helps you measure success against a defined goal, rather than just drifting along.

Common UK Property Exit Strategies

Your exit will almost certainly fall into one of three main camps, each one aligned with a different investment goal. Deciding which path is right for you is a critical part of learning how to invest in properties successfully.

Here are the most common routes UK investors take:

- Sell for Capital Appreciation: This is the classic "flip" or long-term hold approach. The goal is to sell the property after a period, hopefully for a much higher price than you paid, and bank your profit as a lump sum.

- Refinance to Recycle Capital: This is the absolute cornerstone of the BRRRR method. After you've refurbished a property and forced its value up, you refinance to pull out your initial investment. You can then use that same pot of cash to fund your next deal, all while the first property continues to generate rental income.

- Hold for Long-Term Cash Flow: For many investors, the ultimate prize is a portfolio of properties generating a passive income stream to fund their retirement or achieve financial freedom. The "exit" here isn't a sale, but the point at which the rental income completely replaces their earned income.

Thinking about your exit forces you to begin with the end in mind. This proactive approach keeps you in the driver's seat, allowing you to adapt to market shifts without ever being forced into a corner.

Your Property Investment Questions Answered

Diving into the world of UK property can feel like staring at a mountain of questions. Before you put your hard-earned capital on the line, you need clear, straightforward answers.

Whether this is your first deal or you're a seasoned investor sharpening your strategy, let's cut through the noise. This section tackles the questions we hear most often, from how much cash you really need to the gritty details of tax. The goal is to give you the confidence to navigate your projects without the guesswork.

Frequently Asked Questions

We've compiled some of the most common queries from UK property investors into a quick-reference table. Getting these fundamentals right from the start prevents major headaches down the line.

| Question | Answer |

|---|---|

| How much money do I need to start investing in UK property? | For a typical buy-to-let mortgage, you'll need a deposit of at least 25% of the property's value. On top of that, you must have cash ready for legal fees, surveys, and the all-important Stamp Duty Land Tax. The exact starting pot varies hugely by property price and location. |

| Is buying through a limited company always better for tax? | Not always. While a limited company lets you offset 100% of your mortgage interest against rental income, it often comes with higher mortgage rates and accounting costs. It's usually most beneficial for higher-rate taxpayers and those planning to build a large portfolio. Always get professional tax advice tailored to you. |

| What is a good rental yield in the UK? | A solid gross rental yield in the UK is generally 5% or higher, but this is massively dependent on the region. In lower-cost areas in the North, yields can top 8%, while in London and the South East, they might be closer to 3-4%. The number that really matters, though, is ensuring your net cash flow is positive after every single expense is paid. |

These core concepts—initial capital, tax structure, and performance metrics—are the absolute bedrock of a sound investment strategy. They directly impact your long-term profitability and your ability to scale your portfolio. Each decision shapes the next, setting the course for your entire property journey.

Stop drowning in spreadsheets and start making faster, smarter investment decisions. Download the DealSheet AI app and get a complete analysis of any UK property deal in seconds. Start your free trial on the App Store today.