A Landlord's Guide to Using a Rent Yield Calculator UK

A Landlord's Guide to Using a Rent Yield Calculator UK

For any serious UK property investor, understanding rental yield is the most critical metric for evaluating the true earning power of a property. This guide breaks down exactly how to use a rent yield calculator UK to find profitable deals in 2026, covering the crucial differences between gross and net yield and the hidden costs that can impact your returns. Getting this right is the difference between a profitable investment and a financial headache. To analyse any UK property deal from a simple URL in seconds, download the DealSheet AI app for a clear, data-driven picture of a deal's true potential. Get DealSheet AI on the App Store.

What Is a UK Rental Yield and Why Does It Matter?

Rental yield is your property's performance score. It strips away the emotional side of investing—the nice kitchen, the lovely garden—and boils everything down to a single, comparable number. This lets you objectively measure one opportunity against another, whether you're comparing a flat in Manchester to a terrace in Leeds.

But here's the catch: not all yields are created equal. The headline figure you often see quoted is the gross yield. It's a quick, back-of-the-envelope calculation based purely on rent and purchase price. While useful for a first glance, it dangerously ignores the real-world costs of being a landlord.

The True Measure of Profitability

The metric that actually matters to your bank account is the net yield. This is where the rubber meets the road. It gives you a far more realistic view by subtracting all the operational costs that eat into your income.

And those costs are extensive. You have to factor in everything:

- Mortgage interest payments

- Landlord insurance and service charges

- Letting agent and management fees

- Budgets for repairs and maintenance

- Void periods when the property is empty

- Taxes, including the painful impact of Section 24

Gross Yield vs Net Yield at a Glance

This table breaks down the crucial differences. Gross yield is for quick filtering; net yield is for making real decisions.

| Metric | What It Includes | What It Excludes | Best For |

|---|---|---|---|

| Gross Yield | Annual Rent, Purchase Price | All operating costs (mortgage, fees, voids, repairs, tax) | Quick, high-level comparison to filter out obvious non-starters. |

| Net Yield | Annual Rent, Purchase Price, All operating costs | Nothing—it's the full picture of profitability. | Serious deal analysis and making an actual investment decision. |

The gap between these two figures is often huge, and it's where many new landlords get tripped up. As of early 2026, the average gross rental yield in the UK is hovering around 5%. But once you start peeling back the layers of real-world costs like voids, repairs, and taxes, the average net yield often drops to a more sober 3.6%.

That's a massive difference. This rent-to-price ratio of 0.42% per month translates to just £420 in annual rent for every £100,000 invested. This is precisely why having an accurate calculator is non-negotiable, especially for more complex strategies like Serviced Accommodation or Flips where costs can spiral.

If you want to dig deeper into these crucial distinctions, our guide on what rent yield is and why it's critical is a great next step.

Calculating Gross vs Net Yield for Your Property

To get a real grip on a property's profitability, every UK investor needs to understand two critical numbers: gross yield and net yield. They sound similar, but they tell completely different stories about your return on investment.

Think of gross yield as the quick, back-of-the-envelope calculation. It's your first impression, perfect for rapidly comparing a handful of properties to see which ones even deserve a second look. But the figure that actually matters—the one that reflects the money hitting your bank account—is the net yield. This is your real-world return after every single cost has been stripped out. Getting this number right is what separates landlords who thrive from those who get blindsided by expenses.

The Simplicity of Gross Yield

Gross yield is all about speed and simplicity. It's a fast, initial benchmark that lets you filter out properties that are obviously overpriced for the rent they can command. It's the perfect first step in your analysis, nothing more.

The formula is dead simple:

Gross Yield = (Annual Rental Income / Property Purchase Price) x 100

This calculation completely ignores the realities of running a property—from mortgage payments to maintenance. It's purely a measure of income against the initial price tag. While it's a handy tool for shortlisting, relying on it alone is one of the most common and costly mistakes a new investor can make.

The Reality of Net Yield

This is where the serious analysis begins. Net yield is the figure that accounts for the financial reality of owning and managing a rental property in the UK. It's the number that reveals your true profit margin after all the bills are paid.

The formula is naturally more detailed, because it has to be:

Net Yield = ((Annual Rental Income - Annual Operating Costs) / Total Investment Cost) x 100

So, what are these crucial "operating costs"? It's a long list, and it's exactly what a basic rent yield calculator UK tool will miss if you don't feed it the right information.

- Mortgage Interest: This is the big one for most investors.

- Insurance: Buildings, contents, and specific landlord liability cover are non-negotiable.

- Void Periods: You have to budget for the inevitable gaps between tenancies.

- Repairs & Maintenance: From a leaky tap to a new boiler, things will break.

- Letting Agent Fees: If you use an agent, expect to pay 8-15% of the monthly rent.

- Service Charges & Ground Rent: Almost always a factor with leasehold flats.

- Compliance Costs: Gas safety certificates, EPCs, and electrical checks are legal must-haves.

Notice the "Total Investment Cost" in the formula, too. That's not just the purchase price. It includes Stamp Duty Land Tax (SDLT), solicitor fees, and any money you spend on an initial refurb to get it ready for tenants.

A Worked Example: Gross vs Net

Let's put this into practice with a realistic example. Imagine you're buying a property in the UK for £200,000, and it can generate £1,100 in monthly rent.

Gross Yield Calculation:

- Annual Rent: £1,100 x 12 = £13,200

- Gross Yield: (£13,200 / £200,000) x 100 = 6.6%

On paper, a 6.6% gross yield looks pretty solid. But now let's inject a dose of reality by factoring in the annual operating costs, which we'll conservatively estimate at £5,000 for the year (covering mortgage interest, insurance, voids, and repairs).

Net Yield Calculation:

- Net Annual Rent: £13,200 - £5,000 = £8,200

- Net Yield: (£8,200 / £200,000) x 100 = 4.1%

Just like that, the appealing 6.6% yield transforms into a much more sober 4.1%. This is why understanding net yield is non-negotiable. It's the difference between a deal that looks good and a deal that actually is good. For a deeper dive into these numbers, you can learn how to work out yield on a property in our dedicated guide.

Uncovering the Hidden Costs Every UK Landlord Forgets

A profitable property deal hinges on seeing every single expense, not just the obvious ones. While running costs like repairs and management fees are part of a standard net yield calculation, a few larger, often-forgotten financial hurdles can completely change your real returns. To use a rent yield calculator UK tool properly, you have to get these right.

Many investors get caught out by costs that go way beyond a leaky tap or an empty month. These are the big, complex expenses that can turn a promising deal into a financial nightmare if you ignore them. Let's break down the most critical ones every UK landlord needs to factor in.

The Upfront Hit of Stamp Duty Land Tax

Before you bank your first pound of rent, you'll face a massive one-off cost: Stamp Duty Land Tax (SDLT). For anyone buying an additional property in England and Northern Ireland, this tax comes with a hefty 3% surcharge on top of the standard rates.

This isn't just a minor admin fee; it can add thousands, or even tens of thousands, to your initial investment, hitting your overall return on investment (ROI) hard. On a £250,000 buy-to-let, for example, the SDLT bill is a painful £10,000. Forgetting to include this in your "Total Investment Cost" will give you a dangerously optimistic net yield figure from the start.

It's also crucial to remember this isn't the same everywhere:

- In Scotland, you'll pay the Land and Buildings Transaction Tax (LBTT), which has its own Additional Dwelling Supplement.

- In Wales, it's the Land Transaction Tax (LTT), with different rates and rules for second properties.

An accurate calculation means knowing the specific rates for the property's location. For a full breakdown, you can learn more about what Stamp Duty Land Tax is and how it works in our detailed guide.

The Game-Changer: Section 24

One of the most significant and misunderstood costs for UK landlords is the effect of Section 24 of the Finance Act 2015. This legislation completely changed how mortgage interest is treated for tax purposes, but only for individual landlords.

You used to be able to deduct your full mortgage interest payments from your rental income before calculating your tax bill. Not anymore. Now, you can only claim a basic rate tax credit of 20% on your interest payments.

This means higher-rate (40%) and additional-rate (45%) taxpayers can no longer claim full tax relief on their mortgage interest. The result is a much higher tax bill, which eats directly into your net profit and cash flow. For many, this has made previously profitable properties marginal or even loss-making.

Any serious rental yield analysis must account for the impact of Section 24. It can completely alter the viability of a leveraged buy-to-let investment, and ignoring it is one of the fastest ways to miscalculate a deal.

A Checklist of Other Essential Landlord Costs

Beyond SDLT and Section 24, a whole host of other expenses are non-negotiable for running a compliant and safe rental property. A reliable rent yield calculator UK should let you itemise these costs to build a true picture of your profitability.

Your checklist must include:

- Landlord Insurance: This is much more than standard home insurance. It needs to cover buildings, liability, and often loss of rent.

- Gas Safety Certificate (CP12): A legal requirement that must be renewed every year by a Gas Safe registered engineer.

- Energy Performance Certificate (EPC): Properties must hit a Minimum Energy Efficiency Standard (currently an 'E' rating) to be legally let, which could mean expensive upgrades.

- Electrical Installation Condition Report (EICR): Required every five years to ensure the property's wiring is safe.

- HMO Licensing: If your property is a House in Multiple Occupation, you'll likely need a licence from the local council, which comes with a significant fee and much stricter safety standards.

- Letting Agent Fees: Typically range from 8% to 15% of the monthly rent for finding a tenant or providing full management.

Projecting future cash flow is also critical, especially in a volatile market. UK rent inflation averaged 3.88% from 1989 to 2025, but it spiked to 9.0% in the 12 months to December 2024, showing just how quickly things can change. This volatility demands robust tools that can handle dynamic inputs, not just static spreadsheets. You can discover more insights about UK rent inflation on Trading Economics.

A Step-by-Step UK Buy-to-Let Calculation

Theory is great, but property investing is a practical game. To really get a feel for how a rent yield calculator UK works in the real world, let's roll up our sleeves and walk through a proper, step-by-step example for a typical buy-to-let.

Think of this as your repeatable framework. We're going to take a two-bedroom terrace house in Birmingham—a classic investor hotspot—and run the numbers from start to finish. You'll see exactly how a tempting gross yield can quickly change once you factor in the true costs of being a landlord.

Case Study: The Birmingham Terrace

First, let's lay out the basic numbers for our fictional deal. Getting these right is the foundation for everything that follows.

- Property Purchase Price: £225,000

- Monthly Rental Income: £1,150

- Initial Refurbishment Costs: £5,000

- Legal & Conveyancing Fees: £1,500

Before touching the yield formula, we need to calculate our total upfront investment. It's never just the purchase price; it's all the cash needed to get the keys and make the property tenant-ready.

The Stamp Duty Land Tax (SDLT) for a £225,000 buy-to-let in England (as a second property) comes to £8,750. Adding it all up, our total initial investment is £225,000 (price) + £5,000 (refurb) + £1,500 (fees) + £8,750 (SDLT) = £240,250.

Calculating the Gross Yield

With our key figures in hand, the gross yield calculation is quick and simple. It's a useful first glance, a top-level benchmark before we get bogged down in the details.

- Calculate Annual Rental Income: £1,150 (monthly rent) x 12 = £13,800

- Apply the Gross Yield Formula: (£13,800 / £225,000) x 100 = 6.13%

A gross yield of 6.13% looks pretty healthy on the surface. For an inexperienced investor, this number alone might be enough to jump on the deal. But as we know, this figure is an illusion because it completely ignores the running costs.

Calculating the Net Yield: The True Picture

Now for the reality check. We need to subtract all the annual operating costs that chip away at your rental income year after year.

Here's a realistic breakdown of those expenses:

- Letting Agent Fees (10% of rent): £1,380

- Landlord Insurance: £300

- Annual Gas Safety & EPC: £150

- Maintenance & Repairs Budget (1% of property value): £2,250

- Void Period (4 weeks' rent): £1,150

- Annual Mortgage Interest (example figure): £5,500

Total Annual Operating Costs: £1,380 + £300 + £150 + £2,250 + £1,150 + £5,500 = £10,730

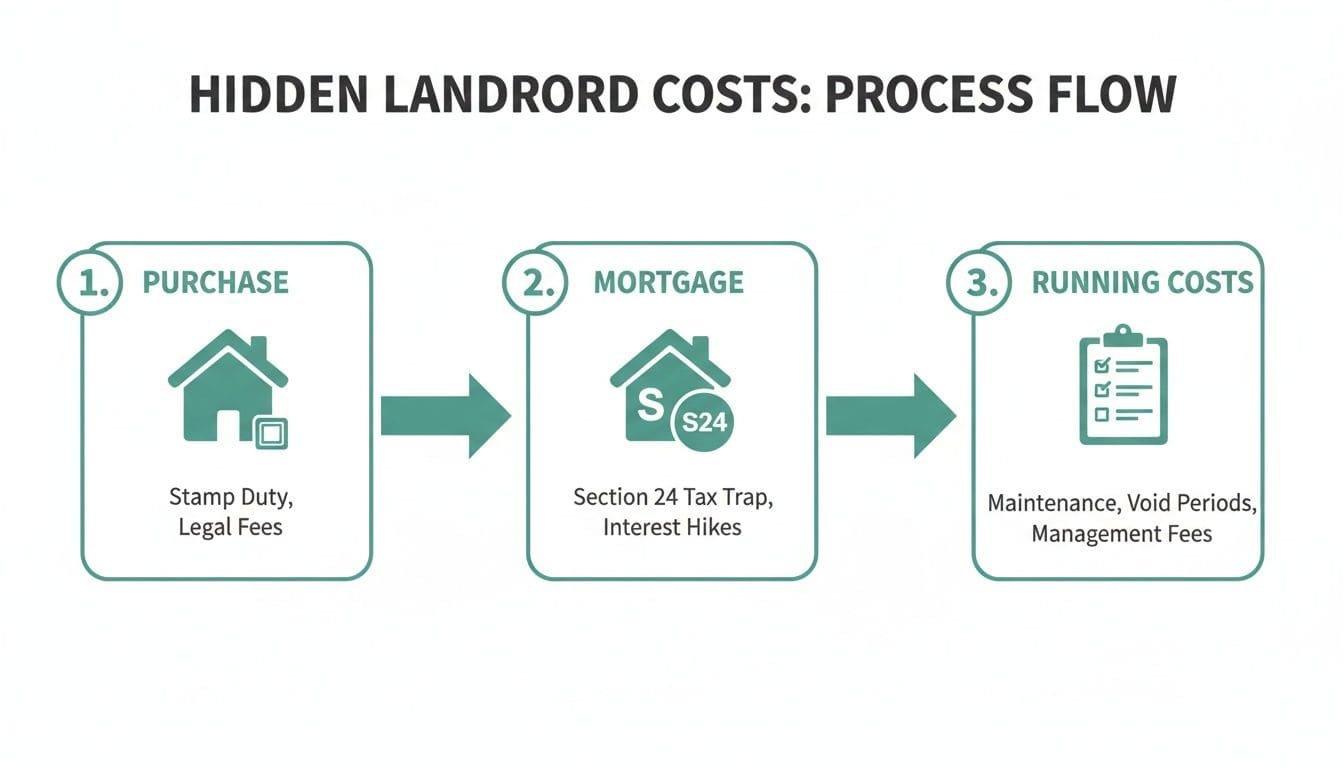

The infographic below shows how quickly these landlord costs can stack up, from purchase right through to the day-to-day running expenses.

This process flow maps out the journey from initial purchase costs, through mortgage realities like Section 24, to the ongoing expenses that ultimately define your net yield.

With our costs tallied, we can finally calculate the net income and the net yield—the number that truly matters.

- Calculate Net Annual Income: £13,800 (gross rent) - £10,730 (costs) = £3,070

- Apply the Net Yield Formula: (£3,070 / £240,250) x 100 = 1.28%

The final result is a net yield of 1.28%. This is a world away from the initial 6.13% gross yield and proves exactly why a thorough, detailed analysis is non-negotiable for any serious investor. This number shows the real return your invested cash is generating.

This walkthrough shows just how important it is to go beyond the headline figures. If you're looking for a tool that handles all this heavy lifting for you, our guide on choosing a buy-to-let investment calculator can point you in the right direction.

How to Find High-Yield Property Hotspots in the UK

Knowing how to calculate your rental yield is an essential skill, but it's only half the battle. The other half is knowing where to invest in the first place. Not all UK postcodes are created equal; finding the real high-yield hotspots takes a bit more strategy than just looking at national averages. After all, a powerful rent yield calculator UK tool is only as good as the numbers you feed it.

The UK property market is famous for its regional divides, and for investors, this is where the opportunity lies. For years, areas with lower property prices—think the North West, the North East, and Scotland—have consistently delivered much stronger rental yields than London and the South East. The logic is simple but powerful: property prices in these regions are more affordable, while rental demand remains solid, creating a much healthier rent-to-price ratio.

Decoding the North-South Yield Divide

This isn't just a hunch; the data backs it up time and time again. In the first quarter of 2024, for example, the North East proudly boasted the highest average gross rental yield in the UK at a whopping 7.65%. It's no surprise it's a prime target for savvy investors.

Now, compare that to London's average of just 4.93%. Despite sky-high rents, the equally sky-high property prices compress potential returns, making it much harder to generate positive cashflow. You can dig into more of this regional data and see the latest findings from Statista.

This fundamental relationship between property prices and local rental demand is the key to identifying profitable hotspots. Your goal as an investor is to find areas where property is still relatively affordable, but rental income is robust and, crucially, has room to grow.

To spot the postcodes that will perform well in 2026 and beyond, you need to look for specific growth indicators. These are the signs on the ground that an area's economy and rental market are heading in the right direction.

Key Indicators of a High-Yield Area

Don't just chase last year's hotspots. Instead, look for the underlying drivers that create rental demand and fuel future growth. Your research should focus on a few key signals that a location has genuine investment potential.

- Local Economic Investment: Are new businesses setting up shop? Is the local council ploughing money into new transport links or public spaces? Corporate investment creates jobs, and jobs are a powerful magnet for tenants.

- Regeneration Projects: Large-scale regeneration schemes can completely transform a neighbourhood, pushing up both property values and rental demand. Keep an eye out for areas with major planned developments.

- Strong Tenant Demographics: A high concentration of students or young professionals is a fantastic sign. These groups provide a consistent and reliable stream of rental demand. University towns, in particular, often deliver excellent yields for this very reason.

- Transport Links: Proximity to major transport hubs—train stations, motorways, and future tram or rail lines—is always a massive driver of demand. Good connectivity makes an area more desirable for commuters, widening your potential tenant pool significantly.

By focusing your search on postcodes that tick these boxes, you stop being a reactive investor and become a proactive one. You're not just finding areas that are high-yield right now; you're identifying places with the economic foundations to sustain and grow those yields for years to come. This approach allows you to look beyond the headlines and make smart, data-driven decisions based on genuine, long-term potential.

Moving Beyond Manual Spreadsheets for Property Analysis

Still calculating your rental yields on a manual spreadsheet? That's like navigating with a paper map in the age of GPS. It might get you there eventually, but it's slow, risky, and dangerously prone to human error. A single misplaced decimal or an outdated tax formula can completely warp your analysis, turning what looked like a great deal into a costly mistake.

The old way of doing things is just fraught with pitfalls. Simple data entry mistakes are common enough, but the real challenge is keeping up with the UK's constantly shifting regulatory landscape. Manually updating your spreadsheet for Stamp Duty Land Tax (SDLT) bands, Section 24 mortgage interest relief, and local licensing schemes is a full-time job in itself. It's not just inefficient; it's a massive risk to your capital.

The Smarter Approach to Deal Analysis

Fortunately, there's a much smarter way. Modern, automated tools are designed to eliminate these risks entirely, giving you the speed and accuracy needed in today's fast-moving property market. A proper rent yield calculator UK tool does the heavy lifting, letting you focus on strategy, not data entry.

Tools like the DealSheet AI app are built specifically for this. It replaces those cumbersome spreadsheets with an intelligent system that actually understands the nuances of UK property investment. You just paste in a property listing URL, and the app's AI instantly pulls the key data, applies the latest regulations, and runs a complete financial analysis in seconds.

The screenshot below shows a typical analysis summary, presenting the key metrics like ROI and cashflow in a way you can actually use.

This kind of dashboard immediately highlights the most important figures, letting you assess a deal's viability at a glance without getting lost in complex formulas.

Gaining a Competitive Edge

This isn't just about saving time; it's about gaining a crucial competitive advantage. While other investors are still fumbling with spreadsheets, you can analyse multiple deals with confidence, running sophisticated scenarios for strategies like HMOs, BRRRR, or Flips.

By automating the tedious calculation process, you free up your time to find more opportunities, negotiate better terms, and make smarter, data-driven decisions. In a competitive market, the investor who can analyse deals the fastest and most accurately almost always wins.

This shift from manual to automated analysis is essential for any serious UK property investor in 2026. It's about moving from guesswork to certainty and building your portfolio on a foundation of precise, reliable data. For those looking to manage more complex portfolios, our guide explains how to evaluate HMOs, Serviced Accommodation, and BRRRR deals without breaking your spreadsheet.

Common Questions About UK Rental Yield

Once you start digging into property numbers, a few questions always pop up. It's completely normal. To help you get your analysis right from the start, we've put together straight answers to the queries we hear most from UK landlords.

Think of this as your quick-reference guide. No jargon, just practical answers to build your confidence.

What Is a Good Rental Yield in the UK for 2026?

This is the big one, and the honest answer is always: "it depends on your strategy." There's no single magic number, but a gross yield between 5% and 8% is widely seen as a solid benchmark for a standard buy-to-let in many parts of the UK.

But a "good" yield is all about what you're trying to achieve.

- For high cash flow strategies, like HMOs or Serviced Accommodation, investors are often targeting a gross yield of 10% or more to make the extra management effort worthwhile.

- For capital growth investors in prime spots like London, a much lower net yield of 2-3% might be perfectly acceptable. The real prize for them is long-term appreciation, not monthly profit.

The most important thing? Always pivot your focus to the net yield. That's the figure that shows what you actually bank after every single cost has been paid.

How Often Should I Recalculate My Rental Yield?

You should run the numbers on your property's yield at least once a year, or anytime there's a major financial shift. An annual health check keeps you honest about how your investment is truly performing.

Key moments that demand a recalculation include:

- Rent Increases: As soon as you agree a new rent with your tenants.

- Remortgaging: A new mortgage deal is one of the biggest changes to your cost base.

- Major Repairs: A surprise £3,000 boiler replacement will hit your annual net profit, and you need to see the impact.

Staying on top of your numbers means you're working with a live, accurate picture of your investment's health, not a rosy calculation you made on day one.

Can a High Yield Also Be a Red Flag?

Absolutely. A yield that looks too good to be true often is. If you see an unusually high figure—say, over 12% for a standard buy-to-let—it should trigger your due diligence instincts, not just your excitement. A basic rent yield calculator UK tool can't spot underlying problems.

These deals often come with hidden red flags:

- A declining area: The property might be in a neighbourhood with growing social issues or economic decline, making it a nightmare to find good tenants or ever see capital growth.

- A problem property: The building might have deep-seated issues like damp, structural problems, or a short lease that requires a huge cash outlay down the line.

- A saturated rental market: Too many similar properties can lead to long, costly void periods and force you to drop your rent just to get a tenant in.

Always dig deeper on deals that look like outliers. A strong yield is fantastic, but not if it comes with a high risk of capital loss or operational headaches.

Ready to analyse your next property deal with speed, accuracy, and confidence? The DealSheet AI app takes the guesswork out of property investment, running a complete financial analysis in seconds. Download it today and start making smarter decisions. Get DealSheet AI on the App Store.