What is Rent Yield? A UK Investor's Guide for 2026

What is Rent Yield? A UK Investor's Guide for 2026

Put simply, rent yield is the annual return you make from a property's rent, expressed as a percentage of the property's value. Understanding what is rent yield is the first, most crucial step in analysing any UK buy-to-let investment, as it tells you how hard your money will be working for you.

Think of it as the ultimate performance scorecard for your investment. It cuts through the noise of house prices and lets you compare a flat in Manchester with a terrace in Bristol on a level playing field. It's the primary indicator of a property's cash-flow potential. To make this crucial calculation effortless, you need actionable insights, which is why tools like the DealSheet AI app give you instant, accurate yield analysis straight from a property listing.

Your First Step in UK Property Analysis

Understanding rent yield is absolutely vital for UK investors. The property market isn't one single entity; it's a patchwork of totally different regional markets where prices and rental demand can vary dramatically. A property's purchase price alone tells you very little about how it will actually perform as an asset.

Rental yield gives you a standardised benchmark to judge potential returns objectively. It helps answer the fundamental question every buy-to-let investor asks: "How hard is my money actually working for me?"

By focusing on this percentage, you can quickly sift through listings to find properties that line up with your financial goals, whether that's maximising monthly income or building a long-term portfolio. For anyone just starting out, getting your head around this concept is a cornerstone of investing in property for beginners.

Why Location Is Everything for Yield

This focus on percentages is critical because high property prices don't automatically mean high returns. In the UK, the opposite is often true.

Take 2026 for example. Projections based on current trends suggest the North East will likely continue to top the charts with an impressive average gross rental yield of around 7.5%. Meanwhile, London will probably trail far behind at closer to 5.0%, where eye-watering property prices—often over £500,000 for a one-bed flat—massively outpace the rents you can achieve.

This stark regional divide shows exactly why you need to know a property's rent yield. To give you a clearer picture, here's how yields looked across the UK in recent times.

Gross Rental Yield at a Glance Across the UK (Q1 2024)

| UK Region | Average Gross Yield |

|---|---|

| North East | 7.65% |

| Scotland | 7.40% |

| North West | 6.61% |

| Yorkshire and the Humber | 6.45% |

| Wales | 6.22% |

| West Midlands | 6.16% |

| East Midlands | 5.84% |

| South West | 5.45% |

| South East | 5.25% |

| London | 4.93% |

Source: Statista.com

As you can see, the difference between the highest and lowest-yielding regions is significant. This is precisely why investors look beyond the capital for better cash-flowing opportunities.

Rental yield is the financial compass for your property journey. It points you towards cash flow and helps you navigate away from assets that look good on paper but fail to perform in reality.

As we'll explore next, the headline "gross yield" is only the beginning of the story, but it's the perfect starting point for any serious deal analysis.

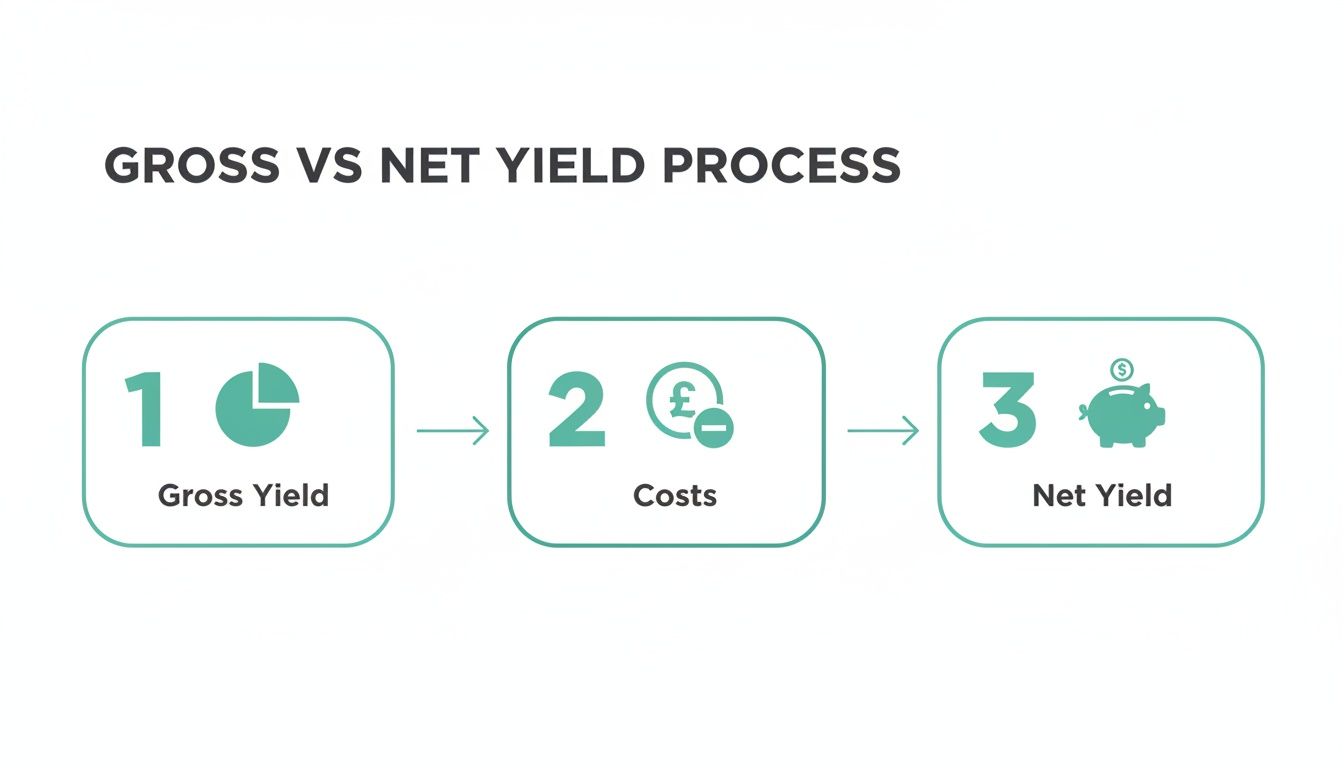

Gross Yield vs Net Yield: Seeing the Full Financial Picture

When you first look at a property deal, the metric that always jumps out is the gross rent yield. Think of it like a car's top speed in a brochure—it's an impressive headline figure designed to grab your attention. It's a quick, back-of-the-envelope calculation, perfect for a first-pass filter.

But just as a car's real-world performance is dictated by fuel, insurance, and maintenance, your property's true profitability is revealed by its net rent yield. This is the number that actually matters because it shows you what's left in your pocket after all the bills are paid. Getting your head around this difference is non-negotiable if you want to understand an investment's genuine financial health.

Understanding Gross Yield

Gross yield gives you a fast, high-level way to compare different properties. Its biggest feature is its simplicity; it completely ignores all the running costs that come with being a landlord.

The formula is dead simple:

(Total Annual Rent / Property Purchase Price) x 100 = Gross Yield %

So, a property you buy for £200,000 that rents for £1,000 a month (£12,000 per year) gives you a gross yield of 6%. It's a handy starting point, but it's a long way from the full story.

The Reality of Net Yield

Net yield is where the financial picture gets real. It tells you what you're actually earning from the investment by subtracting all the necessary operating costs from your rental income before doing the calculation. Your actual profit lives inside this metric.

The formula is naturally a bit more involved:

((Total Annual Rent - Total Annual Costs) / Property Purchase Price) x 100 = Net Yield %

So, what are these all-important costs? They can add up surprisingly fast and have to be factored in for any kind of accurate forecast.

- Mortgage Interest: For most investors, this is the single largest expense by a country mile.

- Letting Agent Fees: Typically between 8-15% of the monthly rent for management services.

- Landlord Insurance: Absolutely essential cover for the building, any contents you provide, and your liability.

- Maintenance and Repairs: A good rule of thumb is to budget around 1% of the property's value each year.

- Ground Rent & Service Charges: These are common with leasehold properties, especially flats.

- Void Periods: You have to budget for times the property might be empty. At least one month a year is a sensible starting point.

- Legal and Safety Certificates: Things like Gas Safety, Electrical Installation Condition Reports (EICRs), and Energy Performance Certificates (EPCs).

This list covers the big ones, but you can see a more detailed breakdown in our guide on using a buy-to-let yield calculator.

Here's a look at the DealSheet AI app, showing exactly how these costs are itemised to calculate the net yield for you, instantly.

The app clearly separates your income from all the operational costs, giving you an immediate and accurate net yield that reflects real-world profitability. Forgetting to account for these expenses is one of the most common mistakes in property investing and can easily turn what looks like a great deal into a financial headache.

How to Confidently Calculate Rental Yield

Theory is one thing, but running the numbers is what truly builds confidence in a property deal. To show you exactly how it works, let's walk through two practical examples following 'Alex', a UK property investor analysing a couple of potential purchases.

These real-world scenarios will demystify the maths behind calculating rent yield. More importantly, they'll highlight why a quick gross yield calculation is only ever a starting point, and how the net yield reveals the true financial story.

Example 1: The Standard Leeds Buy-to-Let

Alex finds a two-bedroom flat for sale in a popular Leeds suburb for £175,000. The letting agent confidently states it can achieve a monthly rent of £900. Alex's first step is to calculate the gross yield to see if it's even worth a closer look.

- Annual Rent: £900 x 12 = £10,800

- Gross Yield Calculation: (£10,800 / £175,000) x 100 = 6.17%

A gross yield over 6% looks promising for Leeds, so Alex digs deeper to find the net yield. He starts estimating his annual costs, including mortgage interest, insurance, and putting some cash aside for maintenance.

- Total Annual Costs: £4,800 (including mortgage interest, insurance, service charge, and a repair fund)

- Net Annual Income: £10,800 (Rent) - £4,800 (Costs) = £6,000

- Net Yield Calculation: (£6,000 / £175,000) x 100 = 3.43%

The net yield is significantly lower, but that's normal. This figure gives Alex a much more realistic picture of the actual cash flow he can expect. This process—starting with a simple calculation and then subtracting real-world costs—is absolutely fundamental to property analysis.

This flow from a high-level overview to a detailed financial picture is the core of understanding what rent yield really means for your bank account.

As you can see, net yield is simply what's left after the unavoidable costs of ownership are taken out of your gross rental income. It's the number that actually matters.

Example 2: The Complex Liverpool HMO

Next up, Alex considers a five-bedroom House in Multiple Occupation (HMO) near a university in Liverpool, priced at £250,000. With each room renting for £450 per month (including bills), the potential income is much higher.

- Annual Rent: (£450 x 5 rooms) x 12 = £27,000

- Gross Yield Calculation: (£27,000 / £250,000) x 100 = 10.8%

A gross yield above 10% is definitely attractive, but Alex knows that HMOs come with much higher operating costs. He needs to account for council tax, all utilities, enhanced insurance, and more intensive management.

With HMOs, higher gross income is a given, but so are higher expenses. The net yield calculation is not just important; it is absolutely critical to avoid turning a high-income property into a low-profit headache.

Alex gets to work listing out the increased annual costs:

- Utilities (Gas, Electric, Water, Broadband): £4,200

- Council Tax: £2,000

- Specialist HMO Insurance: £800

- Management Fees (12%): £3,240

- Maintenance & Voids (between academic years): £2,500

- Mortgage Interest: £7,500

- Total Annual Costs: £20,240

Now for the reality check.

- Net Annual Income: £27,000 - £20,240 = £6,760

- Net Yield Calculation: (£6,760 / £250,000) x 100 = 2.70%

Despite that massive gross yield, the net yield is actually lower than the Leeds flat. This example powerfully illustrates why you must account for every single cost. If you're comparing different types of property investments, you might find our guide on using a rent to value calculator helpful for quick initial filtering.

Manually calculating these figures is time-consuming and dangerously prone to error, which is why automating the analysis with a tool like DealSheet AI is essential for making fast, accurate, and confident investment decisions.

Looking Beyond Yield to Find Great Investments

While knowing your rent yield is the first step to understanding an asset's cash flow, it's only one piece of the puzzle. The most successful UK property investors use a toolkit of different metrics to see the complete financial picture. It's what lets them make smarter, faster decisions.

Think of it this way: yield is king for income, but other metrics reveal how efficiently your own cash is working and what your total, all-in return could be.

Looking beyond yield helps you build a more balanced and resilient portfolio. A property in a prime London borough, for example, might offer a modest net yield of only 3%. Judged on that alone, you'd walk away. But its potential for strong capital growth could deliver a far greater total return over five years than a high-yielding property in a more static market.

Return on Investment (ROI) and Cash-on-Cash Return

One of the most powerful metrics in an investor's toolkit is Return on Investment (ROI), often called Cash-on-Cash Return in property circles. This number cuts through the noise and gets straight to the point.

It answers the most important question you can ask:

"For every pound I personally put into this deal, how many pennies do I get back each year?"

It's laser-focused on the return you get on your own invested capital—your deposit, stamp duty, legal fees, and any refurbishment costs.

The calculation is simple but incredibly insightful:

Annual Net Profit (Pre-Tax) / Total Cash Invested = ROI %

This is absolutely vital when you're using a mortgage, as it separates the bank's money from your own. A high ROI means your capital is working extremely hard for you, which is the entire point of leveraged investing.

To go deeper on this, check out our complete guide on what is a good ROI on rental property.

Understanding Capitalisation Rate (Cap Rate)

Another important term you'll hear, particularly in commercial property or when assessing larger portfolios, is the Capitalisation Rate, or Cap Rate.

Its calculation looks almost identical to net yield, as it compares the property's Net Operating Income (NOI) to its value.

The main difference isn't the formula, but its application. While net yield is used by an investor to assess their personal return on their specific purchase price, Cap Rate is used more broadly to value a property based on its income-generating potential relative to the current market. It's a way to compare different commercial assets on a like-for-like basis, almost like a market-wide benchmark.

Key UK Property Investment Metrics Explained

To make sense of how these different metrics fit together, it's useful to see them side-by-side. Each one tells you something different, and using the right one for the right question is what separates good analysis from a hopeful guess.

| Metric | What It Measures | Best For Assessing |

|---|---|---|

| Gross Yield | Annual rent relative to the property's purchase price. | Quick, initial filtering of deals before you factor in costs. |

| Net Yield | Annual profit (after operating costs, but before finance) relative to the purchase price. | The property's operational profitability, independent of your mortgage. |

| Cash-on-Cash Return (ROI) | Annual profit relative to the total cash you personally invested. | The efficiency of your own capital, especially in leveraged (mortgaged) deals. |

| Capitalisation Rate (Cap Rate) | Net Operating Income (NOI) relative to the property's current market value. | Comparing the relative value and risk of different income-producing assets in a market. |

Ultimately, great investors don't rely on a single number. They combine these metrics to build a complete picture: yield for cash flow, ROI for capital efficiency, and a keen eye on capital growth for long-term wealth creation. Getting this balance right is what turns a decent investment into a great one.

How Inflation and Hidden Costs Impact Your Real Return

Your calculated net yield isn't a static number. Think of it as a living figure, constantly being pushed and pulled by big economic forces and the messy realities of owning a property. For investors looking ahead to 2026, getting a handle on these dynamics isn't just good practice—it's essential for survival.

On one hand, inflation can actually be a landlord's best friend. As rents gradually rise over the years, your income goes up. But the price you paid for the property? That stays fixed. This simple but powerful effect, sometimes called "yield on cost," means your rent yield can grow substantially over time, becoming a serious wealth-building engine.

The Hidden Costs That Erode Profit

But there's a flip side. Hidden costs and rising expenses can quietly eat away at your returns, often when you least expect it. These are the financial shocks that never show up in a simple yield calculation but can deal a heavy blow to your actual cash flow.

Some of the most common culprits include:

- Capital Expenditures (CapEx): These aren't your day-to-day repairs; they're the big, infrequent hits. Think a new boiler (£2,000+), a major roof repair (£5,000+), or replacing all the windows in one go.

- Escalating Service Charges: If you own a leasehold property, service charges and ground rents can—and often do—increase. Sometimes these hikes are sudden and significant, hitting your bottom line directly.

- Rising Mortgage Rates: Are you on a variable rate or nearing the end of a fixed term? A jump in interest rates can dramatically inflate your single biggest cost, potentially turning a profitable asset into a monthly liability.

A successful investment isn't just about the yield you calculate today; it's about the cash flow you can protect tomorrow. Proactive financial modelling separates profitable landlords from those who face unexpected financial strain.

Inflation's Impact on UK Rents

For investors planning for 2026, understanding rental inflation is key. UK rents have seen significant growth, and while the pace may moderate, the underlying supply-and-demand imbalance suggests rents will continue to rise. This makes accurate forecasting essential. It's not just about today's numbers; it's about modelling how future rent increases, alongside rising costs for maintenance and compliance, will affect your profitability over the next five to ten years.

For any serious investor, this volatility makes forecasting future cash flow absolutely critical. This isn't just about rent; it also means factoring in future tax liabilities like Stamp Duty Land Tax as part of your analysis. You can learn more by reading our guide explaining what is Stamp Duty Land Tax.

Modelling how different inflation scenarios will affect your rent yield and cash flow is a cornerstone of professional deal analysis. It's this proactive approach that helps you truly understand a property's resilience before you put your capital on the line.

FAQs: Your Rent Yield Questions Answered

To wrap things up, let's tackle some of the most common questions UK property investors have about rent yield. Think of this as the practical advice you need to move from theory to confident decision-making.

What Is a Good Rent Yield in the UK?

Honestly, a "good" yield depends entirely on your strategy and where you're investing in the UK. There's no single magic number, but as a rule of thumb for 2026, many investors will aim for a gross yield of at least 5-6% on a standard buy-to-let.

But context is everything. In high-performing areas like the North East, an investor focused on cash flow might see 7-8% as a more realistic target. For more complex strategies like an HMO, you'd want to see a gross yield of 10% or more to make the extra management and operational hassle worthwhile.

Ultimately, a good yield is one that leaves you with positive net cash flow after every single cost—from the mortgage and management fees right through to tax—has been accounted for and paid.

Does Capital Appreciation Affect My Rental Yield?

No, not directly. Capital appreciation—the increase in your property's market value over time—isn't part of the rental yield calculation. Yield is purely about the rental income relative to what you paid for the property.

That said, appreciation is a massive part of your Total Return on Investment. Some investors will happily accept a lower yield in an area with a strong chance of long-term capital growth, playing the long game. Others need high yields for immediate monthly income. The smartest strategies often find a balance between the two, generating both cash flow today and wealth for tomorrow.

How Do UK Taxes Like Section 24 Wreck My Net Yield?

Section 24 has a huge and often underestimated impact on the net yield for any higher or additional-rate taxpayer holding property in their personal name. In simple terms, this legislation stops you from deducting mortgage interest as a business expense when working out your taxable profit.

Instead, you get a basic-rate tax credit of just 20% on your interest payments. If you're a 40% taxpayer, this means you're paying significantly more tax, which directly eats into your final net profit and your real-world net yield. This rule makes it absolutely essential to model deals using UK-specific tax rules, not a generic calculator.

At DealSheet AI, we built our platform to handle these complex, UK-specific calculations for you. Stop wrestling with fragile spreadsheets and start making faster, data-driven decisions. Analyse your next property deal in seconds by downloading the DealSheet AI app today.