How to Work Out Yield on a Property: A UK Investor's Guide for 2026

How to Work Out Yield on a Property: A UK Investor's Guide for 2026

If you're looking to succeed in UK property investment, knowing how to work out yield on a property is the single most critical skill you can master. In short, yield is the annual rental income expressed as a percentage of the property's total cost, giving you a clear measure of its performance. This guide provides the formulas, UK-specific examples, and actionable insights you need to calculate it accurately. For investors who want to analyse deals instantly without manual spreadsheets, the DealSheet AI app can analyse any UK property and calculate these crucial figures in seconds.

Why Property Yield Is Your Most Important Metric

Learning how to work out the yield on a property is the one skill every serious UK investor must master. It's what separates a calculated investment from a speculative punt.

In a market buffeted by interest rate changes and dramatic media headlines, your yield calculation provides a clear, objective measure of a deal's performance. While other metrics matter, yield is the bedrock. It lets you compare completely different opportunities on a like-for-like basis, so you know which one is the better bet for your UK portfolio.

For investors who want to skip the spreadsheet headaches, the DealSheet AI app can analyse deals and calculate these crucial figures in seconds.

The Two Pillars of Yield Calculation

At its heart, yield is split into two key types. Each one gives you a different piece of the puzzle on your deal analysis journey.

- Gross Yield: Think of this as your first, quick filter. It's a back-of-the-envelope calculation that gives you a snapshot of a property's raw income potential, before you factor in any running costs.

- Net Yield: This is the number that really counts. It shows you the actual profit left over after all operating costs are paid, giving you a far more realistic picture of the investment's financial health.

By mastering both gross and net yield calculations, you move from simply buying property to strategically building a portfolio that performs. It's the difference between guessing and knowing your numbers.

Understanding Long-Term UK Trends

It's also crucial to put today's numbers into context. UK housing yields have seen some major shifts over the last couple of decades.

Research that tracked over 134,000 UK properties found that yields, which hovered around 5.2% between 2003-2006, had dropped to a low of just 2.8% by 2023. This was largely driven by property prices rising much faster than rents, fuelled by years of declining interest rates.

Knowing these long-term trends in UK housing markets helps you understand whether a deal offering a 6% yield in 2026 is genuinely strong or just average compared to historical norms.

This guide will give you the formulas and practical examples you need to nail both gross and net yield. We'll also dig into what makes a good return in today's market, helping you define what a good rental yield is for your strategy.

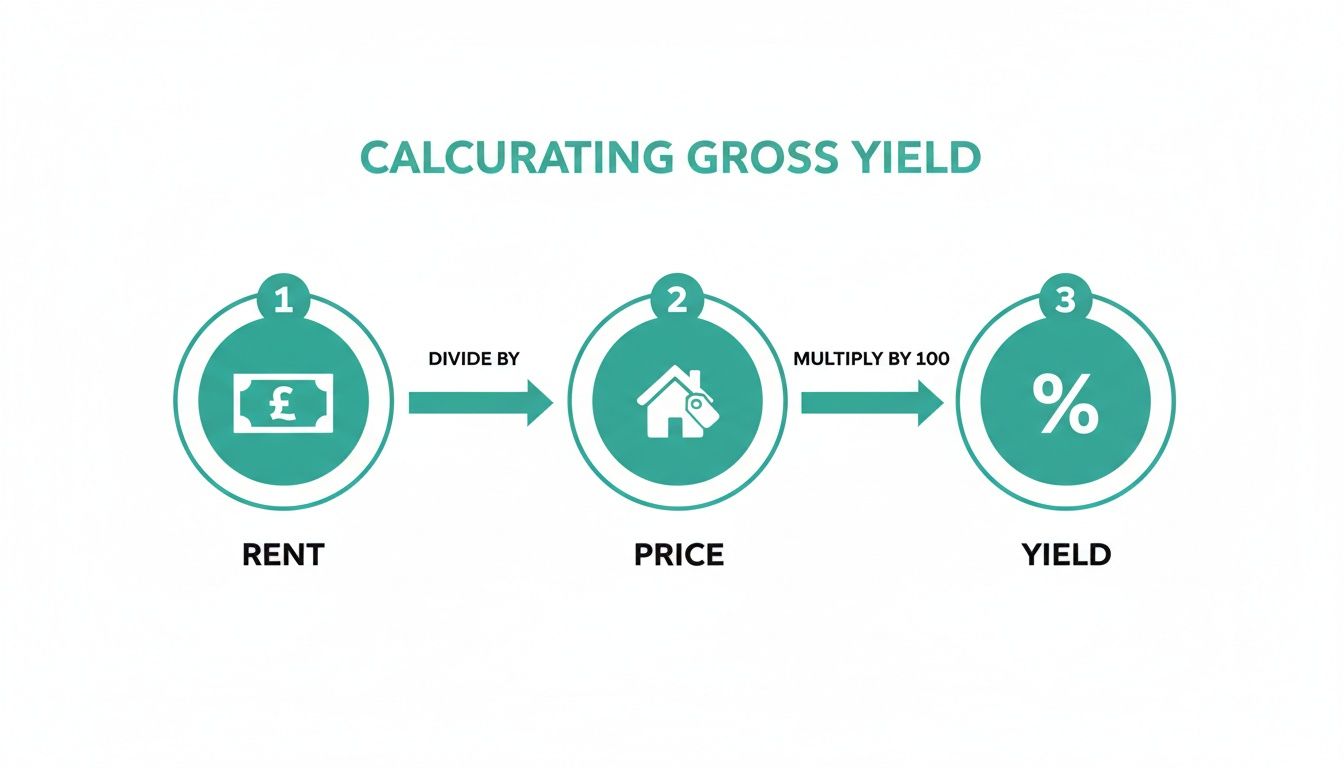

A Quick Guide to Calculating Gross Yield

Gross yield is your first-pass analysis. Think of it as a quick and dirty filter for sifting through potential deals, letting you see a property's income potential before you get bogged down in the nitty-gritty of running costs.

Knowing how to work out yield on a property this way means you can instantly discard deals that just don't have the top-line numbers to work. It's all about speed and initial comparison.

The formula itself is beautifully simple. It only cares about the income generated relative to what you paid for the asset, ignoring everything else for a moment of clarity.

Gross Yield Formula: (Annual Rental Income / Property Purchase Price) x 100 = Gross Yield %

By boiling a deal down to just these two numbers, you can quickly decide if it's even worth a deeper look.

Putting the Formula into Practice

Let's ground this with a real-world scenario. Say you're looking at a two-bedroom terrace in a city like Manchester.

- Property Purchase Price: The place is on the market for £225,000.

- Monthly Market Rent: After a quick check of similar properties on Rightmove and Zoopla, you reckon a realistic rent is £1,100 per month.

First thing's first, you need the annual rent. That's just your monthly figure multiplied by 12.

- Annual Rental Income: £1,100 x 12 = £13,200

Now you have the two inputs for the formula. Let's plug them in.

- Calculation: (£13,200 / £225,000) x 100 = 5.87%

So, the gross yield here is 5.87%. This single number is your benchmark. You can now compare it to other properties in Manchester or even stack it up against deals in different cities. If your personal strategy demands a minimum gross yield of 6%, you know this one falls just short and probably isn't worth your time.

To get a feel for this in a more summarised way, here's how the numbers fit together.

Gross Yield Calculation at a Glance

| Metric | Value | Calculation Step |

|---|---|---|

| Property Purchase Price | £225,000 | This is our denominator in the yield calculation. |

| Monthly Rental Income | £1,100 | The starting point for our income figure. |

| Annual Rental Income | £13,200 | Calculated as £1,100 x 12 months. |

| Gross Yield | 5.87% | (£13,200 / £225,000) x 100 |

This table makes it clear how the final percentage is derived from just two core inputs: price and rent. For a deeper dive, you can check out our guide on using a rent-to-value calculator to speed up these initial checks even further.

The Limits of Gross Yield

Now for the health warning. While gross yield is brilliant for quick filtering, it has to be handled with care. It's a blunt instrument that completely ignores the actual costs of owning and running a property.

It doesn't see your mortgage payments, insurance, maintenance bills, letting agent fees, or the financial hit from void periods.

Because of this, it can be seriously misleading. A property might flash a high gross yield, but if it comes with punishing service charges or needs constant repairs, your real profit could be wiped out. This is exactly why gross yield should only ever be your first step—a way to weed out the obvious non-starters before you invest your valuable time in a proper net yield analysis.

Finding Your True Profitability with Net Yield

While gross yield is a useful first filter, it's the net yield that tells you the real story. This is the number that matters—the actual profit left after all the running costs have taken their cut. If you want to know how to work out yield on a property like a professional, mastering the net yield calculation is non-negotiable.

The formula is a bit more involved, but it paints a far more accurate picture of your investment's health:

Net Yield Formula: ((Annual Rental Income - Annual Operating Costs) / Total Investment Cost) x 100 = Net Yield %

This calculation reveals what's truly left in your pocket. From experience, the two places investors almost always get tripped up are underestimating the 'Annual Operating Costs' and the 'Total Investment Cost'. Get these right, and your analysis will be rock solid.

As this shows, gross yield is a simple function of rent and price. Net yield, however, forces you to dig into the costs that are so often overlooked by novice investors.

Defining Your Annual Operating Costs

These are the recurring, year-on-year expenses that keep your rental property running. A comprehensive list is your best defence against nasty surprises that can completely wipe out your returns.

Your list of potential costs in the UK must include:

- Mortgage Interest: Just the interest portion of your monthly mortgage payment. It's crucial to remember that capital repayment isn't an operating cost.

- Letting Agent Fees: Expect to pay 8-15% of the monthly rent for a fully managed service.

- Insurance: Buildings insurance is a must, but so is landlord-specific contents and liability cover. Don't skip it.

- Maintenance & Repairs: A common rule of thumb is to budget 1% of the property's value each year. For older properties, you might want to increase this.

- Service Charges & Ground Rent: These are mandatory for leasehold properties and can vary wildly. Check the lease details carefully.

- Void Periods: Never assume 100% occupancy. Budget for at least a few weeks per year when the property might be empty between tenants.

- Safety Certificates: Annual gas safety checks (CP12) and Electrical Installation Condition Reports (EICR) every five years are legal requirements, not optional extras.

Calculating the Total Investment Cost

The other half of the puzzle is the total capital you've actually put into the deal. This figure goes way beyond just the purchase price—it includes all the one-off, upfront costs needed to acquire and prepare the property.

Key upfront costs to factor in:

- Purchase Price: The price you agreed with the seller.

- Stamp Duty Land Tax (SDLT): A huge expense, especially for second properties in the UK.

- Legal & Conveyancing Fees: The solicitor's costs for handling the legal transfer of ownership.

- Mortgage & Broker Fees: Any arrangement fees from your lender and the fee for your mortgage advisor.

- Initial Refurbishment: The budget required to get the property tenant-ready. Be realistic here; it's almost always more than you think.

The UK's current market dynamics make these calculations absolutely critical. Residential property affordability has hit levels not seen for nearly 150 years, with houses costing around nine times the average salary. This sky-high price-to-earnings ratio naturally squeezes gross yields right from the start.

As research shows, this price surge is largely down to a long-term decline in real interest rates. For investors in 2026, that means even small increases in mortgage rates can demolish your net yield, making meticulous expense tracking absolutely essential.

By accurately tallying these operating and upfront costs, your net yield calculation becomes a powerful indicator of true profitability, not just a rough guess. To explore a related metric that investors rely on, our guide on using a UK property ROI calculator provides some valuable extra insights.

Essential Metrics Beyond Rental Yield

While knowing how to work out yield on a property is a great starting point, relying on it alone is like trying to fly a plane with only one dial on the dashboard. A savvy investor knows you need a broader view to understand an asset's real financial health.

Building a resilient portfolio means looking beyond that single headline number. A property with a seemingly average yield might actually be a fantastic investment because of its strong cash flow or long-term growth potential. To see the full picture, you need to get comfortable with a few other critical numbers.

Return on Investment (ROI)

Return on Investment, or ROI, gives you the big-picture view of your investment's total performance. Unlike yield, which is purely about the rental income, ROI brings capital growth into the equation—the increase in the property's value over time.

It answers the crucial question: "What is my total return from both rent and appreciation?"

The formula is a powerful one:

ROI Formula: ((Net Profit + Equity Gain) / Total Investment Cost) x 100 = ROI %

Imagine you bought a property where your all-in cost was £250,000. Over one year, it generated a net profit of £5,000 from rent and also increased in value by £15,000. Your total return is £20,000.

Plug that in, and your ROI would be (£20,000 / £250,000) x 100, which equals 8%. This metric is vital for any investor targeting capital appreciation as part of their strategy.

Cash-on-Cash Return

This is arguably one of the most important metrics for anyone using a mortgage. Cash-on-Cash Return measures the return specifically on the actual cash you've put into the deal, not the property's total value. It shows you how hard your own money is working for you.

Here's the calculation:

- Cash-on-Cash Return Formula: (Annual Pre-Tax Cash Flow / Total Cash Invested) x 100 = CoC %

Let's say your total cash investment (your deposit, stamp duty, and fees) came to £60,000. After paying every single expense, including your mortgage, you are left with an annual pre-tax cash flow of £4,800.

Your cash-on-cash return is (£4,800 / £60,000) x 100 = 8%. For many investors, a high cash-on-cash return is the primary goal, as it shows how quickly their capital is generating more capital.

Monthly Cash Flow

Finally, we get to the simplest and most immediate measure of success: monthly cash flow. This is the money left in your bank account each month after you've collected the rent and paid every single bill associated with the property—including the full mortgage payment.

- Calculation: Total Monthly Rent - Total Monthly Expenses = Monthly Cash Flow

A positive cash flow means the property is funding itself and putting money in your pocket. A negative cash flow means you are propping it up from your own funds each month. It's the ultimate, real-world test of a property's short-term viability.

An investment that looks great on a spreadsheet but produces negative cash flow can quickly become a serious financial drain.

These metrics, when used together, tell the complete financial story of a deal. For more tools to help you run these numbers quickly, check out our guide on using a UK property investment calculator.

Avoiding Common and Costly Yield Calculation Mistakes

A tiny miscalculation in a spreadsheet can easily lead to a huge mistake on the ground. When you're learning how to work out yield on a property, it's the small details you overlook that tend to cost you the most. Think of this as your pre-flight checklist, designed to keep your investment analysis solid and protect your returns from some very common (and very avoidable) errors.

One of the most frequent traps is underestimating the true cost and timeline of a refurbishment. It's a classic. A renovation you've pencilled in at £5,000 can quickly spiral to £8,000, while a planned four-week project somehow stretches to eight. This double-whammy hammers your initial budget and, at the same time, extends the rent-free void period, pushing your income further down the road.

Actionable Tip: Always add a contingency of at least 15-20% to your refurbishment budget. For timelines, assume the project will take 50% longer than your first estimate. Stress-testing your numbers this way gives you a much more honest picture of your true entry costs.

Another costly oversight is forgetting to budget for void periods between tenancies. No property on earth is occupied 100% of the time. Even a fantastic rental will have gaps as tenants move on, and assuming a full 12 months of rent is a rookie error that will always inflate your yield calculation.

Verifying Valuations and Understanding Tax

Overly optimistic rental valuations are another major pitfall. A letting agent might suggest a high rental figure to win your business, but that's not the number you should be plugging into your analysis. You absolutely have to verify this with your own independent research.

- The Fix: Check actual achieved rents for comparable properties on platforms like Rightmove and Zoopla. Look specifically for listings marked "Let Agreed" to see what tenants are really paying in that postcode, rather than relying on aspirational asking prices.

Finally, getting your head around UK property tax is crucial. Misinterpreting Stamp Duty Land Tax (SDLT) rules, especially the 3% surcharge on second properties, can add thousands of pounds to your initial outlay. Forgetting it will wreck your yield figures before you've even started.

Perhaps the most fundamental error, though, is using national data for local analysis. As of November 2025, the average UK house price is £271,188. But using that figure to model a purchase in London or the North East would create a wildly inaccurate forecast. You can explore UK house price index data yourself to see just how much regional variations matter for any kind of accurate deal analysis.

Your Top Questions on Property Yield Answered

Even when you know the formulas, a few key questions always pop up when you're learning how to work out yield on a property. Getting these right is the difference between a confident purchase and a costly mistake. Let's tackle the most common queries we see from investors on the ground.

What Is a Good Rental Yield for a UK Property?

There's no single magic number here. A 'good' yield always comes down to your strategy and the property's location. But we can definitely talk about some solid benchmarks for 2026.

For a standard buy-to-let, most UK landlords are looking for a gross yield somewhere in the 5% to 8% range. In high-value, high-growth cities like London, you'll often see much lower yields, maybe 3-4%. Investors there are playing a different game, banking on strong capital growth over time to deliver their total return.

If you're looking at more intensive strategies like a House in Multiple Occupation (HMO), the targets shift. Here, investors often aim for a gross yield of 8% or higher. That premium is there to compensate for the extra management hassle, higher running costs, and the stricter regulations that come with HMOs.

The best way to judge a deal is to benchmark it against what's happening locally. Look at what similar properties have actually let for recently in the same area. That will tell you if your potential deal is a genuine standout or just average for the postcode.

How Does Section 24 Wreck My Net Yield?

Section 24 has a direct and often brutal impact on the real profitability for any UK landlord holding property in their personal name. In short, it stops you from deducting your mortgage interest as a business expense before you calculate your income tax.

Instead, you get a basic rate tax credit of 20% on your mortgage interest payments. If you're a higher-rate (40%) or additional-rate (45%) taxpayer, this means you're facing a much, much larger tax bill. This extra tax eats directly into your post-tax profit, shrinking your true net yield.

This is the single biggest reason you see so many investors now buying properties through a limited company. Properties owned within a corporate structure aren't affected by the Section 24 rules.

Should I Mix Capital Growth into My Yield Calculation?

No, you absolutely shouldn't. Keep these two calculations completely separate. Mixing them up just confuses your analysis and can easily make a poor-performing asset look better than it is.

- Rental Yield: This is all about the property's income performance today. It tells you everything you need to know about its cash flow potential.

- Capital Growth: This is about the property's potential to increase in value over the long haul.

Use rental yield to judge the income side of the investment. Separately, you should forecast the potential capital growth to understand your total Return on Investment (ROI) over the time you plan to hold it. Keeping them distinct gives you a much clearer picture of an investment's specific strengths and weaknesses. It's also worth remembering that upfront costs like Stamp Duty, which you can read about in our guide on what Stamp Duty Land Tax is, will affect your initial cash outlay and your total return calculations.

Stop second-guessing your numbers and start making confident investment decisions. With DealSheet AI, you can analyse any UK property deal in seconds, transforming a simple property listing into a comprehensive financial model.

Download the DealSheet AI app and start your free trial today.